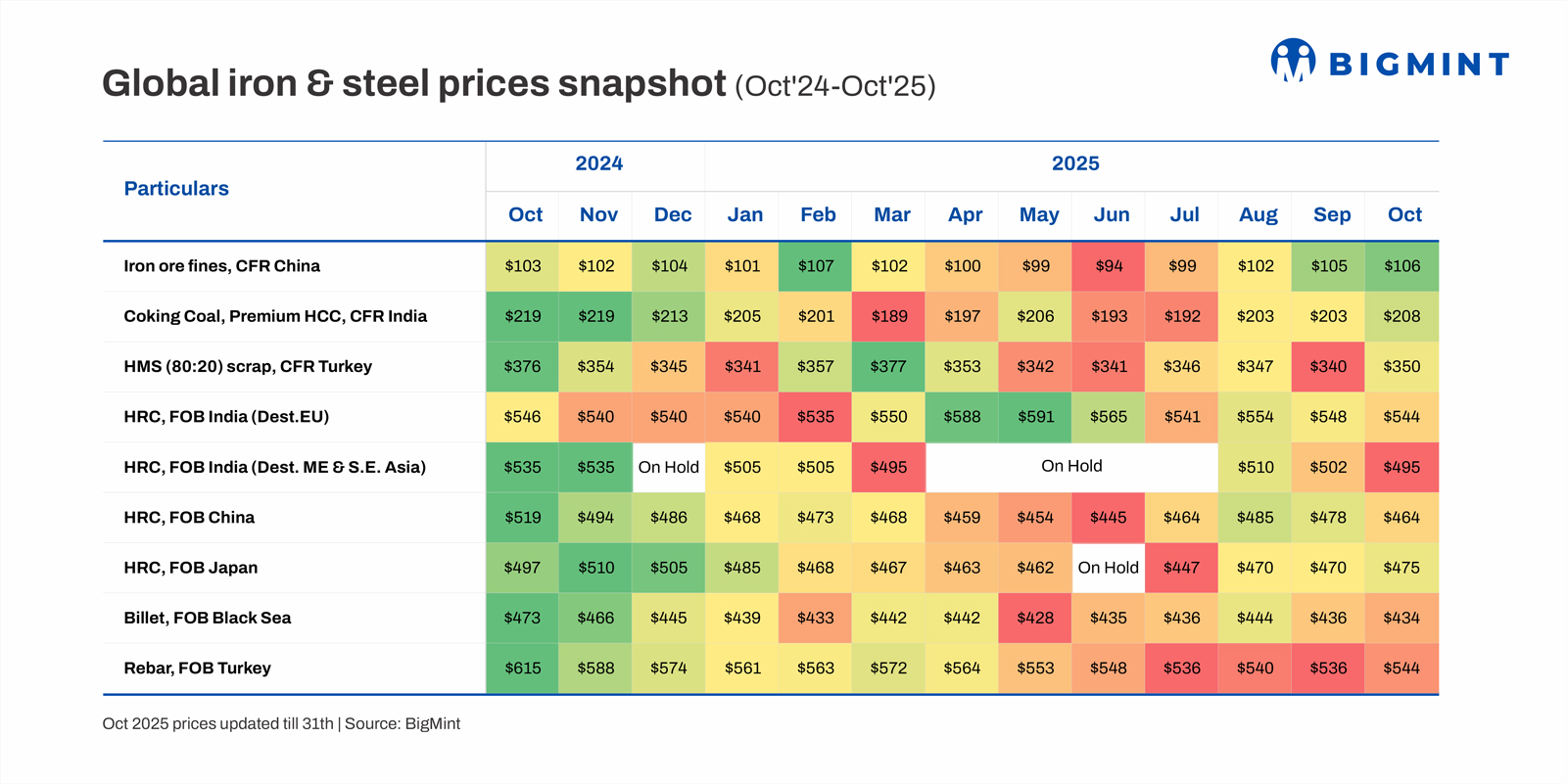

- Iron ore, coking coal prices remain firm

- Chinese, Indian HRC export prices edge down

- Global downtrend likely to continue in Q4CY’25

Morning Brief: The global steel market continued to witness a downward spiral in prices across key geographies in October 2025, signalling a weak start to Q4CY’25. Trade restrictions and the deceleration in steel demand in major regions of the world intensified market competition and negatively affected prices.

The prospect of easing US-China trade tensions was positive for the market but the end of the construction season in China and weak demand in East Asia and the EU weighed on global steel prices. Analysts believe that the US rate cut will not be sufficient to charge up manufacturing demand globally, with tariff walls and geopolitical threats freezing investor and consumer confidence.

Steel & raw material prices in Oct’25

Iron ore stays firm: Iron ore prices to China rose to $109/tonne (t) CFR after the Golden Week holidays later due to restocking, optimism over global economic recovery and easing of concerns over sintering and production cuts. However, uncertainty around talks between a key Australian miner and China’s Mineral Resources Group stirred uncertainty in the market. Sentiments improved after the US-ASEAN Summit and easing US-China trade tensions but the slight decrease in prices in end-October signals volatility ahead amid high steel stocks and weak margins.

Coking coal edges up: CFR India monthly average prices of coking coal edged up by $5/t in October as Australian coking coal prices increased by $4/t m-o-m primarily due to active buying interest from Chinese and Indian steelmakers. Notably, China’s coke market witnessed the second round of hikes recently as supplies tightened due to stricter environmental regulations in key regions leading to an approximate 30% production cut, thereby slightly limiting the availability of high-quality coke.

Ferrous scrap moves in tight range: The Turkish deep-sea scrap market moved within a tight range through October, holding between $346–354/t CFR as mills stayed cautious amid slow rebar sales and high freight costs. Most mills avoided new bookings as weak construction activity and thin margins left little room for aggressive buying what with competition from Chinese billets queering the pitch for Turkish producers. However, there is a likelihood of supplies tightening, especially from Europe, and so the slight price rebound in October is expected to sustain.

India HRC export prices drop: Indian HRC export prices to the EU declined in October due to sluggish demand within the EU and heightened uncertainty surrounding the Carbon Border Adjustment Mechanism (CBAM). EU buyers adopted a cautious wait-and-watch approach, hesitating to make bulk purchases. Proposals from the European Commission to potentially cut duty-free steel import quotas have dampened demand and forced Indian exporters to lower prices.

With Chinese HRC export offers to the Middle East declining, Indian offers too inched lower. HRC export offers to Vietnam were largely stable. However, Vietnamese steel major Hoa Phat has reduced its HRC (SAE1006, non-skin-passed) prices by $8/t m-o-m for January-February 2026 sales after keeping tags stable for November. The decline in HRC prices is attributed to weak market sentiment and subdued demand.

Chinese HRC export prices soften: The Chinese steel market maintained a stable but slightly weak price trend following the National Day holidays, which led to a surge in steel inventory. The world’s top steel manufacturer, Baosteel, rolled over HRC prices for November sales in mid-October. This was due to weak domestic demand and mixed trends on Shanghai Futures Exchange (SHFE).

The decline in monthly average HRC export prices can be explained by the seasonal demand drop-off in the domestic market. But it retains an upbeat macro mood driven by easing U.S.-China trade tensions. While rebar performance remains weak, hot-rolled coils are expected to stay relatively strong in the short term, with declining stock levels easing concerns and suggesting the market will see a rebound despite fluctuations.

Japanese HRC export prices largely stable: Japanese HRC export prices showed a slight uptrend in October. Nippon Steel kept its HRC export prices steady m-o-m for end-November and early-December sales, with offers for the Middle East and ASEAN at $520/t CFR. This is due to Nippon’s global peers such as Hoa Phat and Baosteel rolling over prices. Notably, Nippon Steel is not offering to Europe and India due to trade restrictions. Tokyo Steel, too, has rolled over HRC prices for November.

CIS billet export market outlook bright: CIS billet prices edged down marginally in October but post-monsoon demand recovery in Asia is likely to prop up prices. CIS billet suppliers have kept their prices stable but hinted at small increases amid a stronger rouble and firmer Chinese billet tags. Republic Day holidays and weak rebar sales in Turkiye weighed on the market but tight exporter margins and the expected rebound in global scrap prices will keep CIS billet offers supported.

Slow momentum in Turkish exports: Even though Turkish rebar export offers hovered at $540-550/t FOB, sales momentum stayed slow. The recent IREPAS conference also failed to lift sentiment, with industry players flagging higher freights, muted European and American demand, and growing competition from Asian and Middle Eastern suppliers. Tensions with Israel are also likely to affect rebar export prospects apart from the prevailing turmoil in West Asia.

Outlook

Global steel prices are expected to move in a narrow range in November and December, with the WSA predicting that demand will bottom out by the end of the year. Chinese domestic and export prices of steel may edge down after the peak construction season ended in October. Raw materials, with the exception of scrap, will largely follow the Chinese market movement. Scrap supplies are likely to tighten during the winter and so prices are likely to remain supported.

Due to the lack of any significant improvement in demand, the global steel market is likely to witness a supply surfeit and further deterioration in prices till December, with Chinese steel exports likely to stay elevated.

Leave a Reply