- Rainfall-led mining disruptions may tighten supply in Nov’25

- Market to stay mildly bullish despite weak freights, demand

Indian portside prices of Indonesian thermal coal increased w-o-w during the week ending 7 November 2025, underpinned by firmer global benchmarks and improved Chinese procurement activity.

Market participants highlighted a gradual recovery in buying sentiment as international indices strengthened, and Chinese import demand revived ahead of the peak winter heating season.

Price assessments, market sentiment

According to BigMint’s assessments, the 5000 GAR grade increased by INR 50/t w-o-w to INR 7,150/t at Kandla and INR 7,050/t at Vizag. Similarly, the 4200 GAR grade was assessed at INR 5,800/t at Kandla and INR 5,700/t at Vizag, while the 3400 GAR grade gained INR 50/t to INR 4,450/t at Navlakhi. The price strength was largely attributed to elevated seaborne values and cautious trader restocking in anticipation of higher Q4 demand.

Market sources noted that improved Chinese buying interest following the partial easing of import restrictions and tightening domestic supply lifted regional sentiment. The broader Asian market also reflected firming trends as utilities sought to rebuild stockpiles before winter demand peaks.

Freight market softens slightly

Despite rising coal prices, Supramax freights on the Indonesia (East Kalimantan)-India (Navlakhi) route extended their marginal decline, reflecting low chartering activity and weak demand for spot tonnage. Freight levels fell by $0.05/dmt to $13.73/dmt compared to 30 October 2025.

Charterers reported limited new cargo inquiries amid ample vessel availability in the Pacific basin. A slight drop in bunker fuel prices further pressured freights, which are expected to remain weak in the near term as owners compete for limited cargoes.

Portside inventories decline amid cyclone disruptions

India’s portside thermal coal inventories fell by 2.6% w-o-w to 12.98 million tonnes (mnt) in Week 44 (ending 2 November 2025), compared with 13.33 mnt in the previous week. The decline was primarily led by disruptions caused by a cyclone along the eastern coast, which delayed vessel arrivals and hampered cargo discharge operations.

Weaker restocking at Kandla and Navlakhi weighed on inventories, as traders held back amid uncertain prices and steady industrial demand. Inflows should recover with full port operations, though replenishment may stay slow due to logistical delays.

Power sector coal stocks sufficient but supply imbalances remain

As of 6 November 2025, coal inventories at Indian power plants were at 49.03 mnt, providing about 16 days of consumption cover, suggesting a comfortable supply position at the national level. However, disparities persisted across regions and fuel sources.

Notably, 15 power plants remain under critical stock conditions, including eight reliant on domestic coal, five dependent on imported coal, and two using washery rejects. The localised shortages stem from supply chain bottlenecks, logistical delays, and reduced dispatches from select collieries.

While overall coal availability remained adequate, consistent replenishment and improved logistics will be essential to ensure stable operations during the high-demand winter period.

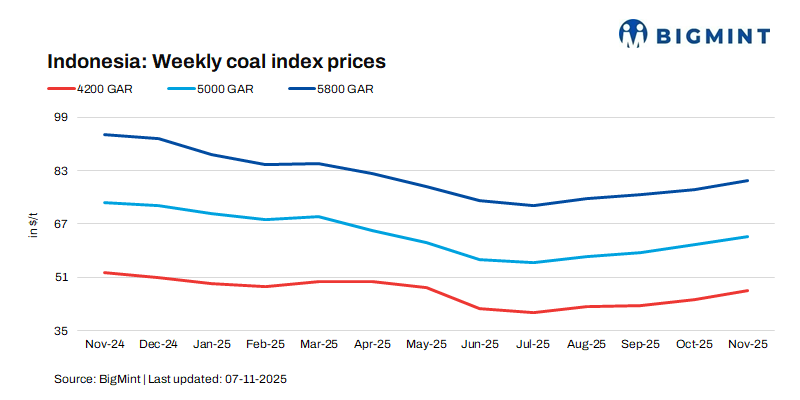

Seaborne coal market strengthens on seasonal Chinese demand

The seaborne Indonesian coal market recorded modest gains during the week, supported by stronger Chinese spot demand and tightening weather-related supply constraints in producing regions. The 5800 GAR grade increased by $1.65/t w-o-w to $79.85/t, the 4200 GAR grade rose by $1.74/t to $47.07/t, and the 3400 GAR grade edged up by $0.33/t to $32.22/t.

The rise in prices reflected steady tender activity from Chinese coastal utilities and resilient South Asian buying interest, even as global freights softened. Market participants expect Indonesia’s FOB prices to remain supported as rainfall in Kalimantan begins to disrupt mine output and loading operations, potentially tightening export availability through November.

Outlook

India’s portside thermal coal market is expected to stay mildly bullish amid firm seaborne prices and pre-winter restocking, though weak domestic demand and lower freights may cap gains. Prices are likely to remain range-bound to slightly higher through mid-November.

Leave a Reply