- A few major mills hike HRC, CRC list prices, others keep tags unchanged

- Some Tier-1 mills hike BF rebar list prices for Nov, buyers tread cautiously

- Raw material prices show uptrend, demand in trade channel still lags

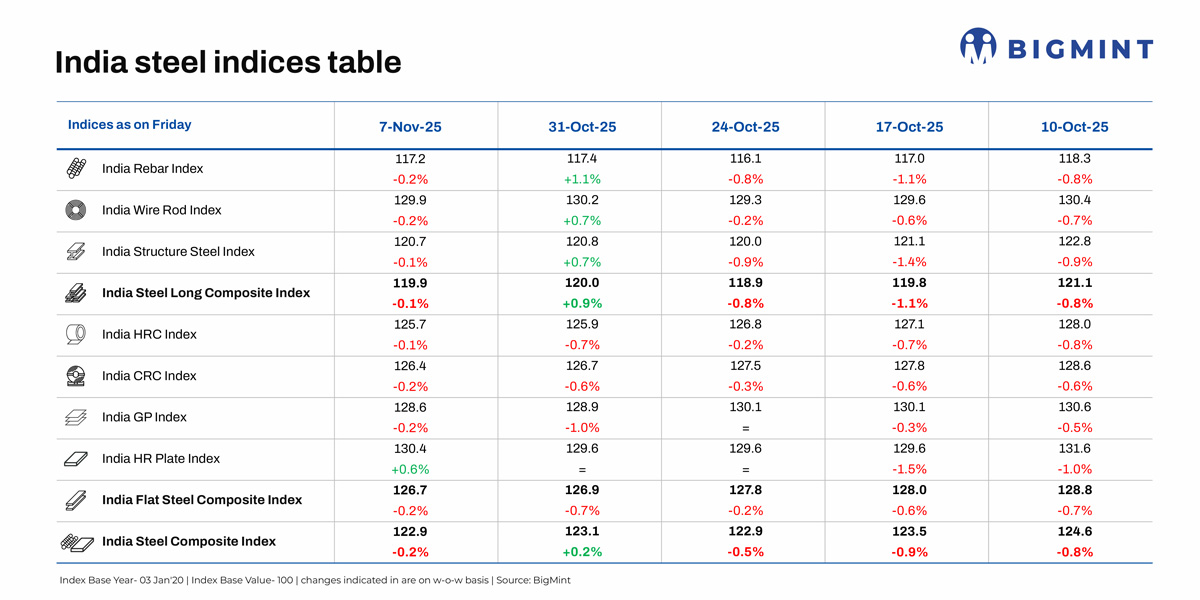

Morning Brief: BigMint’s flagship India steel composite index, a barometer of the domestic steel market, edged down by 0.2% w-o-w as assessed on 7 November 2025. After recording a slight uptick last week following 11 weeks of successive decline the composite index edged back again into negative zone amid uncertainty about price direction prevailing in the domestic steel market.

The flat steel composite index fell 0.2%, with the HRC index recoding a marginal 0.1% drop. However, the HR plate index trended up w-o-w on demand improvement. The rebar index fell 0.2% after showing a marked improvement last week. The market is treading cautiously following the list price hikes announced by some of the primary producers.

Highlights of price movements

HRC, CRC record marginal decline: BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) inched down by INR 300/t to INR 47,300/t ($544/t) on 7 November 2025 against INR 47,600 on 4 November. CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 2500/t to INR 55,300/t on 7 November against INR 55,500/t on 4 November. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Leading steelmakers have HRC and CRC prices by INR 1,250/t for November sales compared with late-October levels. However, one major producer has opted to keep prices unchanged. M-o-m, trade-level HRC prices fell by INR 1,200/t ($9/t) to INR 47,900/t ($553/t) in October from INR 49,100/t ($562/t) in September.

Mills had to take a price hike due to the sustained firmness in domestic iron ore prices amid tightening availability and the rise in imported coking coal prices. The average price of Australian-origin premium HCC stood at around $197/t in early November against a monthly average of $191/t in October.

Post-Diwali, participants have returned to the market and optimism is growing after some mills announced price hikes for November.

Moreover, India’s finished steel exports increased by 9.6% m-o-m to 0.640 mnt in October from 0.584 mnt in September and 45% y-o-y from 0.442 mnt in October 2024. Likewise, imports during April-October 2025 were 3.804 mnt, a decrease of 34.1% compared to 5.768 mnt in the same period last year. Higher exports will provide an impetus to domestic production and prices while lower imports shows the impact of trade remedial measures undertaken by India.

Mixed signals in rebar market: The blast furnace (BF) rebar market witnessed mixed pricing signals in early-November. Some leading primary mills increased rebar prices by up to INR 1,250/t ($14/t) for early-November deliveries as against those prevailing in end-October. Meanwhile, others rolled over their prices against previous levels.

Trade-level BF rebar prices rose by INR 500/t ($6/t) w-o-w to INR 47,800/t ($539/t) exy-Mumbai, as per BigMint’s assessment on 7 November. Prices are exclusive of GST at 18%. Demand remained sluggish in the trade channel in October owing to the festive season and the extended monsoon. Rebar inventories at Tier-1 mills increased by 15% m-o-m in early-November, sources informed.

Trade-level IF rebar tags witnessed an m-o-m drop in October. Early gains, driven by stronger semi-finished steel prices and improved bookings, were offset by subdued trading ahead of the festive season. High inventories of 12-15 days and cautious market sentiment persisted, prompting some manufacturers to offer discounts to sustain sales. Rebar prices dropped by INR 1,900/t ($21/t) m-o-m to a monthly average of INR 42,200/t ($476/t) exw-Mumbai in October.

Outlook

The domestic steel market is likely to stay stable in the near term, supported by steady production, and firm consumption trends driven by increased construction and infrastructure activity in the near term. However, export momentum may soften amid weaker global prices, while imports are expected to remain limited due to safeguard duty and lower domestic prices compared with the cost of landed imports.

Near-term supply pressure due to maintenance and repair breaks undertaken by some major mills at blast furnace facilities or strip rolling lines may provide some support to flat steel prices. Sentiment is positive in the longs segment, too. However, buyers are treading cautiously following the list price hikes announced by some major mills.

Leave a Reply