- Mills running at low 35-40% capacity utilisation rates

- Currency weakness, inflation raise production costs

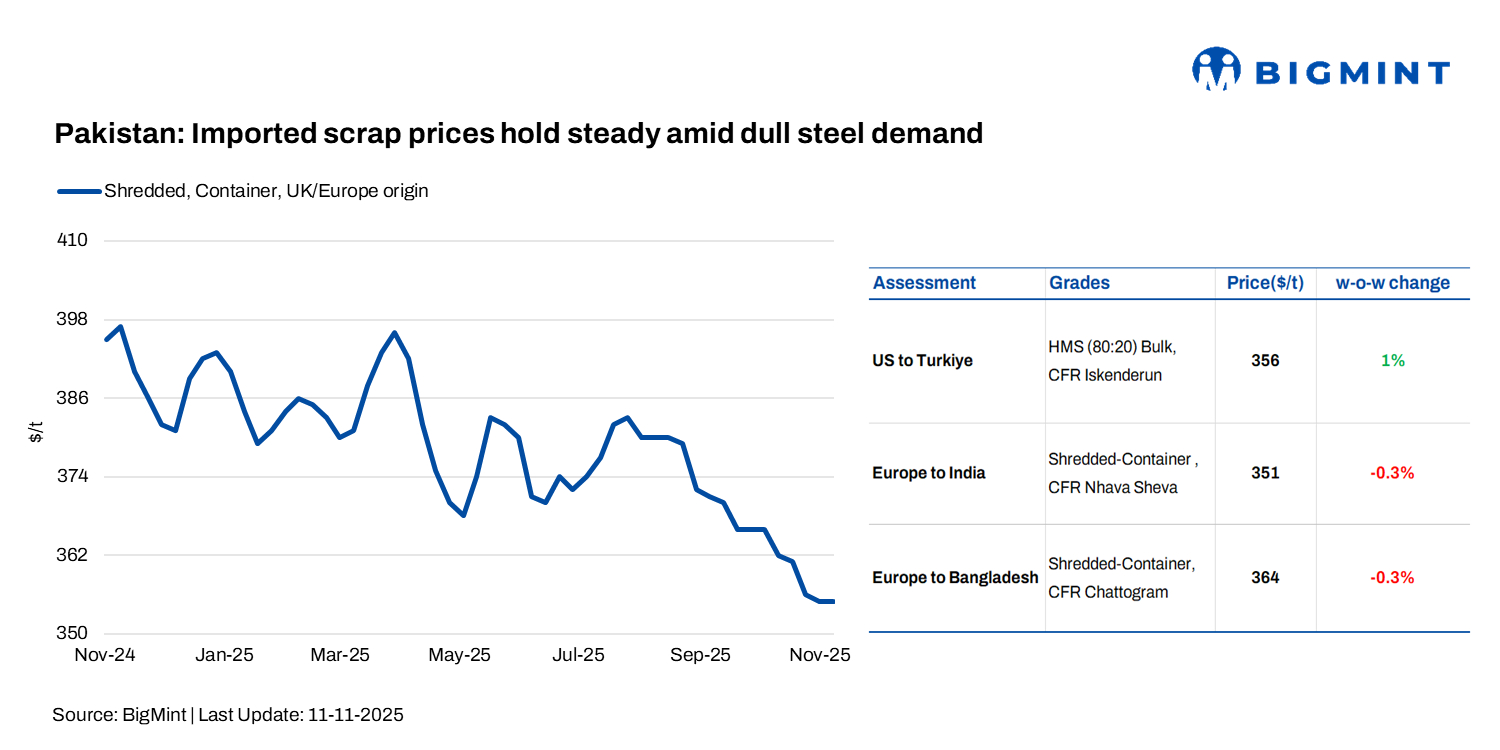

Pakistan’s imported shredded scrap prices held steady w-o-w at $355-356/t CFR, with European/UK-origin shredded assessed at $355/t CFR Qasim and recent deals concluded near $355-358/t. UAE-origin scrap also stayed firm, with HMS at $340/t, sheared HMS at $345-348/t, and fabrication scrap at $350-355/t.

The steel market continued to struggle amid weak fundamentals. Some mills booked Middle East parcels for quick deliveries, lending mild support to prices. Finished steel sales improved slightly from October, while discussions between the government and industry representatives continued, focusing on long-awaited reforms to revive the struggling steel sector. Steel mill margins were also under pressure, with a depreciating currency and inflation raising production costs.

Around 5,000-6,000 t of shredded scrap were booked from the UK, Sweden and other European regions at $355-363/t on a CFR Qasim basis.

As per market insiders, Nigar scrap (similar to shredded scrap) was recently purchased at PKR 138,600/t ($490/t), though scrap availability remained tight in the local market, with hopes for improvement ahead.

Rebar was traded at PKR 220,000/t ($778/t), billet at PKR 190,000/t ($672/t), bala at PKR 177,000/t ($626/t), and local scrap at PKR 135,000-140,000/t ($478-496/t). Mills operated at 35-40% capacity utilisation, with no significant recovery yet.

Shipbreaking: Weak fundamentals and HKC delays weigh on market confidence.

Outlook

Pakistan’s scrap and steel markets are likely to remain subdued in the near term amid weak demand, liquidity challenges, and slow capacity utilisation. While limited bookings and government-industry talks may provide brief support, a sustained recovery will depend on improved domestic liquidity, policy clarity, and a revival of seasonal demand towards the year-end.

Leave a Reply