- HRC prices rise as trade activity resumes post-holidays

- BF rebar market sees mixed pricing signals in early Nov

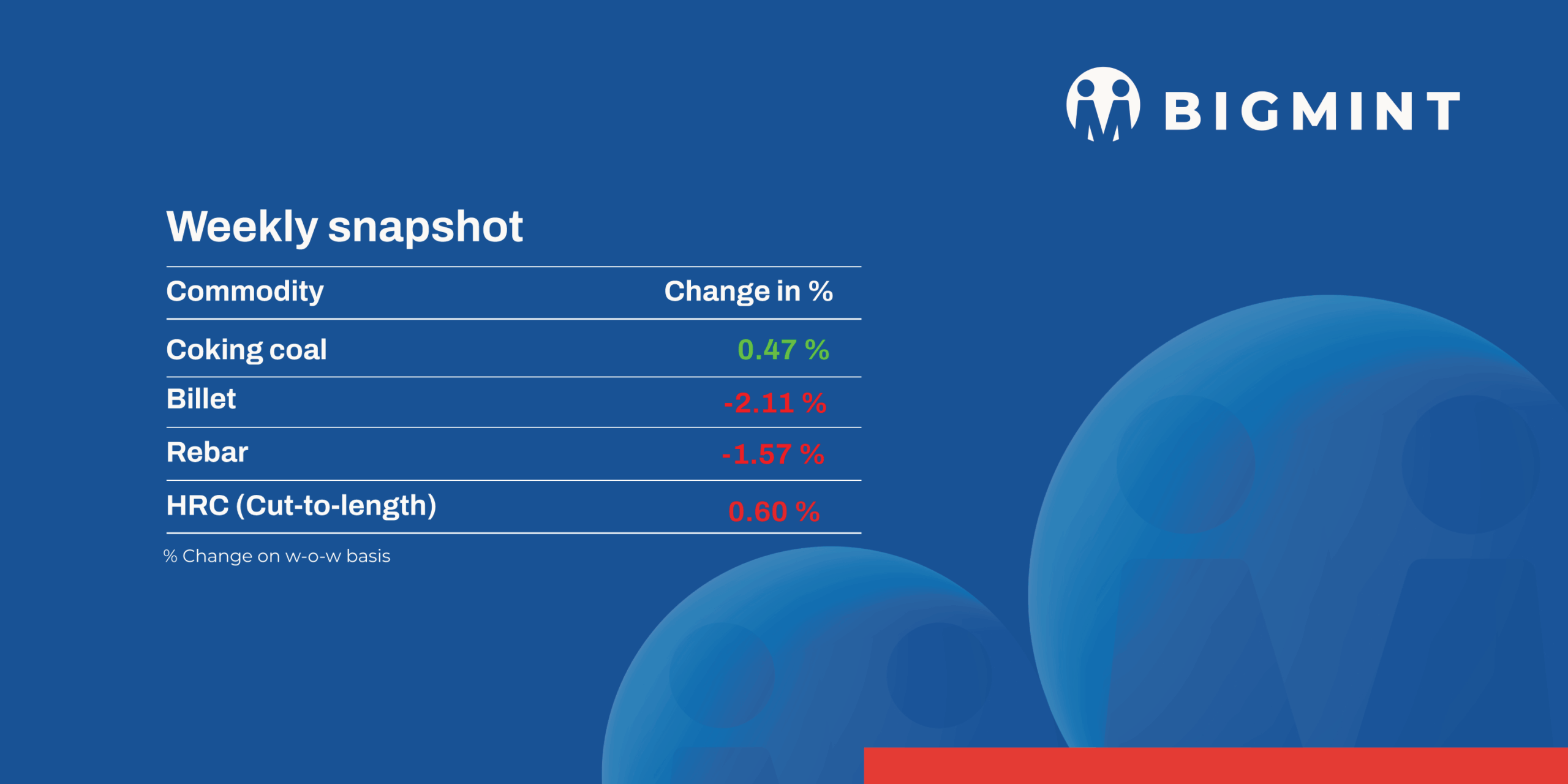

The domestic steel market saw negative trend in prices during week 45 ( 3-7 Nov, 2023). Semi-finished steel prices dropped in the range of INR 50-700/tonne (t). Trade-level blast furnace (BF) rebar prices also gained w-o-w, reflecting improving market sentiment.

Iron ore, pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained largely stable at INR 10,000/t ($113/t) DAP on 7 November. Buyers concluded deals for around 15,000 t from both local and Odisha-based pellet suppliers. Raipur-based pellet producers kept their offers for Fe 63 (+/-0.5%) material at INR 9,800-10,200/t ($111-115/t) exw.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $1/t w-o-w to $71/t FOB east coast on 6 November. Meanwhile, the index stood stable w-o-w at $81/t CFR China. Around 55,000 t of Fe 57% iron ore fines were heard sold at $71/t FOB Paradip, while a few other deals were heard under negotiation. Exporters mentioned that discounts for Fe 57% fines averaged 15-16% against the benchmark index.

- BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index fell by $4/t w-o-w to $102/t FOB east coast on 5 November. Pellet prices dipped, as the domestic market remained more attractive. Consequently, no fresh deals were heard in this window.

Coal

- South African portside thermal coal offers in India were largely unchanged w-o-w, with RB2 (5500 NAR) at INR 8,200/t and RB3 (4800 NAR) at INR 7,100/t across Paradip, Vizag, and Gangavaram. Weak buying led traders to divert cargoes to South Korea and Sri Lanka. Overall sentiment remained subdued due to declining sponge and semi-finished market prices.

- Domestic coal prices stayed stable w-o-w, with 5,000 GCV assessed at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. SECL will auction 238,500 t of non-coking coal on 13 November, mainly G6-G9 and G12 grades. Limited auction volumes could mildly support prices, though sluggish steel demand may restrict any sharp gains in the near term.

- BigMint’s premium hard coking coal (PHCC) index rose by $1/t w-o-w to $211/t CNF Paradip on 7 November, supported by firm Chinese demand. Traders noted Australian offers at $211-212/t CFR India, while bids stayed $3-4/t lower, leaving deals unconfirmed. Indian steel mills continued cautious buying as prices followed Chinese trends.

- Met coke prices in eastern India rose to a 6-month high at INR 31,000/t ex-Jajpur, supported by limited supply and higher coking coal costs. Improved trading and fresh tenders tightened merchant availability in the east, while western markets stayed steady.

Ferrous scrap

- India’s imported ferrous scrap market remained subdued throughout the week, with limited buying interest from mills. Offers for shredded scrap hovered around $350-355/t CFR and HMS 80:20 at $325-330/t, while workable bids were $5-10/t lower.

- Falling sponge iron prices and steady domestic scrap availability continued to weigh on import appetite. Mills found imported scrap less competitive compared with local material, leading to subdued bids for UK, European, Brazilian, and African-origin HMS. Buyers and sellers appeared unwilling to take risks, reflecting a market under pressure from both local and global steel trends.

- Approximately 7,250 t of imported ferrous scrap were booked for India, including 3,000-4,000 t of shredded at $350-355/t, 1,500-2,000 t of HMS 80:20 at $322-330/t, with the remaining volumes comprising LMS, PNS, and NTP.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices remained mostly stable with a slight dip of INR 50/t ($1/t) w-o-w to INR 71,800-72,000/t ($810-812/t) in Durgapur, Raipur, and Vizag. The minor decline was mainly due to limited spot demand and cautious buying sentiments, despite restricted supply from key producers.

- Ferro manganese: Indian ferro manganese (HC 70%) prices went up by INR 1,200/t ($14/t) w-o-w to INR 73,200/t ($826/t) exw-Durgapur, while prices also rose by INR 1,000/t ($11/t) w-o-w to INR 73,100/t ($825/t) exw-Raipur. The increase was primarily driven by supply shortages in the domestic market.

- Ferro silicon: Indian ferro silicon (Si 70%) prices were mostly steady with a slight decline of INR 300/t ($3/t) w-o-w to INR 87,700/t ($989/t) exw-Guwahati, while Bhutan’s prices stood at INR 88,000/t ($993/t). The slight dip followed the announcement of Bhutan’s November offers at INR 88,000/t ($994/t) exw, which reflected softer market sentiment.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices declined by INR 1,500/t ($17/t) w-o-w to INR 117,500/t ($1,326/t) exw-Jajpur. Prices fell, as the stainless steel market was under pressure amid the resumption of imports following the relaxation of BIS norms. Prices of 304-grade stainless steel hot-rolled coils (HRCs) declined by INR 2,000/t ($23/t) w-o-w to INR 184,000/t ($2,076/t) exw-Mumbai.

Semi-finished steel

- India’s semi-finished steel market witnessed downward movement this week, as per BigMint’s assessment. Domestic billet prices across major regions decreased by INR 50-700/t ($0.5-8/t) on a w-o-w basis, Despite the mild recovery last week, buying activity remained limited, as most bookings were concluded in the previous week. The decrease in spot offers, coupled with subdued finished steel demand, prompted market participants to adopt a cautious approach, limiting overall momentum in the semi-finished steel segment.

Metallics

- Meanwhile, the sponge iron market remained volatile, witnessing minor fluctuations of INR 100-200/t ($1-2/t) across key locations. While some regions recorded marginal gains, others saw slight corrections. The market’s mixed trend was due to higher input costs and weak buying interest, leading sellers to hold offers firm in the short term to limit downside risks.

- SAIL’s Rourkela Steel Plant (RSP) conducted an auction on 3 November for 4,000 t of steel-grade pig iron, in which the entire quantity was booked at an average price of INR 31,700/t exw. This marks an increase of INR 1,150/t compared to the previous auction on 24 October, in which the entire quantity of 3,800 t was sold at INR 30,550/t exw.

- Indian direct reduced iron (DRI) export offers edged lower by $1-2/t this week, settling at $312/t CPT Raxaul and $322/t CPT Benapole. The decline came as buying interest from Bangladesh remained limited, with only a few spot bookings heard during the week.

Finished long steel

- IF-rebar: The induction furnace (IF) route rebar market witnessed a downward trend this week. Market participants highlighted slower buying activity compared to the previous week, as most buyers had already procured material earlier. Dispatches and lifting of previously booked orders are currently in progress. Inventory levels were estimated at around 12-15 days, which is usually maintained at 8-10 days. In the near term, participants expect the market to remain range-bound.

- On a weekly basis, rebar prices decreased by INR 200-1,000/t across regions, except in a few markets such as Mandi, Mumbai and Hyderabad, where prices increased by INR 200/t, 700/t and 500/t, respectively.

Trade reference prices of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size were assessed at INR 37,400-38,000/t exw Raipur and INR 41,900-42,500/t exw-Jalna. - Trade reference prices of heavy structural steel for base size 150mm channel stood at INR 39,400-39,800/t exw-Raipur.

- Trade reference prices of wire rod hovered at INR 37,900-38,500/t ex Raipur.

- BF-rebar: Some leading primary mills have increased rebar prices by up to INR 1,250/t ($14/t) for early-November 2025 deliveries as against prices prevailing in end-October, sources informed BigMint. Meanwhile, some mills have rolled over their prices against previous levels. Demand remained sluggish in the trade channel last month owing to the festive season and the extended monsoon.

- Trade-level BF rebar prices rose by INR 500/t ($6/t) w-o-w to INR 47,800/t ($539/t) exy-Mumbai, as per BigMint’s assessment on 7 November 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices opened at INR 45,500-46,500/t ($513-524/t) FOR Mumbai basis.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India increased w-o-w to INR 46,700-49,000/t ($526-552/t). Cold-rolled coil (CRC) prices ranged between INR 52,600-57,000/t ($593-643/t).

- BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) inched up by INR 200/t ($2/t) w-o-w to INR 47,600/t ($537/t) on 4 November 2025 against INR 47,400 ($534/t) on 28 October. CRC (IS513, Gr O, 0.9 mm/CTL) prices rose by INR 500/t ($6/t) w-o-w to INR 55,500/t ($626/t) on Tuesday against INR 55,000/t ($620/t) the week before. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- In the HRC segment, after a period of softening prices, driven by weak demand and festive-season slowdown, sentiment has begun to improve. Following the holidays, participants returned to the market, leading to a slight price recovery. Additionally, optimism grew, as mills considered list price hikes for November despite low expectations of an improvement in demand. Tighter supply from blast furnace and HSM shutdowns signal a mild near-term upside.

- India’s bulk imports of HRCs touched 391,856 t as of 31 October 2025, based on vessel line-up data. Around 93,380 t of additional cargoes are expected by mid-November.

- India’s bulk exports of HRCs touched 442,393 t as of 31 October 2025.

- BigMint’s Indian hot-rolled coil (HRC, S275) export index for Europe (EU) fell by $8/t w-o-w to $532/t FOB main port amid CBAM uncertainties. The HRC (SAE 1006) export index for the Middle East (ME) and Vietnam dropped by $5/t w-o-w to $490/t FOB. This decline in prices was due to weaker global market sentiments. Moreover, market participants are waiting for clarity regarding CBAM, sources informed BigMint.

Leave a Reply