- Rising secondary production reduces need for imports

- Scrap turns cost-effective as LME lead prices decline

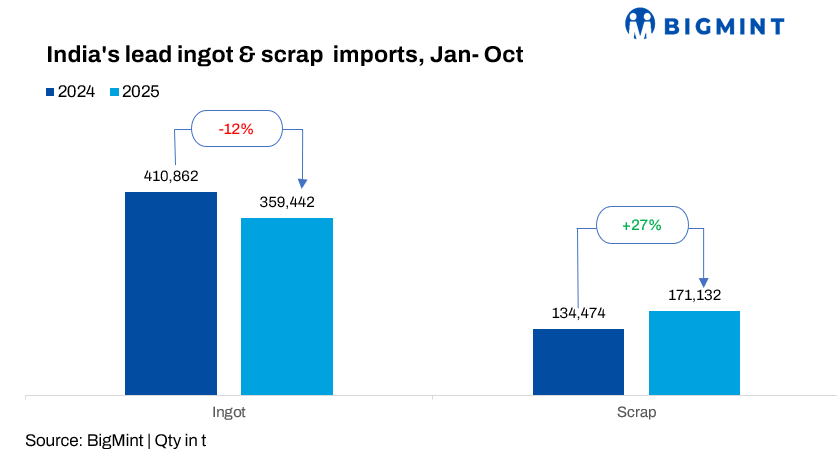

India’s semi-finished lead ingot imports fell 12% y-o-y to 359,314 tonnes (t) during January-October 2025, compared with 410,862 t in the corresponding period of 2024. The fall was driven by weaker shipments from major suppliers such as South Korea, Malaysia, Japan, and the Philippines, amid subdued downstream battery-sector demand and higher domestic availability.

Additionally, lead scrap imports increased by 27% y-o-y to 171,132 t in January-October 2025, driven by a decline in London Metal Exchange (LME) prices, which made scrap more cost effective.

Imports from South Korea, Malaysia decline

Among suppliers, South Korea remained India’s largest source, but imports dropped 57% y-o-y, to 59,854 t in January-October 2025 from 140,647 t in the year-ago period, amid lower refinery dispatches and competitive regional pricing.

Malaysia, the second-largest source, saw volumes fall 18% to 63,722 t, while Indonesia and the Philippines also experienced declines of 7% and 15%, respectively.

In contrast, the United Arab Emirates (UAE) stood out as an emerging source, with imports rising to 37,718 t in January-October 2025 from 18,216 t in the year-ago period, reflecting growing re-export activity through Gulf trade hubs.

What led to a drop in lead ingot imports?

- India’s secondary lead production rose by an estimated 6-8% y-o-y in 2025, supported by increased scrap collection and steady smelter operations in Tamil Nadu, Gujarat, and Uttar Pradesh. With lead scrap imports increasing y-o-y, recyclers had ample feedstock, reducing the need for semi-finished imports.

- Lead demand from battery and cable manufacturers softened due to slower EV battery replacement and weaker construction activity. Domestic lead consumption grew only 1-2% y-o-y during January-September 2025, compared with 5% growth in 2024, curbing import requirements.

- Average LME lead prices eased to $2,040/t in mid-2025 from $2,230/t in 2024, narrowing arbitrage margins. Meanwhile, container freights from East Asia to India rose 20-25% early in 2025 due to Red Sea diversions, hurting landed cost competitiveness.

- The government’s enhanced customs scrutiny on non-ferrous metal imports and shorter credit cycles from trade financiers affected working capital for smaller importers. Several mid-sized traders temporarily halted bulk imports to avoid documentation delays and margin pressures.

- Importers increased sourcing of lead scrap and refined lead from the UAE, which offered lower duty structures and higher resale flexibility.

Outlook

Lead import volumes are expected to stabilise in late 2025, supported by steady demand from the battery and cable sectors. However, total 2025 arrivals are projected to remain 20-25% lower than 2024 levels, given subdued demand from OEMs and high domestic inventory levels. A rebound is likely in early 2026 as regional lead prices normalise and restocking resumes.

Leave a Reply