- Higher quantities from SAIL lift overall auction volumes

- Elevated base prices trigger resistance, auction cancellations

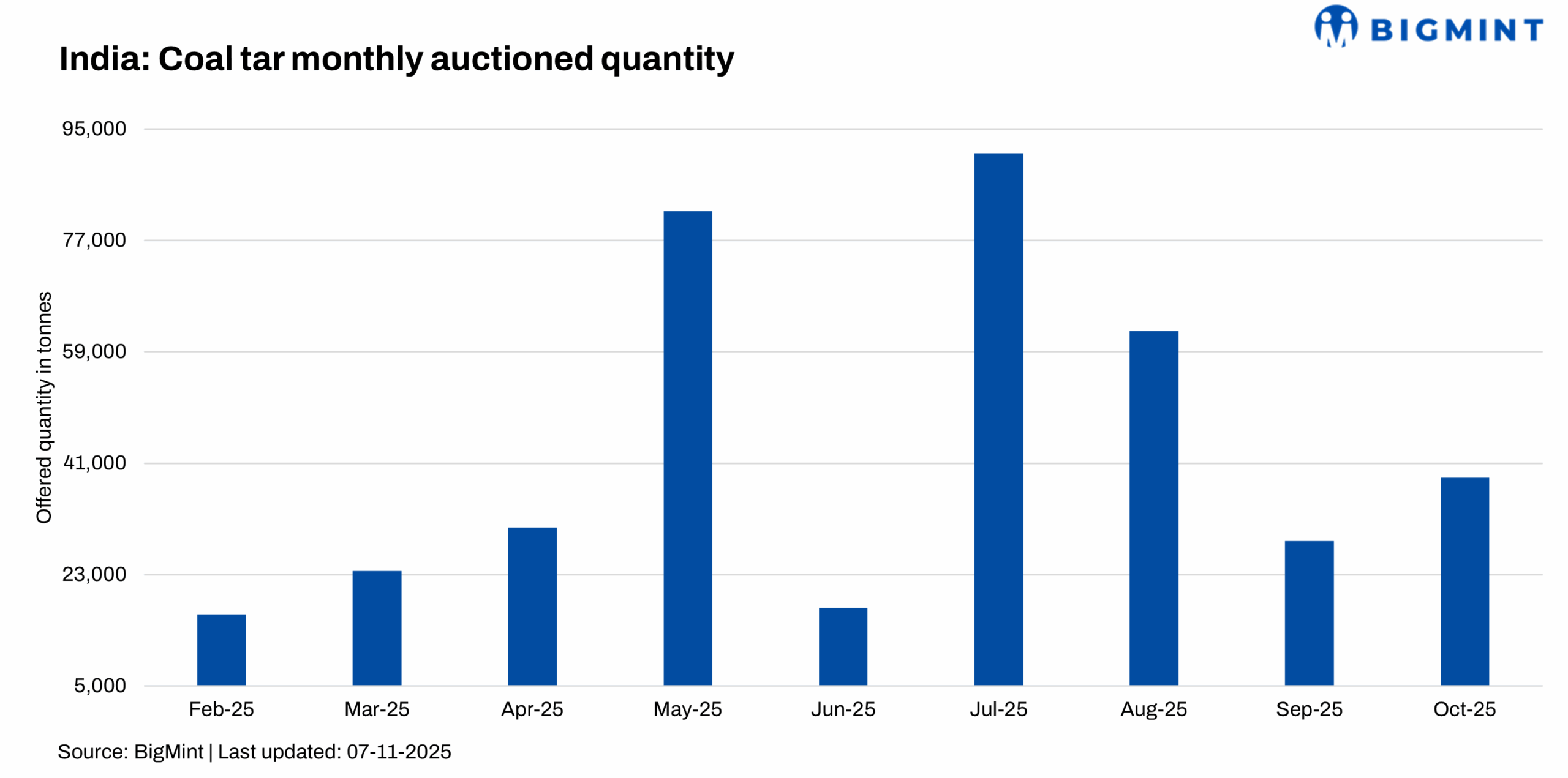

India’s crude coal tar market saw offered volumes in auctions climb up to 38,661 tonnes (t) in October 2025 from 28,431 t in September, driven by a surge in quantity from SAIL subsidiaries and a higher number of auctions overall. Despite the increase in auction volumes, buying interest remained muted, as many buyers were reluctant to book material at the announced base prices, considering them to be high. This caused several auctions to be cancelled or repeatedly rescheduled.

BigMint assessed crude coal tar at INR 31,755/t (ex-works, Eastern India) in October, down from INR 37,500/t in September.

According to market participants, coal tar pitch prices declined in October 2025, largely reflecting subdued demand from downstream sectors and weak market fundamentals. This downward trend subsequently exerted pressure on raw material – crude coal tar prices, leading to a corresponding decline during the month.

SAIL – auction-by-auction details

- Rourkela Steel Plant: An auction originally scheduled for 9 October (6,400 t) received no bids due to a high base price. The lot was eventually upsized and relisted multiple times — 22 October, 28 October, and 31 October. On 31 October 2025, 9,500 t were sold at INR 31,755/t, marking a decline of INR 5,745/t versus the previous successful auction on 18 September.

- Durgapur Steel Plant: An auction on 24 October was rescheduled to 28 October after receiving no bids; on 28 October, the plant sold 8,500 t at a weighted average of INR 32,200/t, down INR 4,400/t from the auction held on 2 September. This demonstrated buyers’ reluctance at earlier base levels.

- Bhilai Steel Plant: SAIL-Bhilai concluded two successful auctions in October. On 8 October, 1,985 t were sold at a weighted average of INR 33,500/t. Another auction on 18 October was rescheduled due to no bids and subsequently held on 28 October, where 2,506 t were sold at INR 31,500/t. These results show intra-month price moderation.

Other suppliers and participation

NMDC Steel (Nagarnar) and RINL (Vizag): NMDC sold 300 t at INR 31,700/t on 28 October, down INR 4,400/t m-o-m, while Vizag Steel sold 2,310 t at INR 32,500/t on 22 October, a drop of INR 4,550/t from its September auction. Multiple early-October auctions across suppliers were cancelled due to resistance to base prices.

Outlook

With SAIL’s increased offered volumes and cautious buying due to high base prices, prices are expected to remain under pressure in November, though steady industrial consumption and selective bidding could stabilise volumes and prevent sharp additional declines, particularly in key demand regions.

Leave a Reply