- Brazil lifts exports as weather-related disruptions subside

- Firm Capesize rates, Chinese restocking support freights

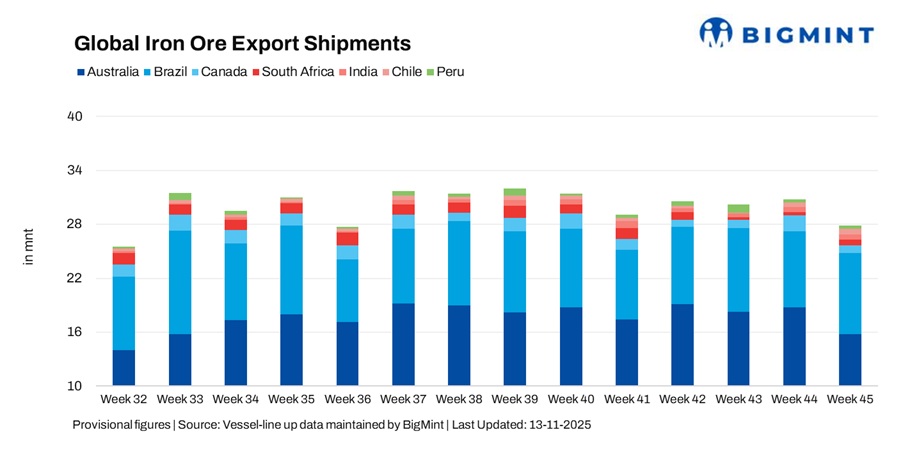

Global iron ore exports declined 9% to 27.80 million tonnes (mnt) in week 45 (01-07 November 2025) from 30.70 mnt in week 44 (25-31 October), as a sharp drop in Australian shipments outweighed moderate gains from Brazil, India, Chile, and South Africa. While overall trade activity slowed, freight market sentiment improved, with firm Capesize rates and steady restocking demand from China offering some support to vessel utilisation.

Despite steady buying interest ahead of winter, muted steel output and high port inventories in China continued to weigh on seaborne demand, curbing export momentum from key suppliers. Softer Australian loadings and logistical constraints in Canada further contributed to the weekly decline.

Australia’s shipments fall on weak chartering

Australia’s iron ore exports fell 16% w-o-w to 15.77 mnt in week 45 from 18.82 mnt a week earlier, marking the lowest level in four weeks. Reduced vessel turnaround at key Pilbara ports and selective scheduling by major miners weighed on overall throughput. Loadings from Port Hedland (10.45 mnt), Walcott (2.69 mnt), and Dampier (2.45 mnt) reflected a slowdown in activity, while operational adjustments and slower chartering amid ongoing maintenance cycles further curtailed shipments.

Among major miners, BHP (6.12 mnt), Rio Tinto (5.13 mnt), and FMG (3.18 mnt) collectively accounted for the majority of exports. On the destination side, China remained the principal buyer with 13.26 mnt, while shipments to South Korea (1.36 mnt) and Japan (0.96 mnt) stayed broadly stable. Firmer freights and higher bunker costs added mild cost pressures, discouraging incremental loadings during the week.

Brazil’s exports rebound, rising freights add pressure

Brazil’s iron ore exports rose 8% w-o-w to 8.99 mnt from 8.35 mnt, recovering from weather-related disruptions seen in late October. Improved performance at Ponta da Madeira (3.83 mnt), Tubarao (2.22 mnt), and Itaguai (1.70 mnt) supported the rebound, reflecting smoother port operations and stronger vessel turnaround. Among key miners, CSN (3.92 mnt) and Vale (3.83 mnt) increased their loading pace amid steady Chinese restocking.

China remained the major buyer, taking 3.42 mnt, followed by Oman (0.51 mnt), Malaysia (0.39 mnt), and Bahrain (0.34 mnt). The uptick reflected renewed miner activity and firmer demand for high-grade fines, with some cargoes also directed toward Europe. Despite improving volumes, high freights on long-haul routes kept some buyers cautious, slightly tempering overall momentum.

Canadian volumes ease after prior spike

Canada’s iron ore exports halved to 0.87 mnt, down 52% w-o-w from 1.79 mnt, as logistical congestion and vessel delays at Quebec’s ports slowed loading activity. Loadings from Sept-Iles (0.51 mnt) and Port Cartier (0.36 mnt) reflected reduced throughput after a strong rebound in week 44 when miners had cleared earlier backlogs.

Among major shippers, AM/NS (0.36 mnt), IOC (0.34 mnt), and Guinea and Nimba Mines (0.17 mnt) accounted for most of the week’s volumes. Lower rail wagon availability and adverse weather curtailed dispatches, with the majority of shipments headed towards European destinations. The US was the largest importer (0.18 mnt), followed by Algeria (0.17 mnt) and the Netherlands (0.16 mnt). Although freight sentiment strengthened, higher voyage costs limited new bookings, keeping overall export activity subdued.

South Africa sees steady recovery

South Africa’s iron ore exports increased sharply by 60% w-o-w to 0.61 mnt from 0.38 mnt, supported by improved rail movement and stronger loading performance at Saldanha Bay (0.53 mnt) and Richards Bay (0.08 mnt). Easing congestion at key terminals aided vessel scheduling, while Chinese demand for medium-grade ore remained stable.

The Netherlands emerged as the leading importer, taking 0.35 mnt, followed by China (0.19 mnt). However, operational constraints and intermittent rail delays continue to pose challenges for a sustained recovery in the coming weeks.

India’s shipments continue amid active Chinese restocking

India’s iron ore exports rose 22% w-o-w to 0.58 mnt from 0.47 mnt, driven by stronger loadings from Dhamra (0.24 mnt) and Paradip (0.18 mnt) ports. Odisha-based miners increased shipments amid improved vessel turnaround and steady Chinese buying interest.

However, exporters faced rising freight costs on Supramax routes, which slightly narrowed margins despite higher overseas demand. China remained the primary destination, importing 0.20 mnt, while the limited availability of high-grade ore continued to cap further growth in export volumes.

Chile, Peru show mixed trends

Chile’s iron ore exports rose 12% w-o-w to 0.55 mnt, maintaining upward momentum as improved weather conditions supported loadings at Totoralillo (0.34 mnt) and Huasco (0.20 mnt) ports. China remained the sole major buyer, taking in the entire 0.55 mnt of shipments.

In contrast, Peru’s shipments edged 3% lower w-o-w to 0.43 mnt, weighed down by operational slowdowns and limited vessel availability at San Nicolas (0.36 mnt) and Matarani (0.08 mnt). Shougang Hierro maintained steady dispatches of 0.36 mnt, though weaker logistical performance capped overall throughput. China was the primary importer, accounting for 0.39 mnt of total exports.

Firmer Capesize demand underpins bullish freight sentiment

The iron ore freight market strengthened this week, buoyed by firm Capesize demand, limited vessel availability, and active Chinese restocking ahead of winter. Higher rates on long-haul routes reflected improving vessel utilisation, particularly from Australia and Brazil, while steady demand on shorter routes such as India-China kept Supramax rates broadly stable.

The firmer freight environment encouraged prompt chartering but also raised voyage costs for exporters, mildly constraining shipment volumes. Rising bunker prices and tightening tonnage supply further reinforced bullish freight sentiment, highlighting a cautiously firm near-term outlook, led by the Capesize segment.

Outlook

Global iron ore trade is likely to stay steady in the near term, supported by Chinese restocking that continues to drive exports from Brazil and India. However, elevated freights, weaker Australian shipments, and subdued Chinese steel margins may cap further gains. Shipment trends through mid-November will depend on seasonal factors and port performance, while strong freight market dynamics influence miners’ scheduling. Meanwhile, Guinea’s Simandou project, which began operations at the beginning of the week, is expected to gradually lift the overall export volumes on a global level.

Leave a Reply