- Prices may slip below $100/dmt amid oversupply

- Shrinking profits lead mills to reduce production

Mysteel Global: China’s imported iron ore market is set for a softer November, with both supply and demand expected to weaken amid slower global shipments and lower domestic hot metal output, according to Mysteel’s latest monthly report on the commodity. As supply continues to outstrip demand, prices of imported iron ore are likely to trend downward, the report predicts.

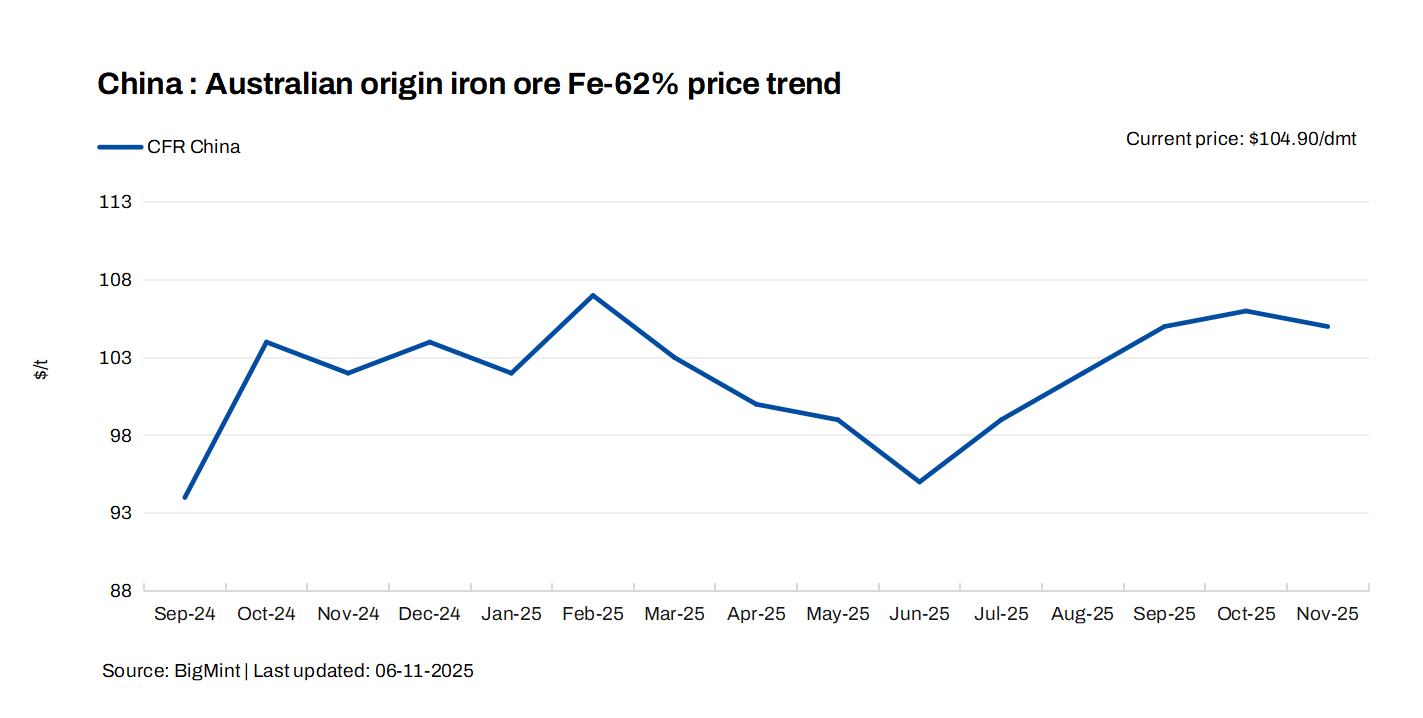

Imported iron ore prices were on a roller-coaster ride during October, increasing initially — driven by active replenishment by steelmakers after China’s National Day holiday — and then falling as blast furnace production declined. Yet, the last few days of October saw prices rebound, as the easing of trade tensions between China and the United States bolstered market sentiment.

Despite last month’s volatility, average iron ore prices held largely steady from September. Mysteel’s SEADEX 62% Australian Fines index, for instance, averaged $104.85/dmt CFR Qingdao throughout October, higher by a marginal $0.14/dmt from the previous month.

Looking ahead to November, with limited new policy catalysts expected, weakening fundamentals will begin exerting pressure on imported iron ore prices.

On the supply side, seasonal port maintenance in Australia and Brazil will curb iron ore shipments from these key exporters in November, resulting in an m-o-m decline of 10 million tonnes (mnt) in global iron ore shipments, the report forecast. However, arrivals of iron ore cargoes at Chinese ports are expected to remain elevated, supported by earlier robust shipment volumes, the report added, hinting at still loose supply of iron ore.

Demand for the steelmaking material seems set to soften further, however, with Chinese steelmakers continuing to trim their hot metal production. Shrinking profit margins have already led mills to steadily scale back their production over the past month, and there are few signs that their profitability will improve significantly in the weeks ahead.

During the last week of October, daily hot metal output among the 247 blast-furnace mills tracked by Mysteel averaged 2.36 mnt/day, down 2.3% from the same week the month before. Over the same period, the number of steelmakers saying they were still making profits on steel sales also hit the lowest level so far this year.

Meanwhile, steel consumption in China is expected to weaken as colder weather hampers outdoor building activity, making further cuts in construction steel production a strong possibility. In addition, seasonal output restrictions imposed on heavy industry sectors in northern China — aimed at curbing winter smog — will also contribute to lower hot metal output among mills.

The daily hot metal output of the 247 mills surveyed is forecast to range between 2.35-2.38 mnt/day during November, lower than October’s range of 2.36-2.42 million t/d, according to the report.

Amid the growing supply glut of iron ore, prices will struggle to stay above the $100/dmt threshold, with potential declines toward $95/dmt, the report warned, adding that the oversupply will also be reflected in China’s portside stocks mounting further.

By the end of October, stocks of iron ore at China’s major 45 ports had accumulated by 5.4 mnt or 3.9% m-o-m to a seven-month high of 145.4 mnt, Mysteel’s tracking showed.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply