- LME stocks adequate for >1 day of consumption

- Indian govt revokes 2025 QCO on refined zinc

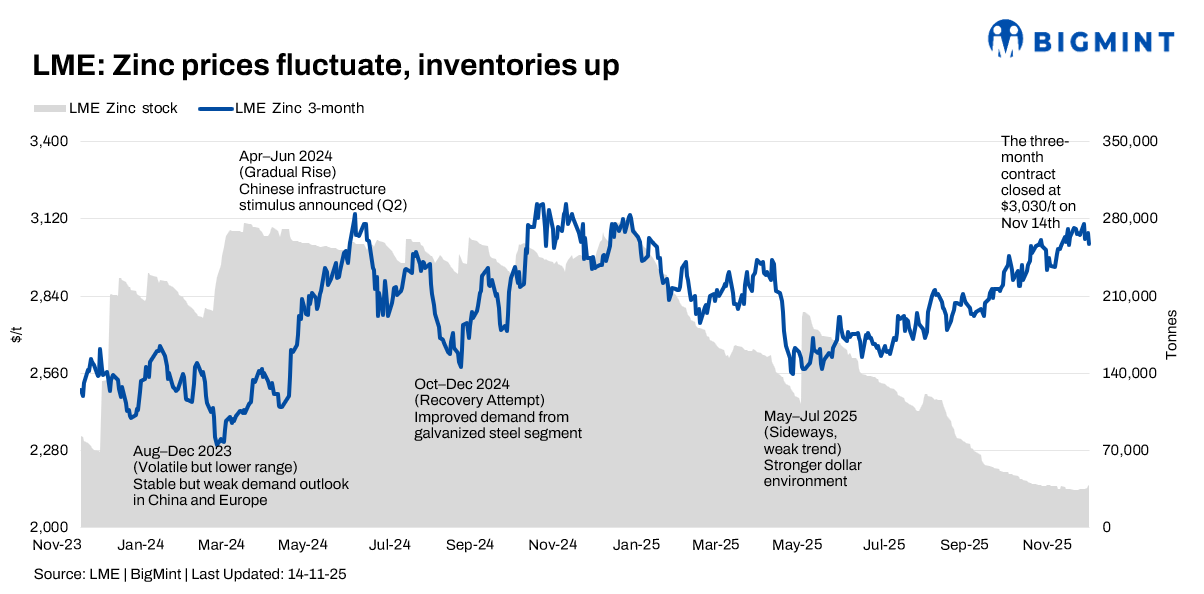

The global zinc market recorded a week of volatility but maintained an overall upward bias during Week 46 (10-14 November 2025). Prices traded within a narrow band through most sessions, supported by persistently tight LME inventories and a mild rebound in physical premiums. However, weak macroeconomic cues and mixed Chinese demand capped the upside as the week progressed.

Price trends

LME zinc cash-settlement prices fluctuated throughout the week, ending slightly higher. Prices opened at $3,190/tonne (t) on 10 November and closed at $3,255/t on 14 November, marking a 2.03% rise. The three-month contract moved in the opposite direction, drifting from $3,101.50/t to $3,030/t, a 2% decline.

Inventory analysis

LME zinc inventories remained extremely tight despite rising through the week. Stocks were at 34,900 t on 10 November and increased steadily through 11-13 November, reaching 38,975 t on 14 November, up 11.67% over the week. The additional warrants eased some supply pressure, prompting mild price pullbacks. Still, zinc inventories remained historically low — less than one day of global consumption — maintaining structural tightness.

MCX zinc trends (November 10-14)

MCX zinc prices fluctuated throughout the week, reflecting the volatile global sentiment and domestic factors. The 28 November contract closed at INR 304,700/t on 10 November and INR 303,350/t on 14 November, marking a decline of 0.44% after reaching INR 305,700/t on 13 November. The Indian market reacted to global cues, with some trimming of positions observed, which weighed on zinc prices. However, some earlier support came from global factors and a pick-up in spot demand.

SHFE zinc trend

The most-traded SHFE ZN2512 contract closed at RMB 22,500/t on 14 November, down 0.62% from RMB 22,640/t on 10 November. The SHFE/LME price ratio was near 7.4, keeping the import window shut. With the US government shutdown ending and the Fed signalling cautious hawkishness, rate-cut expectations weakened. Weak Chinese macro data further suppressed sentiment.

India withdraws refined zinc quality control order, easing import norms

The Ministry of Mines revoked the Refined Zinc (Quality Control) Order, 2025 on 13 November, removing mandatory BIS/ISI certification for refined zinc imports. This simplifies customs clearance and reduces procurement costs. India imported 0.24 mnt of zinc during January-August 2025, primarily from South Korea (0.09 mnt) and Japan (0.03 mnt), and supply diversity is expected to expand as regulatory hurdles fall.

Outlook

The near-term zinc outlook remains cautious. Persistent oversupply concerns, particularly with weak Chinese demand, and mixed macroeconomic signals are likely to keep prices volatile. The market will closely monitor consumption trends and inventory movements for future price indications.

Leave a Reply