- Soft stainless demand weighs on market sentiment

- Lower chrome concentrate tags reduce cost support

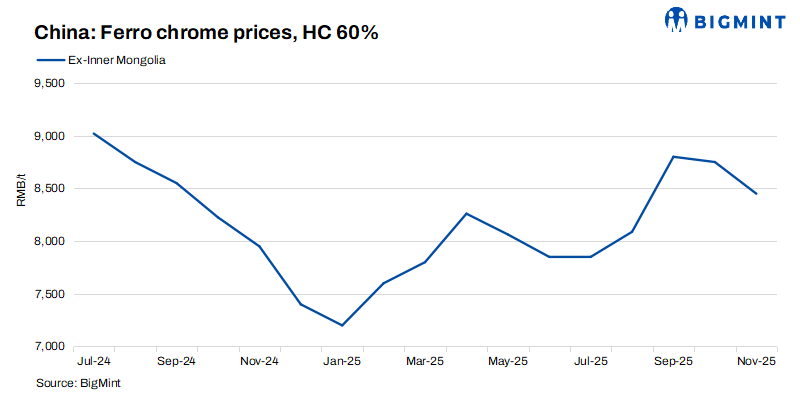

Mysteel Global: The shift from supply tightness during this year’s third quarter to a fourth-quarter surplus has sent China’s spot prices of high-carbon ferro chrome into decline. The supply pressure is set to compound with the commissioning of greenfield smelter projects that are likely to cause prices to decline even lower.

The results of Mysteel’s most recent survey of the 177 domestic smelters regularly tracked and representing 95% of domestic capacity show that during October, China’s HC ferro chrome production climbed to a new peak of 825,000 tonnes (t).

This has added immediate pressure to the domestic spot market, a Shanghai-based analyst observed, pressure that will intensify with the commissioning of a combined 280,000 t of new HC ferro chrome smelting capacity in North China’s Inner Mongolia this month. Meanwhile, 90,000 t of production capacity in the region was shifted to produce HC ferro chrome in November.

On the demand side, Mysteel Global noted that consumption of the ferro alloy has dwindled as the stainless steel sector reduces production. A slight contraction is on the horizon, with planned crude stainless output in November projected at 3.46 million tonnes (mnt), down 1.7% from October’s actual production, according to Mysteel’s latest survey of 43 stainless producers.

Also boding ill for ferro chrome prices are lower feedstock prices, the Shanghai analyst said. On 17 November, Mysteel assessed the portside prices of 40-42% South African chrome concentrates at RMB 53.25/dmtu ($8/dmtu), down by RMB 3/dmtu ($0.4/dmtu) from the previous month.

Seaborne prices have followed a similar southward trend. Mysteel assessed the CIF price for 40-42% chrome concentrates shipped from South Africa to Tianjin at $278/dmt on 17 November, lower by $4/dmt from a month earlier.

Despite this, smelters remain profitable, a key factor explaining their high operating rates. Mysteel’s latest assessments suggest that by 14 November, the average profit margin for producing HC ferro chrome using the semi-closed submerged arc furnace-electric furnace route stood at 3.31% in Inner Mongolia, China’s primary production hub.

All these factors will continue to weigh on spot HC ferro chrome prices going forward, the analyst concluded.

Mysteel’s assessment showed that on 17 November, prices of 55% high-carbon ferro chrome in Inner Mongolia, the benchmark in the domestic ferro chrome market, had slumped to RMB 8,100/t ($1,140/t), 50Cr, ex-works including VAT – a significant RMB 400/t ($56/t) decline from the prior month.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply