- Limited output, stockouts lead to supply crunch

- China prices steady despite weak steel demand

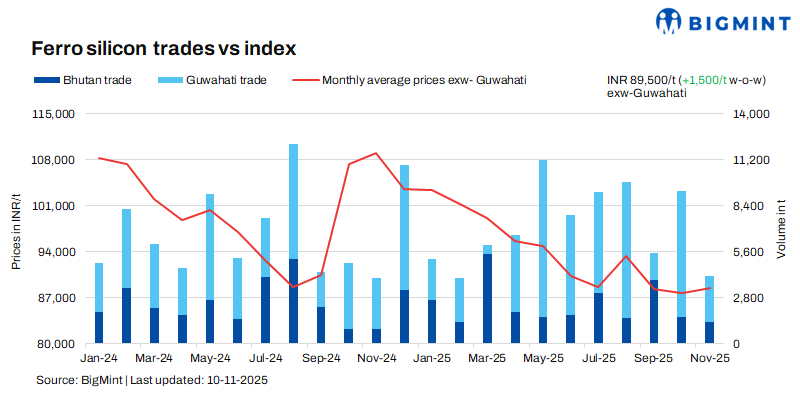

Indian ferro silicon (70%) prices increased by INR 1,500/tonne (t) ($17/t) as compared to the previous assessment on 3 November. Most sellers raised their offers due to a slight supply crunch, as some key suppliers in Bhutan ran out of stock. Additionally, active trades were concluded, which boosted sellers’ confidence.

As per BigMint’s assessment on 10 November, ferro silicon prices in India were at INR 89,500/t ($1,009/t) exw-Guwahati. In Bhutan as well, prices increased by INR 1,000/t ($11/t) w-o-w to INR 89,000/t ($1,003/t) exw. Deals for around 3,700 t were concluded last week in both regions, mainly within the price bracket of INR 87,000-90,000/t ($981-1,015/t) exw.

Market summary (4-10 November 2025)

Tight supply keeps prices elevated: Ferro silicon prices in Bhutan opened at INR 88,000/t ($992/t) exw for the month, with most deals concluded around this level. However, several key plants quickly ran out of stock, while some shifted focus to exports, resulting in a mild supply crunch in the domestic market. In South India too, production of 70-grade material remained limited, pushing market offers up to INR 90,000/t ($1,015/t) exw. Despite these supply constraints, buyers continued to resist price hikes.

A Bhutanese seller told BigMint, “All suppliers are trying their best to increase prices, but customers are very sensitive and resisting higher offers.” This reflects the prevailing cautious market sentiment, with rising prices due to tight availability somewhat countered by limited buyer acceptance.

Chinese prices remain flat w-o-w: Ferro silicon (Si: 75%) prices in China remained steady w-o-w at RMB 5,800/t ($815/t) exw-Inner Mongolia, as rising semi-coke and electricity costs increased production expenses, prompting producers to maintain firm prices and avoid further cuts.

However, weak demand from steel mills, slow bidding activity, and limited trader participation kept market sentiment subdued, limiting any upward movement. Although the volatile futures market provided some support, environmental policies and steel mill maintenance also influenced sentiment. Overall, the market remained largely stable, with these factors collectively resulting in a market stalemate.

Meanwhile, according to Mysteel Global, China’s ferro silicon output in October increased by 3.5% m-o-m to a 10-month high of 505,338 t, resulting in a 17% rise in smelter inventories. The combination of higher supply and weak demand weighed on market sentiment, leaving many smelters operating at a loss. With steel demand expected to decline during the winter months, the likelihood of a near-term price recovery remained limited.

ZCE futures edge up w-o-w: Ferro silicon futures on China’s Zhengzhou Commodity Exchange (ZCE) for January 2026 delivery inched up by RMB 62/t ($9/t) w-o-w to RMB 5,588/t ($785/t) on 10 November, from RMB 5,526/t ($776/t) on 3 November.

Outlook

Although suppliers have raised their offers, the sustainability of those in the coming days will largely depend on buyers’ acceptance of higher tags.

Leave a Reply