- Deregulation to ease raw-material sourcing constraints

- Downstream sectors expect reduced cost pressures

The Ministry of Mines has revoked the Quality Control Orders (QCOs) on copper, aluminium, zinc, nickel and tin, formally scrapping the BIS certification requirements imposed between 2023 and 2025. The notification, issued on 13 November 2025, marks one of the most significant deregulation moves for India’s non-ferrous value chain in recent years.

NITI Aayog recently recommended that the QCOs be rolled back due to industries’ persistent difficulties in securing both raw materials and finished metal, with certification delays tightening supply and inflating premiums. A BIS representative added that more QCOs remain under review for possible withdrawal as policymakers push to ease compliance burdens and stabilise material availability.

How did QCOs disrupt metal sourcing?

The QCOs were designed to ensure quality benchmarks for imported metals, but the implementation created friction across supply chains. Factory audits, sample testing, documentation layers and lengthy approvals kept several overseas suppliers — across Asia, Europe, the Middle East, Africa and the Americas — out of the Indian market. The reduction in supplier participation tightened availability, raised premiums and triggered recurring shipment delays, particularly for MSMEs. The withdrawal removes these operational bottlenecks, offering buyers more predictable procurement cycles.

What does QCO withdrawal mean for copper?

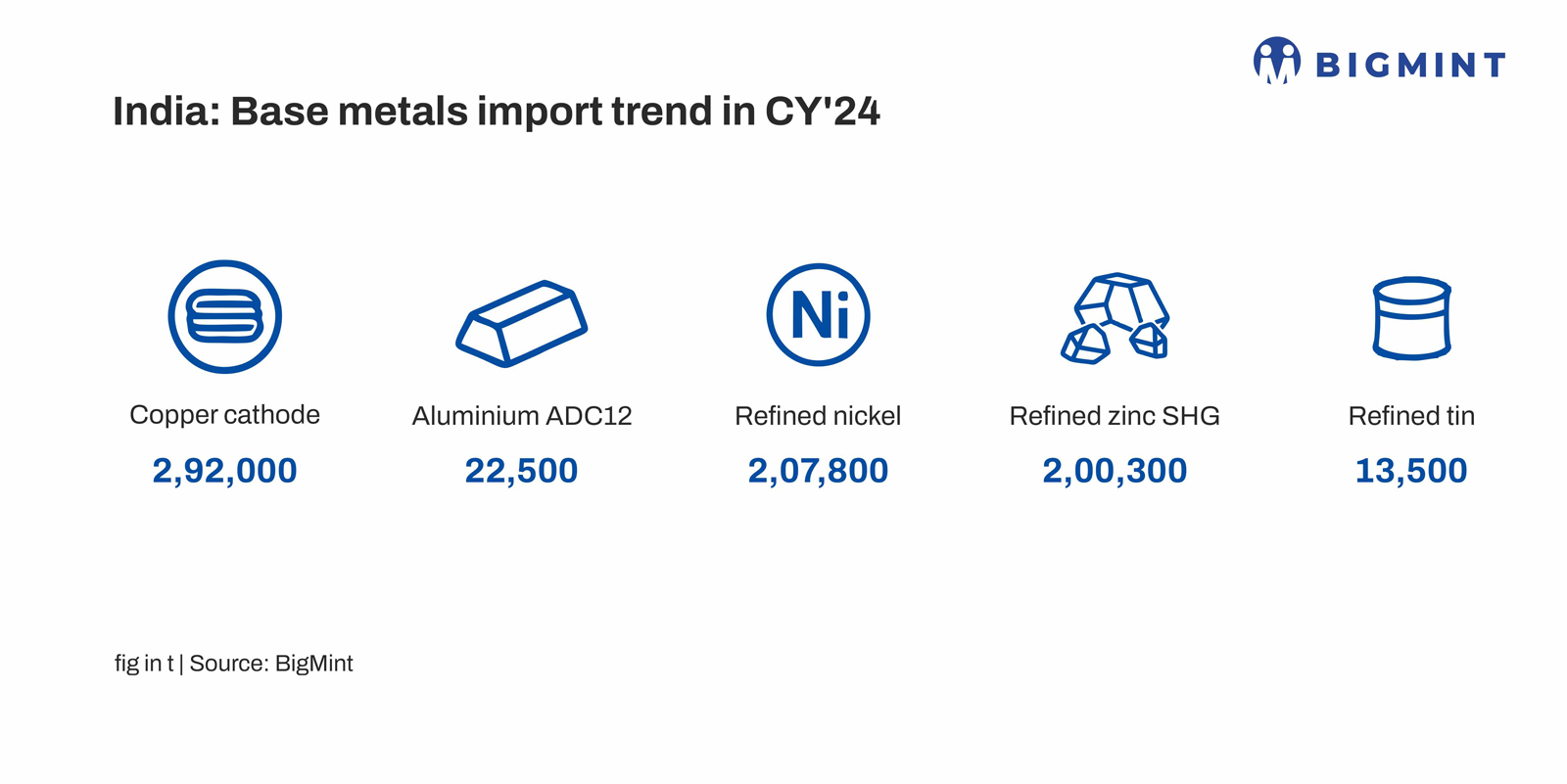

Copper cathode imports declined from 357,000 tonnes (t) in 2023 to 292,000 t in 2024, but inflows began to recover in 2025 with 177,000 t imported by September. The trend suggests the QCO slowed but did not halt inflows. With the order withdrawn, traders expect more global producers to resume shipments, improving cathode availability for wire rod mills, tube makers, and downstream fabricators as demand strengthens in early 2026.

India relies on imports for nearly one-third of its cathode requirement due to slower domestic smelting expansion. Construction and infrastructure account for around 40-45% of total copper consumption, making India’s downstream industries sensitive to global supply conditions. Copper cathode imports fell 7% y-o-y in Q2FY’25 to 70,135 t. With the QCO now lifted, buyers expect smoother procurement during the upcoming infrastructure and clean-energy capex cycle.

How will aluminium & alloy markets respond?

While India’s aluminium ADC12 imports were 22,500 t in CY’24, up drastically y-o-y, in H1CY’25, inflows shrank 87% to 1,188 t from 9,417 t a year earlier, despite favourable trade agreements with key suppliers. The policy reversal is viewed as part of a broader effort to stabilise input availability for automotive castings, engineering alloys, and downstream fabrication units.

The removal of mandatory certification is expected to improve inflows of ADC12 and other alloy grades, supported by new BIS approvals recently granted to producers in Malaysia. Market participants expect reduced sourcing friction and smoother customs clearance, though a major price correction remains unlikely given firm upstream costs. Quality-control norms for select downstream aluminium products remain in force, and authorities may continue monitoring through DGFT documentation and updated compliance systems.

What changes for zinc buyers?

Refined zinc SHG imports totalled 200,300 t in CY’24, down 13% from CY’23. However, India imported around 240,000 t of refined zinc between January-August 2025, led by South Korea (90,000 t) and Japan (30,000 t), with diversified volumes from the US, the UAE, Singapore and Europe.

The elimination of the QCO removes the requirement for BIS/ISI marking on refined zinc, reducing procurement costs and broadening the supplier pool. The withdrawal is expected to encourage more overseas participation and enhance price competitiveness for galvanisers and alloy producers.

How does decision affect nickel & stainless steel?

The government has withdrawn the Refined Nickel QCO (2025), reversing the certification mandate introduced in April. This eases sourcing for stainless steel melt shops, speciality alloy producers and battery-precursor manufacturers. India is fully import-dependent on refined nickel: volumes rose 88% in 2024 to 207,800 t, then January-October 2025 witnessed a 24% y-o-y fall to 145,466 t.

The stainless-steel flat-rolled QCO, however, remains in force. Imports of hot-rolled (HR)/cold-rolled (CR) stainless flat products from China and other suppliers will therefore continue to face restrictions at least until Q2CY’26, with closer monitoring through the SIMS portal. Stainless flat imports stood at 706,300 t during January-September 2025, down 6% y-o-y. Most established exporters already comply with BIS requirements, so the immediate impact is limited, though the withdrawal of the nickel QCO should improve overall raw-material flexibility for mills, as per market participants.

Will tin market stabilise?

Refined tin imports stood at 13,500 t in CY’24, up 11.6% from the previous year.

Tin refiners had largely avoided India due to BIS compliance requirements, leading to irregular shipments for solder manufacturers and electronics component makers. The rollback is expected to restore steady supply, relieve cost pressures, and improve planning visibility across the electronics value chain.

Outlook

The removal of all major base-metal QCOs is expected to ease supply pressures rapidly, supported by faster customs clearance, renewed participation from overseas producers and lower compliance-related costs. Downstream sectors — from electricals to infrastructure and mobility — should see more stable raw-material availability and more competitive procurement as demand accelerates through 2026. The policy shift positions India for improved supply-chain resilience and reduces the risk of import-driven volatility during the next phase of industrial and infrastructure expansion.

Leave a Reply