- Indonesia, Colombia, and Canada recorded sharp declines in shipments

- Freight softness across Pacific routes weighed on fixtures

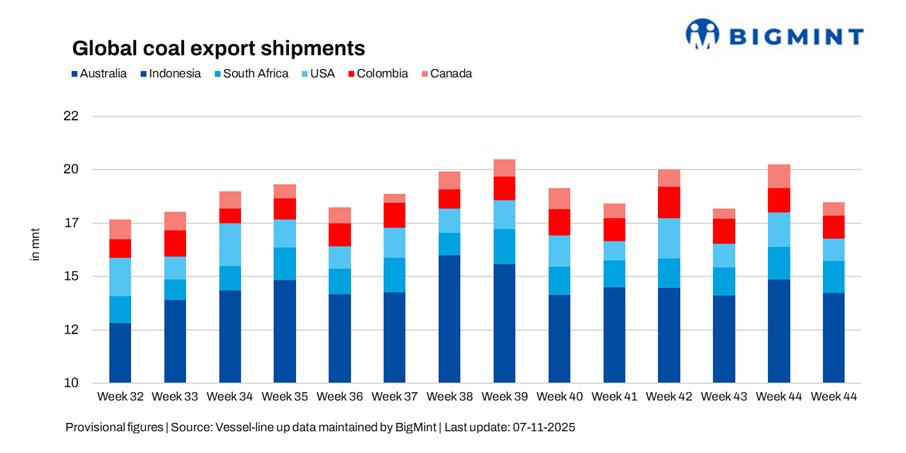

Global seaborne coal exports fell 8.5% week-on-week (w-o-w) to 18.16 million tonnes (mnt) in week 45 (1-7 November 2025) from 19.84 mnt in week 44 (25-31 October), according to BigMint’s vessel line-up data. The decline was led by lower shipments from Indonesia, Colombia, and Canada, while Australia remained a notable exception with a marginal increase in volumes.

The slowdown reflected post-festive weakness in Indian demand, adverse weather conditions due to cyclone-related disruptions along India’s east coast, and freight market softness across key Pacific routes. With several buyers having restocked ahead of the festive period, fresh fixtures remained limited even as vessel availability improved across most load regions.

Country-wise trends

Australia’s coal exports rose 1.6% w-o-w to 7.33 mnt in week 45 from 7.21 mnt in week 44, supported by steady operations at major terminals – Newcastle (3.04 mnt), Gladstone (1.36 mnt), and DBCT (1.26 mnt). Consistent miner output, efficient rail movement, and favourable weather conditions helped maintain smooth loading activity despite a broader slowdown in fresh fixtures.

Demand from Japan (2.00 mnt) and China (1.83 mnt) remained firm, offsetting softer Indian buying. Major exporters such as Glencore (0.80 mnt) and BHP (0.69 mnt) continued stable shipments under long-term contracts, while limited spot tenders and cautious procurement by Indian buyers capped any further upside in overall export volumes.

Indonesia’s coal exports fell sharply by 9.7% w-o-w to 6.73 mnt in week 45 from 7.45 mnt a week earlier, as sluggish post-festive Indian demand and weak freight sentiment curtailed new bookings. Loadings dropped across key terminals – Taboneo (1.50 mnt), Bunati (1.17 mnt), and Samarinda (1.09 mnt) – amid subdued vessel scheduling and slower cargo nominations. Cyclone-related disruptions along India’s east coast further impacted shipment flow, leading to longer turnaround times and cautious chartering activity.

On the demand side, China (1.78 mnt) and India (1.24 mnt) remained principal buyers, while imports from the Philippines (0.64 mnt) and Japan (0.60 mnt) edged lower amid weak industrial offtake and limited spot procurement. Although miners attempted to sustain output, subdued buying interest across the Pacific Basin and freight pressure on short-haul routes continued to weigh on Indonesia’s overall export momentum.

South Africa’s coal exports dipped 3.4% w-o-w to 1.43 mnt in week 45 from 1.48 mnt in week 44, with volumes largely supported by stable operations at Richards Bay (1.43 mnt). While intermittent rail bottlenecks persisted, improved scheduling and better vessel coordination helped sustain near-steady throughput during the week. However, overall market activity remained subdued amid soft global demand and limited fresh fixtures.

Weaker Indian buying at 0.59 mnt, partly due to reduced sponge iron production and lower industrial coal consumption, restricted export growth potential. India (0.55 mnt) continued to be the main destination, while European demand stayed muted as buyers refrained from spot procurement amid elevated freight rates and weak import margins.

Colombia’s coal exports fell sharply by 35.2% w-o-w to 1.00 mnt in week 45 from 1.55 mnt in the previous week, as operational slowdowns and reduced cargo nominations weighed on port activity. Loadings at Puerto Nuevo (0.65 mnt) and Puerto Bolivar (0.31 mnt) declined notably, with producers curtailing shipments amid rising freight costs and weak demand from the Atlantic basin. Adverse weather conditions and vessel scheduling delays further contributed to lower throughput during the week.

Major exporters such as Prodeco Group (0.65 mnt) and Cerrejon Mines (0.31 mnt) recorded slower loading activity, reflecting restrained export momentum. On the demand side, Brazil (0.21 mnt) and Turkey (0.17 mnt) emerged as the key importers, though overall buying interest across Europe and the Mediterranean remained tepid amid muted industrial demand and high voyage costs.

US coal exports declined modestly by 4.4% w-o-w to 1.04 mnt in week 45 from 1.09 mnt in week 44, supported by steady loadings at Baltimore (0.30 mnt), Norfolk (0.27 mnt), and Mobile (0.26 mnt). Consistent terminal operations helped sustain volumes despite subdued export interest from Asian buyers and weaker chartering activity across the Atlantic.

Soft European demand and limited Indian fixtures continued to weigh on market sentiment, with India (0.32 mnt) emerging as the leading destination. However, elevated voyage costs, weak power sector coal consumption, and slower industrial recovery across key import hubs kept overall shipment momentum restrained through the week.

Canada’s coal exports dropped 41% w-o-w to 0.62 mnt in week 45 from 1.06 mnt in week 44, marking the steepest decline among major exporters. Lower rail deliveries and weaker buying interest from Pacific Basin markets constrained shipments through Roberts Bank (0.22 mnt), Vancouver (0.25 mnt), and Prince Rupert (0.15 mnt). Disruptions to rail logistics and port congestion further affected vessel scheduling, leading to reduced loadings across key terminals.

Elk Valley Resources (0.25 mnt) remained the principal shipper during the week, though subdued industrial demand and persistent weather-related challenges limited export momentum. Japan (0.31 mnt) emerged as the leading destination, but muted procurement from other Northeast Asian buyers and cost-sensitive chartering kept overall activity subdued.

Soft Freight Hits Coal Shipments

Freight market conditions remained soft in week 45 as India’s coal demand weakened post festive season and cyclone-related disruptions slowed port operations. Rates declined across the Pacific basin, particularly on the Indonesia-India corridor, while the Atlantic market held largely steady amid limited inquiries.

Softer Panamax and Supramax indices reflected weaker vessel demand, with higher bunker prices adding mild cost pressure. The subdued freight environment dampened shipment momentum from Indonesia and the Atlantic, as exporters avoided concluding new fixtures at unfavourable levels.

Outlook

Global seaborne coal exports are likely to remain range-bound in the near term as sluggish industrial demand and freight softness continue to weigh on fixtures. While Australian shipments may hold steady owing to resilient miner output and stable Northeast Asian demand, export momentum from Indonesia and Colombia could remain subdued amid weak Indian procurement.

Recovery prospects hinge on weather normalisation and seasonal restocking ahead of winter, though cautious chartering and limited buying interest suggest overall trade activity may stay subdued through mid-November. Meanwhile, Queensland’s CleanCo has partnered with Aurizon to supply 25% of its power from renewable sources, supporting Aurizon’s net-zero 2050 goal and boosting the global competitiveness and sustainability of Queensland’s metallurgical coal exports.

Leave a Reply