- LME lead inventories decline by 6% w-o-w

- MCX tags close higher, tracking global cues

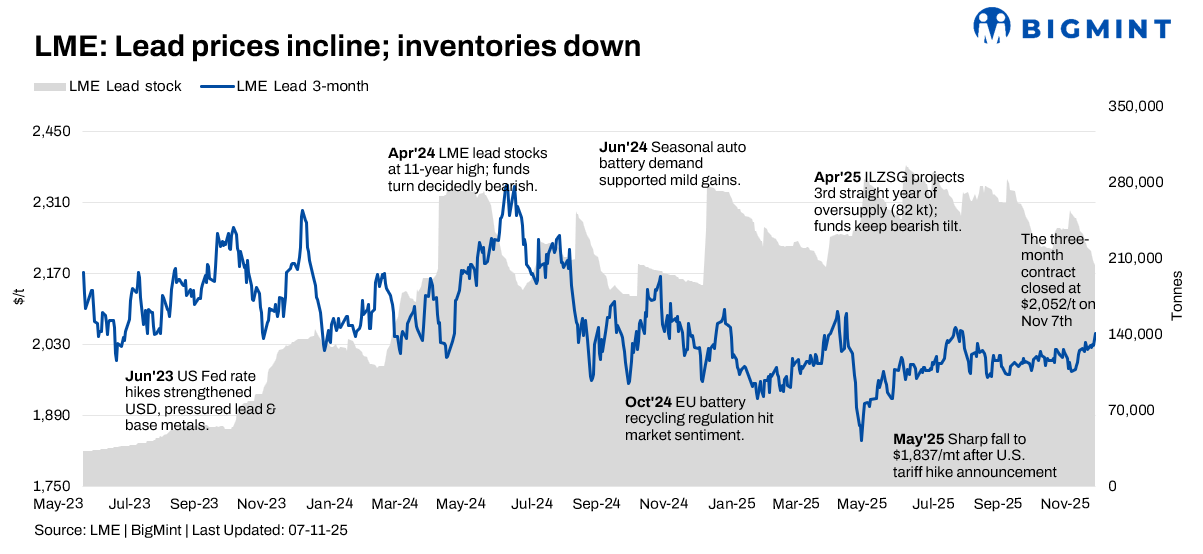

The global lead market experienced fluctuations during Week 44, with prices closing higher. Prices on the London Metal Exchange (LME) dipped mid-week before ending higher, supported by tightening LME inventories. Overall, the global market was influenced by conflicting signals from inventory movements, macroeconomic data, and regional supply dynamics.

Price trends

Overall, LME lead cash-settlement prices edged up during the week, with a notable mid-week dip followed by a late-week rebound. Prices opened the week at $1,995/t on 3 November and were at $2,045/t on 7 November. This represents a w-o-w increase of approximately 2.50% for the cash price. The three-month contract mirrored this movement, starting at $2,024/t and ending at $2,052.50/t.

Inventory analysis

LME lead inventories saw a significant decline in the latter half of the week, reaching multi-month lows. Initially, there were increased expectations for LME shipments to delivery warehouses, which weighed on prices at the start of the week. Late-week, a significant decline in LME lead inventory was a major factor contributing to the late-week price rebound, reaching 203,700 t by 7 November, down 6% from 216,800 t on 3 November.

MCX lead trends (3-7 November)

MCX lead prices reflected the volatile global sentiment and domestic factors. The MCX lead contract for the November expiry closed at INR 184,850/t on 3 November and closed higher at INR 185,400/t on 7 November, marking an increase of 0.22% over the week. Indian prices were influenced by global cues and domestic factors, including rupee fluctuations and demand signals.

SHFE lead trend

SHFE lead prices maintained a fluctuating trend but showed some strength during the week. The most-traded SHFE lead 2512 contract opened at RMB 17,390/t on 3 November, briefly touching a low of RMB 17,350/t before fluctuating upward and finally settling at RMB 17,475/t on 7 November. This represents a w-o-w increase of 0.49%. Trading sentiment rebounded, and the expansion of spot discounts in eastern China halted, suggesting some underlying strength.

Amara Raja reports strong Q2FY’26 performance; cell plant on track

Amara Raja Energy and Mobility Ltd. posted consolidated revenue of INR 34,670 million in Q2FY’26, up 6.6% y-o-y, with profit before tax at INR 406 crore. Export sales rose to INR 4,919 million from INR 3,821 million in Q1, driven by robust demand in overseas markets. The company’s Customer Qualification Plant (CQP) for lithium-ion cell manufacturing under its new energy division is progressing well and is expected to become operational by Q4FY’26, marking a key milestone in India’s clean energy transition.

Outlook

The near-term lead outlook is mixed. The late-week rebound, driven by inventory declines and a strong close in SHFE, suggests some underlying strength. However, the market remains sensitive to broader economic signals and inventory movements, with volatility expected. The outcome of ongoing macroeconomic events will continue to influence market direction.

Leave a Reply