- Alang consolidates lead in South Asia’s recycling market

- Bangladesh, Pakistan lag amid compliance and payment hurdles

- HKC-certified Alang yards drive growth despite weak domestic demand

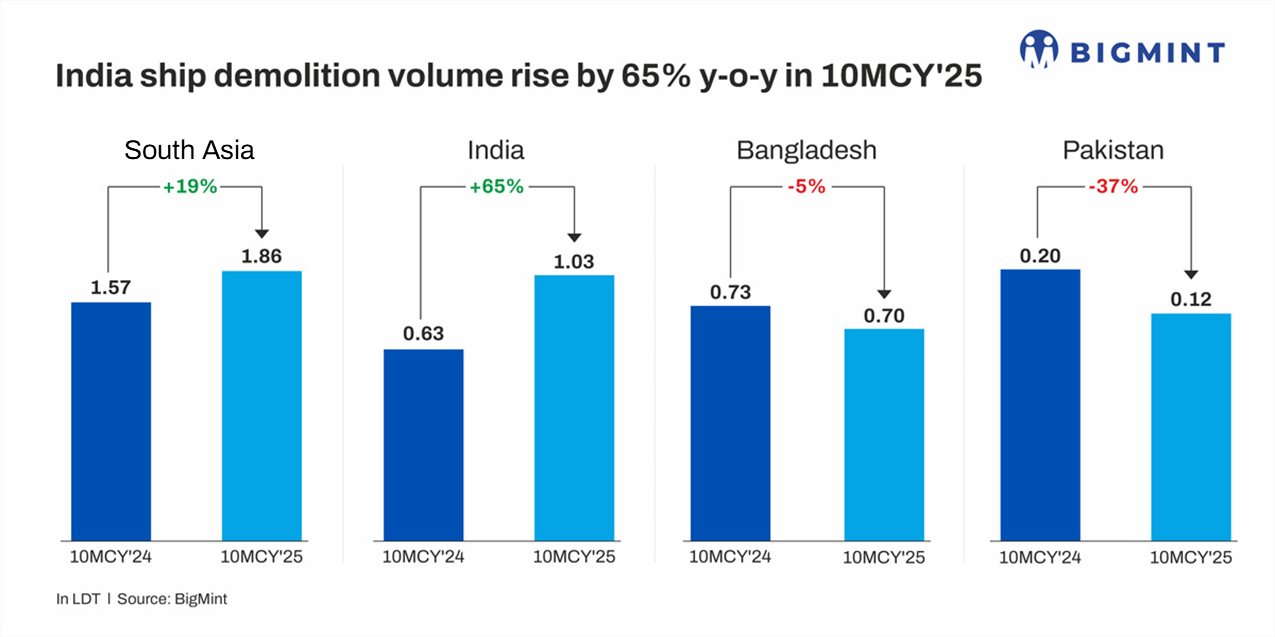

Morning Brief: India’s ship recycling industry witnessed a sharp growth in the first 10 months of 2025, reinforcing its lead over its South Asian counterparts – Pakistan and Bangladesh. Total arrivals at Alang reached 1.03 million light displacement tonnage (LDT), up 65% from 629,840 LDT a year earlier, data shows.

The number of vessels dismantled at Alang yards climbed to 103 from 82 in the same period last year. India’s strong Hong Kong Convention (HKC) compliance (with 112 of the 131 operational yards certified) kept it ahead of Bangladesh and Pakistan, both of which continue to face regulatory and financial setbacks.

The surge in dismantling assumes significance because BigMint data shows that volumes in Alang had declined to the lowest level in 2024 since the global financial crisis in 2008, falling to around 680,000 LDT compared with 1.02 million LDT in 2023 – a decrease of 35% y-o-y.

Why did volumes surge?

Why did volumes surge?

Industry officials said the recent surge in tonnage was driven by sanctioned or OFAC-linked vessels being accepted at Indian yards. “Compliant tonnage inflows have nearly dried up, while sanctioned ships continue to find buyers,” an Alang-based recycler said. Only small lots of open-market vessels, roughly 100,000-200,000 t, arrived recently, underscoring a two-tiered market.

This trend has pressured bidding levels for compliant vessels, as India remains the only South Asian destination willing or able to handle such “shadow” ships. Despite higher volumes, local sentiment remains subdued. Container and tanker segment demand has weakened, and prices are expected to ease further by INR 2-3/kg before stabilising.

Liquidity remains tight, with limited bank support for imports. Only select Russian financial channels are reportedly facilitating payments, forcing most recyclers to rely on private arrangements.

Why are Bangladesh, Pakistan losing ground?

Ship recycling in Bangladesh and Pakistan contracted due to limited HKC compliance, weak steel demand, and liquidity issues. Bangladesh’s volumes fell 5% y-o-y to 703,122 LDT, with vessel count down to 72 units. Only 9 of 130 yards are HKC-certified, and NOC delays continue to restrict operations.

Pakistan’s ship recycling declined 37% y-o-y to 129,291 LDT, with 17 vessels dismantled versus 25 last year. LC shortages, currency volatility, and slow regulations kept activity low, diverting several ships to India, where HKC compliance and operational readiness remain stronger.

Bangladesh and Pakistan have posed tough competition previously in the purchase of scrap ships. These countries, especially Bangladesh, are faced with growing domestic steelmaking capacity along with near-total dependence on imported scrap. Therefore, these countries were prepared to pay higher prices for ships compared with Indian buyers. Moreover, Pakistan and Bangladesh remained outside the HKC framework for long and were able to bid competitively for decommissioned ships.

However, today global regulations such as the Hong Kong Convention and EU Ship Recycling Regulation have changed the scenario and non-compliant yards are finding it difficult to survive.

How are prices trending across South Asia?

How are prices trending across South Asia?

Container vessel prices averaged $455/LDT in India during 10MCY’25, down from $529/LDT last year. Bangladesh and Pakistan followed similar trajectories, with prices falling to $460/LDT and $462/LDT, respectively.

For tankers, Indian prices declined to $445/LDT from $513/LDT, while Bangladesh and Pakistan registered drops to $450/LDT and $452/LDT. The regional correction reflects subdued end-user steel demand and a softer scrap market.

What lies ahead for South Asia’s ship recyclers?

What lies ahead for South Asia’s ship recyclers?

India is expected to retain its leadership in South Asia’s ship recycling trade, supported by HKC compliance, operational capacity, and regulatory stability. In contrast, Bangladesh and Pakistan may continue to face slower inflows unless compliance frameworks and financial access improve.

Market participants anticipate a mild recovery in early 2026, contingent on improved shipping activity and firmer steel prices. Until then, India’s Alang yards are likely to remain the primary destination for vessel recycling in the region.

Leave a Reply