- Sales volumes decline q-o-q in Q2FY’26 due to monsoon-led disruptions

- Margins weaken q-o-q on lower realisations, seasonal cost pressures

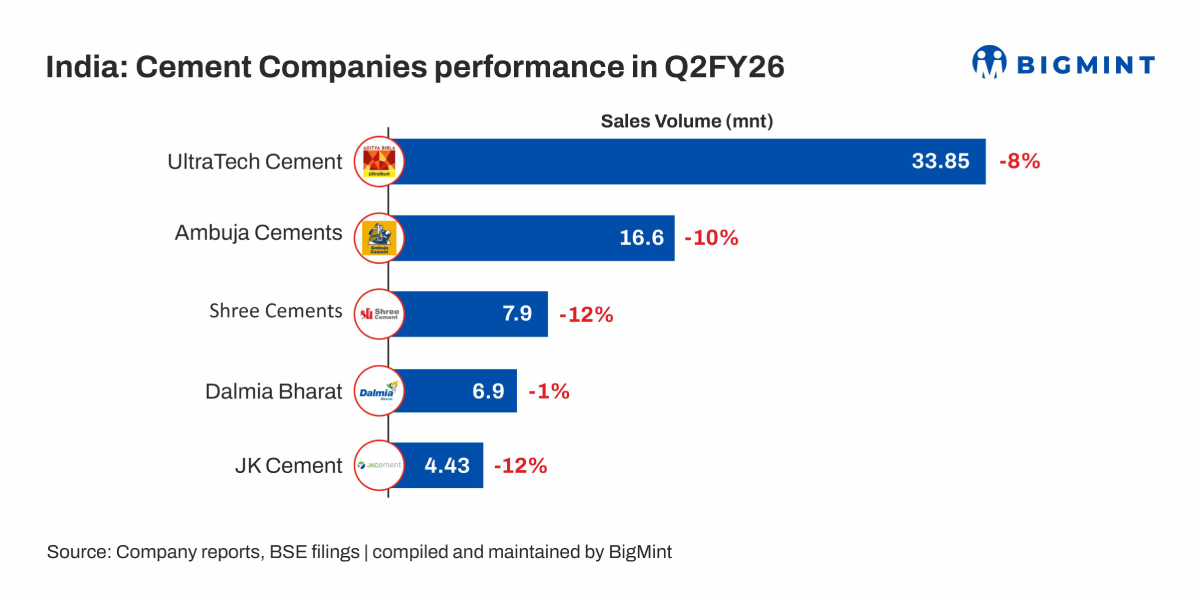

India’s leading cement companies witnessed a drop in Q2FY26 performance, as monsoons weighed on construction activity and led to an 8–14% sequential volume declines for UltraTech, Ambuja, Shree, JK Cement, and Dalmia Bharat. EBITDA per tonne also softened q-o-q due to lower realisations, seasonal cost pressures, and maintenance shutdowns.

On a y-o-y basis, however, the sector delivered growth in performance, with 3-20% growth in sales volumes and significant EBITDA/t expansion of up to 56%, supported by lower fuel costs, better operational efficiencies, and improved product mix. Companies continued to pursue capacity additions, RMC expansion, clinker upgrades, and debottlenecking initiatives, positioning the industry for a rebound in H2FY’26 as post-monsoon demand strengthens.

Company-wise performance

1. UltraTech Cement’s consolidated sales volumes declined 8% q-o-q to 33.85 million tonnes (mnt) in Q2 from 36.83 mnt in Q1 owing to monsoon-led demand weakness and soft construction activity. Domestic grey cement volumes also eased sequentially. EBITDA per tonne stood at INR 966/t, down 23% q-o-q from INR 1,248/t in Q1, driven by lower realisations and seasonal cost pressures.

On a y-o-y basis, volumes rose 7% from 31.67 mnt in Q2, supported by network expansion and stable underlying demand. EBITDA per tonne improved 24% y-o-y from INR 778/t, aided by lower fuel, power, and logistics costs. Grey cement realisations were higher y-o-y despite a slight sequential dip.

The company continued to augment capacity, maintaining its trajectory toward 212 mtpa by FY27. With demand expected to recover post-monsoon and cost tailwinds persisting, the company remains optimistic about sustaining healthy volume growth and margin resilience in FY26.

2. Ambuja Cement’s standalone cement sales volume dropped 10% on the quarter to 16.6 mnt in Q2 as against 18.4 mnt in the previous quarter. EBITDA per tonne was recorded as INR 1,060/t, largely stable q-o-q due to improved mix and operational leverage.

Volumes surged 20% y-o-y from 13.8 mnt in Q2FY’25. EBITDA/t was up by 32% y-o-y, and consolidated EBITDA rose 58% y-o-y to INR 1,761 crore.

The company raised its FY’28 capacity target to 155 mnt/year, driven by debottlenecking, while staying debt-free. It expects demand tailwinds from GST reform and infrastructure spending and aims to cut costs further to INR 4,000/t by the end of FY’26.

3. Shree Cement’s sales volumes declined 12% q-o-q due to monsoon-driven construction slowdown and softer retail demand. EBITDA per tonne stood at INR 1,078/t in Q2, down nearly 21% q-o-q, affected by lower realisations, higher maintenance shutdowns, and seasonal cost pressures. Premium product sales also saw a temporary dip sequentially, impacting blended margins.

On a y-o-y basis, sales volumes were up by 7% to 7.9 mnt in Q2, supported by stronger demand in core northern and eastern markets. EBITDA rose a robust 43% y-o-y, aided by higher premium cement contribution, improved fuel efficiency, and reduced logistics cost. Green power usage rising to 63% also supported margin expansion, while trade sales mix remained healthy.

Demand recovery post-monsoon and ramp-up of new capacities are expected to support better volumes and margins in H2FY’26.

4. JK Cement’s volumes fell q-o-q to 4.40 mnt in Q2 from 5.10 mnt in Q1, impacted by seasonal demand softness, maintenance shutdowns, and higher input costs. EBITDA per tonnes declined to INR 902/t, down from INR 1,247/t in Q1, as the company absorbed higher maintenance and power/fuel costs.

On a y-o-y basis, grey cement volume grew 16%, while white cement & wall putty volumes rose 10%, reflecting sustained traction in core markets. EBITDA surged 57% y-o-y, supported by strong realizations and cost optimization, lifting total EBITDA to INR 447 crore.

The company’s near-term margins may see pressure due to maintenance and marketing spends, but its long-term outlook remains firm, thanks to capacity expansions in Panna, Hamirpur, Bihar, and Prayagraj, plus focused cost control and green power mix.

5. Dalmia Bharat’s cement sales volume declined slightly q-o-q to 6.9 mnt in Q2 from 7 mnt in Q1. EBITDA per tonne fell to INR 1,013/t, down by 20% from INR 1,261/t in last quarter, largely due to higher fixed costs and the startup phase for its Umrangso clinker line.

On y-o-y basis, volumes were up nearly 3% from 6.7 mnt in Q2, while EBITDA/t surged 56%, driven by strong realisations, lower fuel costs, and improved efficiency.

The company also began a 3.6 mnt/year clinker line trial run in Umrangso, with commercial production expected by Q3FY’26, reflecting confidence in long-term capacity expansion.

Note: Sales volumes and EBITDA per tonne figures have been rounded off in this article.

Leave a Reply