- Falling sponge iron prices weigh on demand

- Prices may continue to face downward pressure

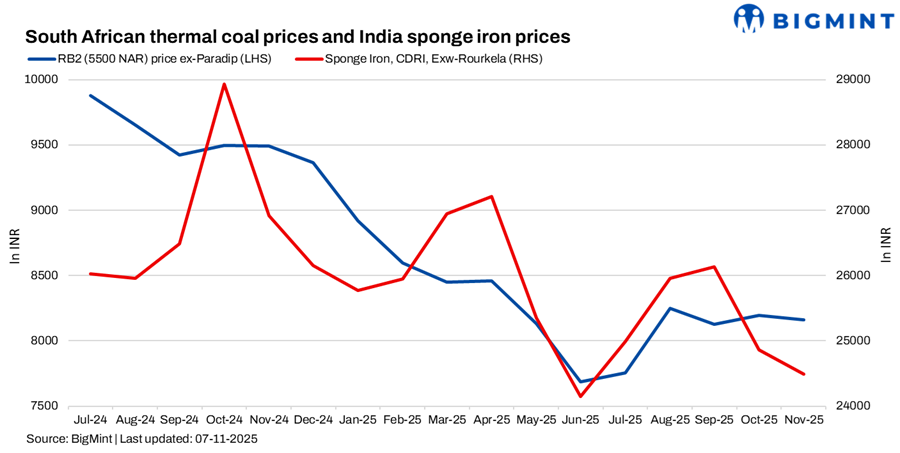

South African portside thermal coal offers in India remained largely unchanged w-o-w, with RB2 (5500 NAR) assessed at INR 8,200/t and RB3 (4800 NAR) at INR 7,100/t across Paradip, Vizag, and Gangavaram. The market remained subdued, with traders diverting cargoes to South Korea and Sri Lanka due to weak Indian demand. Two small deals were heard for RB2 coal at INR 8,125/t (2,000 t) and INR 8,100/t (4,000 t) ex-Mangalore, indicating thin trading activity.

Portside thermal coal inventories dropped 2.6% w-o-w to 12.98 mnt in Week 44 (ending 2 November 2025) from 13.33 mnt in Week 43. The decline was driven by slower vessel arrivals and lower offtake across the eastern coast following cyclone disruptions, while restocking at western ports remained weak.

Domestic coal prices stayed firm, with 5,000 GCV assessed at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. SECL’s upcoming auction on 13 November will offer 238,500 t of non-coking coal across grades G6-G9 and G12. With reduced supply, prices could see mild upward momentum, though weak steel activity may cap gains. However, bids would finally determine the auction outcome.

In the sponge iron market, BigMint’s C-DRI index (ex-Rourkela) declined by INR 450/t w-o-w to INR 24,250/t amid weak end-user demand and slow inquiries. Sellers were seen reducing offers to conclude small-volume deals, while bulk bookings remained absent due to liquidity constraints.

On the export front, South African RB2 FOB offers fell marginally by $0.5/t w-o-w to $71.50/t, and RB3 slipped by $1/t to $58/t. Despite stable Panamax freights at $14.8/dmt on the South Africa-India route, buying sentiment stayed muted amid limited vessel fixing and holiday slowdown at the Richards Bay Coal Terminal (RBCT).

Outlook

Market sentiment in India remains cautious as weak industrial activity and poor steel demand weigh on imported coal buying. Unless fresh restocking emerges in the second half of November, South African coal offers may remain under slight downward pressure.

Leave a Reply