- GCC mills switch to rebar production amid muted billet sales

- CIS producers eye semis exports to balance domestic slowdown

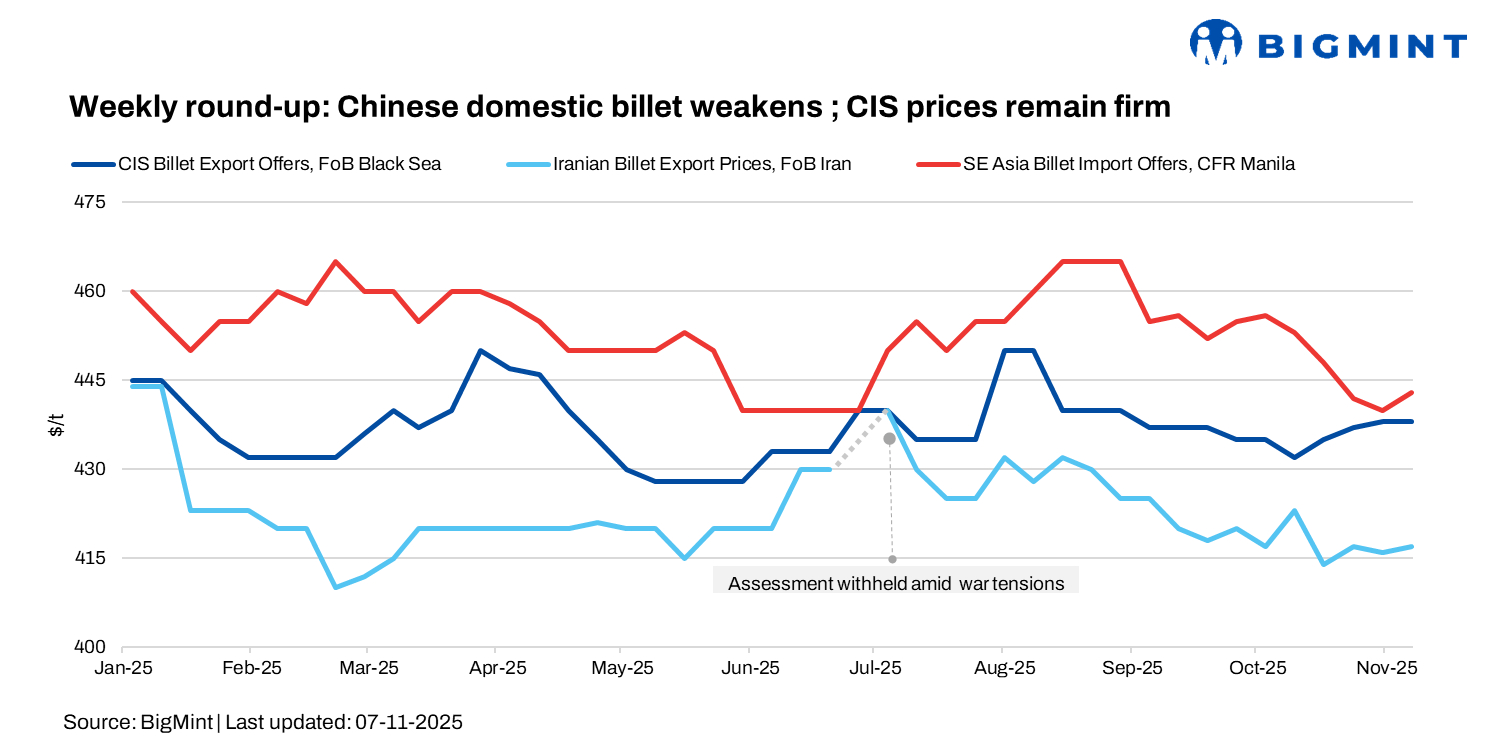

The global billet market remained mixed in week 45, with modest gains across Asia and the Middle East, while CIS and Turkiye stayed range-bound. Russian exporters held billet offers steady at $440-445/t FOB Black Sea, while domestic prices in China softened.

In Turkiye, the imported scrap market slowed after early-week activity, with 8-9 new bookings heard. While mills increased domestic scrap purchase prices to secure tonnage, scrap exporters remained firm, citing limited supply, high freights, and the approaching winter. US-origin HMS 80:20 was at around $355-356/t CFR Turkiye.

Local scrap mirrored import trends, rising TRY 100-300/t ($3-5/t). Lira depreciation caused a $2/t decline in dollar-based tags, as limited imports and high costs pushed mills to adjust local prices.

Market updates

CIS

CIS billet suppliers from the Black Sea region maintained export prices at $440-445/t FOB Black Sea, holding off earlier plans for an upward adjustment. Russian shipments were mostly scheduled for late December to early January, with some Ural mills already offering for January.

In Turkiye, Russian billet was assessed at $455-460/t CFR ($435-440/t FOB), while Donbas material stood at $450-455/t CFR ($430-435/t FOB). Buyers deemed these offers high, especially as Chinese semis traded at $455-457/t CFR, resulting in no confirmed deals this week.

Amid limited transactions and firm scrap costs, CIS billet export prices remained stable. Producers also considered diverting output toward semi-finished exports due to a domestic slowdown, with Black Sea billet at $440-445/t FOB. This may support domestic prices if Russian demand improves in December.

Asia

Saudi Arabia: The billet market stayed muted despite a mild uptick in rebar prices, as mills focused on rebar production to offset elevated scrap costs and sustain margins. Domestic billet offers hovered at SAR 1,790-1,800/t ($477-480/t) exw, though buying activity remained sluggish amid weak long steel demand.

Scrap prices have been largely stable since late October at SAR 1,380-1,400/t ($368-373/t) in major regions. Imported billets remained unviable, with Chinese semis last offered near $460/t CFR.

Rebar prices firmed further, with leading mills transacting at SAR 2,045/t ($545/t) delivered, while second-tier producers targeted SAR 2,025-2,050/t ($540-547/t).

UAE: The UAE billet market remained divided this week as suppliers held firm on prices, supported by strong rebar sales, while buyers resisted current levels to maximise margins. Billet offers from a merchant producer in the UAE stood at $480-490/t CPT and from Qatar at $490-500/t CFR, while buyers targeted $460/t CFR and below. Around 50,000 t of 3sp billet were recently booked at $465/t CFR for December shipment.

Sellers showed little concern over slower bookings, redirecting billet output toward rebar production, which continued to yield better margins. Indonesian billet offers stood at $435-440/t FOB ($455-465/t CFR UAE), while volatility in China’s billet market added uncertainty. To secure feedstock, UAE mills have resorted to increasing domestic scrap procurement by around 50,000-55,000 t/month and DRI sourcing from Qatar.

Iran: Billet export activity stayed weak in early November amid sluggish global demand, increased competition, and new sanctions disrupting trade flows. Offers were heard at $415-420/t FOB for December shipment, with some traders quoting as low as $405-410/t FOB. Buyers remained cautious due to oversupply from other origins and sanctions-related risks.

IF-based mills also struggled with exports as demand from Iraq and Afghanistan weakened. Meanwhile, slab exports showed better traction at $410-412/t FOB, while rebar prices held steady at $400-410/t exw.

Iran’s Khorasan Steel Complex (KSC) is set to construct a 60 MW solar power plant in Neyshabur to secure a stable energy supply and reduce reliance on the national grid. During H1 of the current Persian year (21 March 2025 -22 September 2025), Khorasan Steel’s billet output rose 11 % y-o-y to 0.47 mnt, long steel by 6% to 0.3 mnt, and pellet production by 8% to 0.96 mnt.

China: Chinese billet prices declined by RMB 40/t w-o-w to RMB 2,940/t ($413/t), while SHFE January 2026 rebar fell by RMB 76/t w-o-w to RMB 3,030/t ($426/t). The market faced pressure from weakening construction demand, high raw material inventories, and subdued futures.

Mills trimmed output to manage costs, with occasional speculative buying providing short-term support. Positive cues from fresh infrastructure investments and policy measures offered mild optimism, but overall sentiment remained cautious. Export offers stayed largely unchanged, with stable demand from the Middle East and Africa.

Chinese exporters held firm at over $455-460/t CFR for 3SP-grade billet, while buyers remained near $440-445/t CFR.

Leave a Reply