- Domestic coal prices steady amid limited SECL auction volumes

- Indonesian coal sentiment improves on Chinese demand recovery

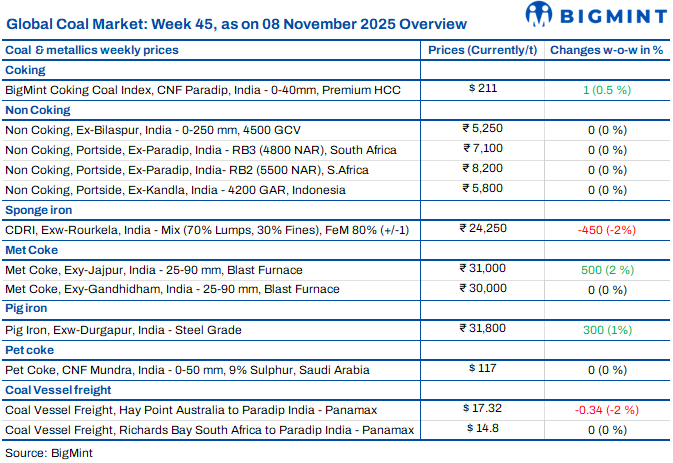

India’s coal market maintained a cautious tone this week as trading activity stayed muted following festive disruptions and sluggish industrial demand. Limited auction volumes from SECL, stable portside prices, and subdued sponge iron production kept overall sentiment restrained. While Chinese buying supported seaborne benchmarks, domestic fundamentals remained weak, with market participants expecting mild restocking-led support ahead of winter demand.

Portside Indonesian coal prices rise on stronger Chinese demand

Indian portside prices for Indonesian-origin thermal coal edged up w-o-w, supported by firmer seaborne benchmarks and revived Chinese buying ahead of winter. BigMint assessed 5000 GAR at INR 7,150/t at Kandla and INR 7,050/t at Vizag, while 4200 GAR stood at INR 5,800/t and INR 5,700/t, respectively. The 3400 GAR grade rose to INR 4,450/t at Navlakhi. Gains were limited by weak freight and cyclone delays. On the seaborne front, Indonesian 5800 GAR increased by $1.65/t to $79.85/t, while 4200 GAR and 3400 GAR rose $1.74/t and $0.33/t, respectively. Indian market sentiment remains cautiously optimistic amid firm overseas demand and mild restocking before winter.

South African coal market dull amid weak demand

South African portside thermal coal offers in India stayed largely unchanged w-o-w, with RB2 (5500 NAR) at INR 8,200/t and RB3 (4800 NAR) at INR 7,100/t across Paradip, Vizag, and Gangavaram. Weak buying led traders to divert cargoes to South Korea and Sri Lanka. Two small RB2 deals were heard at INR 8,125/t (2,000 t) and INR 8,100/t (4,000 t) ex-Mangalore. BigMint’s C-DRI index (ex-Rourkela) fell INR 450/t w-o-w to INR 24,250/t as sponge iron demand stayed sluggish. On the export side, RB2 FOB offers dipped $0.5/t to $71.50/t and RB3 by $1/t to $58/t, while freight remained steady at $14.8/dmt. Overall sentiment stayed weak amid muted industrial activity and limited restocking.

Domestic coal prices steady

Domestic coal prices stayed stable w-o-w, with 5,000 GCV coal assessed at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. SECL will auction 238,500 t of non-coking coal on 13 November, mainly G6-G9 and G12 grades. Limited auction volumes could mildly support prices, though sluggish steel demand may restrict any sharp gains in the near term.

US thermal coal prices steady amid muted buying interest

Portside prices of US-origin thermal coal in India were unchanged w-o-w at INR 10,150/t ex-Kandla. Weak end-user demand and a lack of post-festive buying momentum kept trade limited. Sufficient domestic coal availability also contributed to stable price levels through the week.

BigMint coking coal index inches up on Chinese market strength

BigMint’s premium hard coking coal (PHCC) index rose by $1/t w-o-w to $211/t CNF Paradip on 7 November, supported by firm Chinese demand. Traders noted Australian offers at $211-212/t CFR India, while bids stayed $3-4 lower, leaving deals unconfirmed. Indian steel mills continued cautious buying as prices followed Chinese trends.

In China, the met coke market is expected to see a fourth round of price hikes amid tight supply and elevated input costs. Meanwhile, India’s BF rebar market displayed mixed pricing signals, with some primary mills raising offers by INR 1,250/t while others maintained previous rates.

Eastern India’s met coke prices hit 6-month high

Met coke prices in eastern India rose to a 6-month high at INR 31,000/t ex-Jajpur, supported by limited supply and higher coking coal costs. Australian premium hard coking coal gained $3/t w-o-w to $197/t FOB, pushing offers up. Improved trading and fresh tenders tightened merchant availability in the east, while western markets stayed steady. Pig iron prices also firmed in recent auctions. Looking ahead, met coke prices are expected to stay stable to firm, driven by active eastern demand and elevated coking coal prices despite weak steel margins.

Refiners cut pet coke prices for Nov’25

Indian refiners reduced pet coke prices for November 2025. Nayara Energy reduced prices marginally by INR 50/t to INR 14,820/t, following last month’s INR 580/t hike. MRPL slashed rake supply prices by INR 400/t to INR 11,370/t (excluding INR 70/t tarpaulin charge) and road supply prices to INR 12,870/t. Buyers lifting over 2,500 t/month via road can avail an INR 1,500/t discount, matching rake prices. CPCL trimmed its price slightly by INR 30/t to INR 14,530/t. BPCL announced a mixed revision — Bina refinery raised rates by INR 297/t to INR 15,046/t, while Kochi reduced by INR 11/t to INR 12,536/t. Refineries reduced prices after four consecutive months of upward revisions.

Imported pet coke prices steady amid wide bid-offer gap

Imported pet coke prices in India held firm w-o-w, with BigMint assessing US-origin material at $118-120/t CFR and Saudi-origin at $117-119/t CFR. The market continued to face a wide bid-offer gap, as traders quoted higher prices while buyers sought discounts. Meanwhile, Chinese buyers booked three US-origin cargoes above $120/t CFR, and Indian buyers explored other import sources.

Dry bulk coal freights soften amid weak post-festive demand

India’s seaborne coal freight market stayed under pressure this week as muted industrial demand, a post-festive season trade lull, and cyclone disruptions slowed fixture activity. Panamax freights on the Australia-India route slipped to $17.32/dmt, while South Africa-India remained flat at $14.80/dmt. Supramax freights from Indonesia to India dropped to $13.73/dmt. With weak cargo inflow and limited restocking, freights are likely to remain subdued in the near term.

Leave a Reply