- Inner Mongolia leads production growth

- Healthy profits support high operating rates

Mysteel Global: China’s production of high-carbon ferro chrome climbed to a new peak in October, driven by sustained profitability and high operating rates at smelters, Mysteel Global understood.

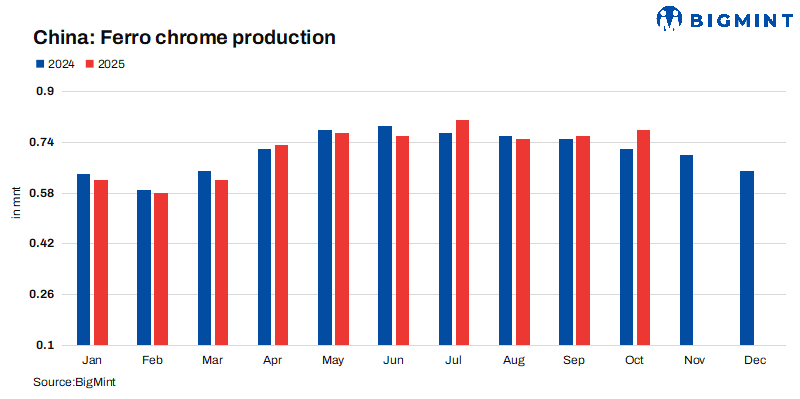

High carbon ferro chrome output among the 177 domestic smelters Mysteel regularly surveys showed they produced 825,000 tonnes (t) last month, making for a m-o-m increase of 1.5% and a y-o-y rise of 8.9%. Cumulative output over January-October stood at 7.27 million tonnes (mnt), down 2.8% from the same period last year, however. The 177 smelters represent 95% of domestic capacity.

The primary production hub of Inner Mongolia led the growth last month, with output there hitting 602,700 t, up 2.4% from September and 14% from a year earlier, the survey results show.

The rise was fuelled by healthy profit margins, which incentivised smelters to maintain high run rates. “Although retail ferro chrome prices saw a minor correction last month, major stainless steel mills raised their purchase prices under long-term contracts for October delivery, ensuring that the smelters enjoyed decent profit margins,” an industry insider in East China’s Wuxi told Mysteel Global.

For instance, China’s Tsingshan Group had announced on 23 September that it was lifting its bid price for HC ferro chrome for October delivery by RMB 200/t ($28/t) to RMB 8,495/t (50% Cr basis), or $1,194/t, including tax.

Similarly, a large-scale steel mill in North China set its purchase price for the ferro alloy at RMB 8,295/t ($1,164/t) (50% Cr basis) for October delivery, cash payment, including tax and delivery, up by RMB 50/t ($7/t) from the previous month.

Meanwhile, production costs among smelters dipped in October. Mysteel’s assessments suggest that as of 30 October, the average cost for producing HC ferro chrome using the semi-closed submerged arc furnace-electric furnace (SF-EF) route in Inner Mongolia had fallen to RMB 7,862/t ($1,107/t), a drop of RMB 59/t ($8/t) from a month earlier.

As a result, local smelters using the SF-EF process secured an average profit of RMB 403/t ($57/t) on sales under long-term contracts and RMB 438/t ($61/t) on spot sales, according to Mysteel’s assessment.

Amid these favourable conditions, smelting operations remained vigorous. Most HC ferro chrome producers in South China maintained high operating rates, while in North China, despite maintenance stoppages at some facilities, the restart of large-capacity plants contributed significantly to output growth, a Shanghai-based source noted.

A smelter in Inner Mongolia that resumed operations at end-September is estimated to have contributed roughly 50,000 t of HC ferro chrome output in October, the source added.

The positive momentum is expected to extend into November, a Shanghai-based analyst suggests, citing still-healthy smelter profitability.

Tsingshan, for example, kept its November purchase price unchanged from October’s level, while lower chrome ore prices have further reduced the cost of producing the ferro alloy.

As of 4 November, the average cost for smelting HC ferro chrome using the SF-EF route in Inner Mongolia had declined further to RMB 7,857/t ($1,102/t), down by RMB 64/t ($9/t) m-o-m, Mysteel data show.

These factors should continue to keep the smelters’ margins attractive, ensuring their production enthusiasm remains strong, the analyst concluded.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply