- Benchmark HRC prices drop INR 600/t w-o-w

- Sentiments soften in BF rebar market after last week’s price hike

- Supply glut in certain product segments weighing on prices

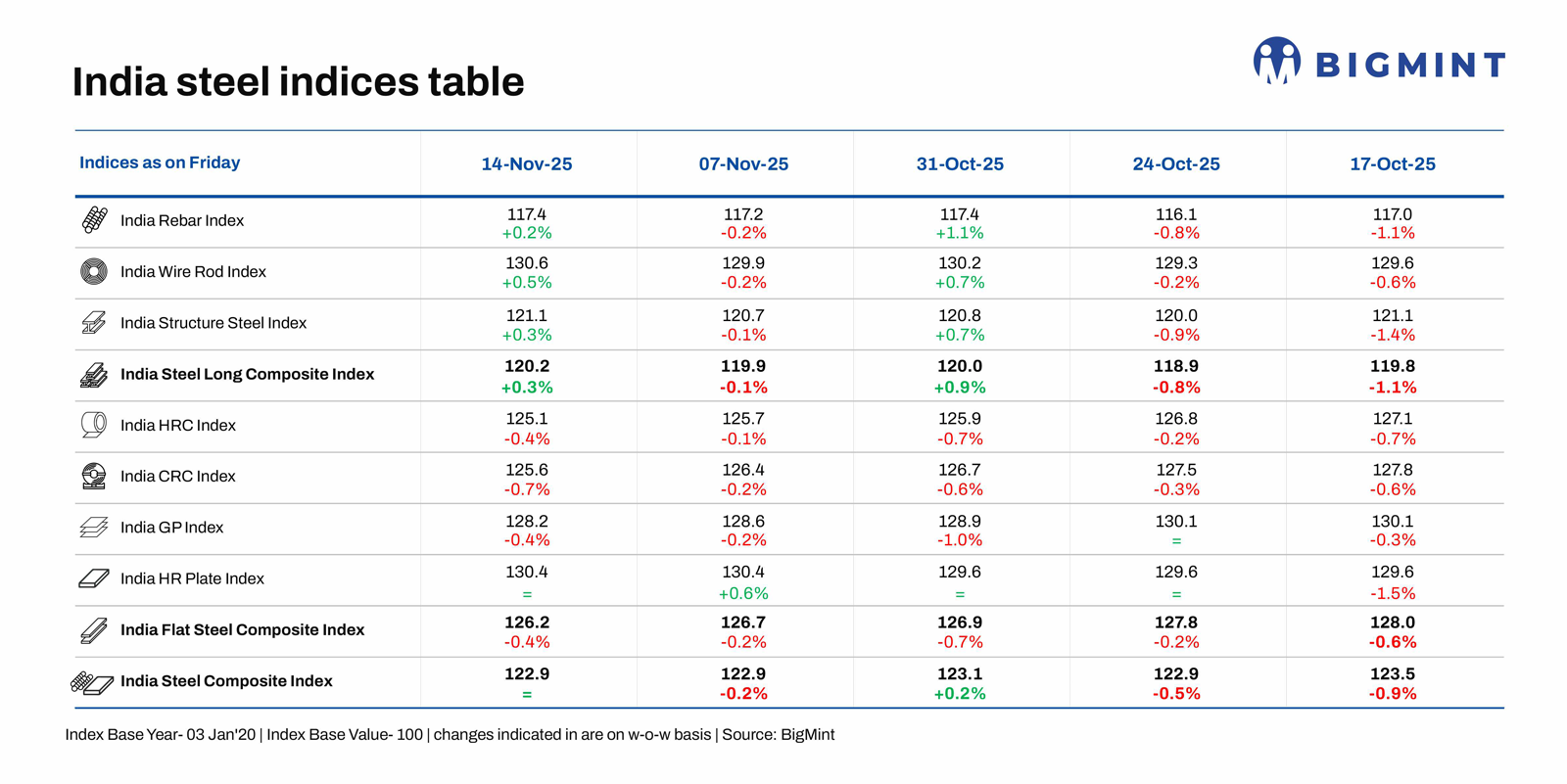

Morning Brief: BigMint’s India steel composite index, a barometer of the domestic steel market, remained flat w-o-w as assessed on 14 November 2025 amid mixed trends in steel prices observed across the country. Market fundamentals remain strong with higher growth expected in Q3 and Q4 of the current fiscal compared to the preceding quarters.

However, crude and finished production growth of roughly 12-13% y-o-y in the current fiscal seems to be outpacing consumption which grew at a rate of roughly 8% y-o-y in H1FY’26, as per Minister of Steel data. With the rapid expansion and buildout of new facilities and product lines, a supply glut has emerged in many regional markets, which is weighing on prices.

After the unseasonal rains and disruptions in October the market expected a rebound in steel prices in November, which is yet to materialise. The flats index edged down by 0.4% w-o-w while longs gained 0.3%. However, pricing trends showed wide variations across markets.

Highlights of price movements

Downtrend in flat steel market: Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends w-o-w. Some markets saw a downtrend, while in others prices remained firm. HRC prices hovered between INR 46,500-48,300/t ($525-546/t) across regions, while cold-rolled coil (CRC) prices ranged between INR 52,000-56,500/t ($588-538/t).

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 600/t ($7/t) w-o-w to INR 47,000/t ($531/t) on 11 November against INR 47,600 ($538/t) on 4 November. CRC (IS513, Gr O, 0.9 mm/CTL) prices decreased by INR 400/t ($5/t) w-o-w to INR 55,100/t ($622/t) on 11 November. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Domestic HRC market sentiment remained subdued amid weak demand and slow trade. A market participant stated that no fresh offers or inquiries were heard, reflecting limited trading activity. Liquidity constraints continued to pile pressure, while distributors struggled to secure workable prices.

Sentiments soften in rebar market: Trade-level BF rebar prices dropped w-o-w owing to slow demand across markets. Some primary mills either offered price support or reduced list prices amid weak market sentiments. Trade-level BF rebar prices dropped by INR 500/t w-o-w to INR 47,300/t ($533/t) exy-Mumbai, as per BigMint’s benchmark assessment on 14 November. Prices are exclusive of GST at 18%. In the projects segment, prices hovered between INR 45,500-46,500/t ($513-524/t) FOR Mumbai.

Inventories at mills reduced slightly by 8% in mid-November as compared with levels seen at the beginning of the month, as per sources. However, inventories are still at elevated levels. JSW Steel’s standalone crude steel production rose 9% y-o-y despite reduced capacity utilisation due to the BF-3 shutdown at Vijayanagar. Capacity utilisation stood at around 92% (excluding BF-3). This has increased supply, putting pressure on prices.

IF rebar prices exhibited mixed trends w-o-w across key markets. Trade activities improved slightly, supported by an uptick in semi-finished steel prices. Inventory levels remained steady at 12-15 days across regions.

Outlook

Most the primary mills had increased list prices the week before last. However, the hikes don’t seem to have been absorbed by the market in the absence of any significant improvement in trade sentiments. Most of the Tier-1 mills reported shrinking EDITDA margins in Q2FY’26 and domestic iron ore and imported coking coal costs remain firm.

Therefore, some form of rationalisation of production in certain segments is to be expected. This supply-demand balance will play out as per the dynamics of the different regional markets.

Leave a Reply