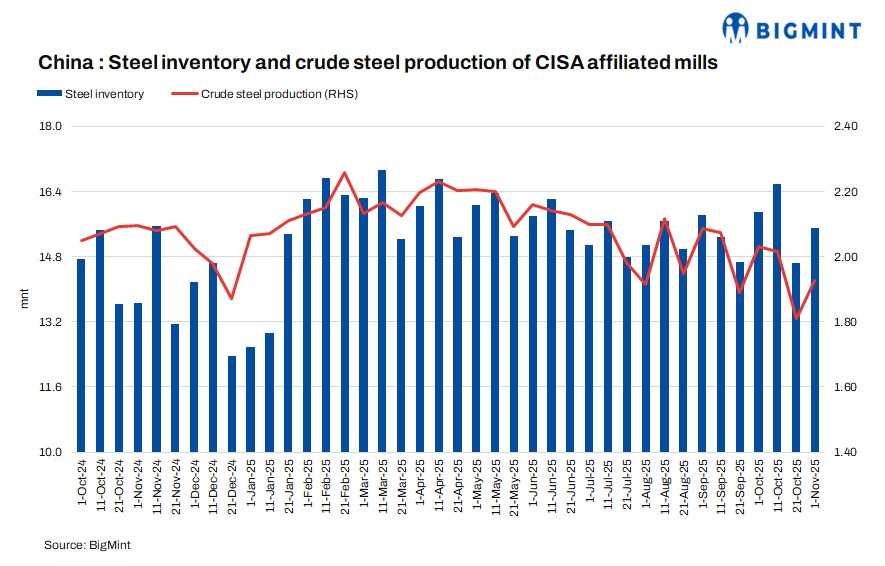

- Rising inventories highlight sluggish steel demand

- Output fluctuations reflect cautious mill operations

The China Iron and Steel Association (CISA) has reported that the total steel inventory at key Chinese enterprises in early November 2025 stood at 15.49 million tonnes (mnt), marking an increase of 860,000 tonnes (t) or 5.9% from late October 2025. However, inventory levels decreased by 390,000 tonnes or 2.5% compared with the same period last month. On a y-o-y basis, stocks were higher by 1.83 mnt or 13.4%, indicating continued supply pressure and subdued demand across the steel value chain.

Production volumes

The average daily crude steel output of CISA-affiliated enterprises reached 1.926 mnt in early November, rising by 6.0% from late October. However, output was down by 8.1% y-o-y, reflecting lower operational rates than in 2024.

The average daily finished steel output stood at 1.884 mnt, declining by 5.5% from late October. Production also fell by 3.5% y-o-y, signalling soft rolling activity amid muted downstream demand.

The average daily pig iron output was 1.804 mnt, up 3.5% from late October. On a y-o-y basis, pig iron output dropped by 4.1%, as mills adjusted blast furnace operations in line with market conditions.

Outlook

China’s steel market is expected to remain weak in the near term as inventories remain elevated, and demand continues to be sluggish amid the seasonal slowdown. While crude steel production showed an improvement from late October, overall output still lags behind last year, limiting supply pressure to some degree. Prices are likely to remain range-bound to soft until real consumption picks up and inventories begin to ease.

Leave a Reply