- Asian demand mixed in Oct, India reduces intake

- Thermal coal exports fall 9% y-o-y in Jan-Oct’25

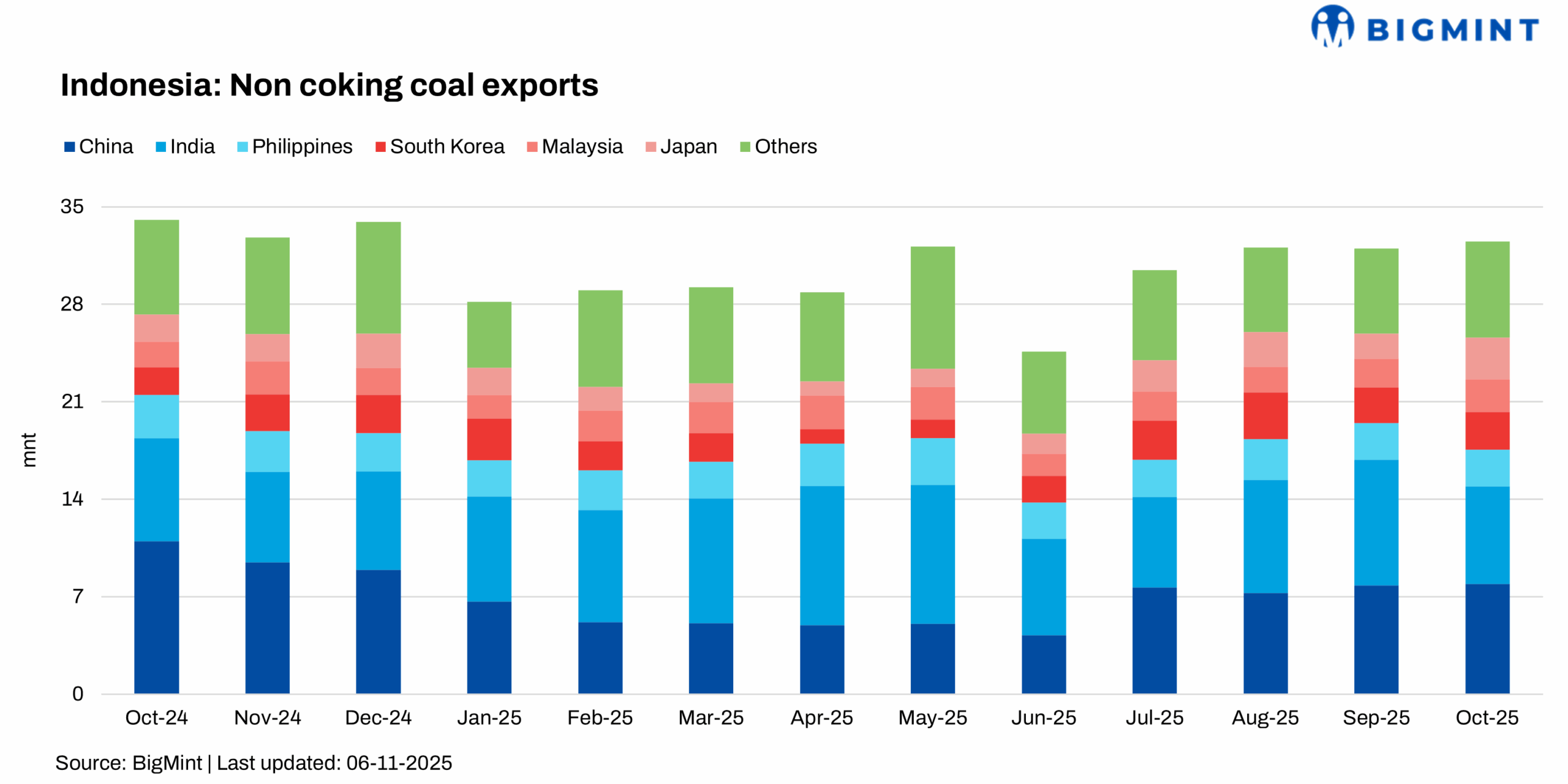

Indonesia’s non-coking coal exports posted a mild recovery in October 2025, rising 1.6% m-o-m to 32.51 million tonnes (mnt) from 31.99 mnt in September. The uptick was largely driven by resilient Asian demand and improved port activity following earlier logistical slowdowns.

However, on a y-o-y basis, shipments were down 4.6%, highlighting a gradual cooling in global coal consumption amid moderating industrial output and tighter environmental policies across key markets.

Jan-Oct’25 exports reflect sluggish global coal appetite

Between January-October 2025, Indonesia’s thermal coal exports stood at 299.2 mnt, marking a 9% y-o-y decline. The drop reflects weaker overseas demand, as Asian buyers reduced imports amid lower power generation, rising renewable use, and cost optimisation efforts, prompting Indonesian miners to recalibrate output and pricing strategies.

Asia’s import landscape splits between conservatism, opportunism

Demand across major Asian buyers remained mixed and region-driven in October. India’s imports dropped 22.6% m-o-m to 7 mnt, pressured by ample domestic stocks and weak industrial demand, as utilities drew from existing inventories. In contrast, China’s imports rose 1.3% to 7.92 mnt, supported by steady power consumption and winter readiness. Malaysia’s intake climbed 15% to 2.35 mnt amid firm industrial activity and competitive Indonesian offers.

In northeast Asia, Japan’s imports jumped 67% m-o-m to 3 mnt on seasonal restocking and power unit restarts, while South Korea’s volumes edged up 5.3% to 2.7 mnt, sustaining stable power demand. The Philippines also saw a marginal 0.3% rise to 2.64 mnt, reflecting gradual demand recovery. Overall, Asia’s coal buying remained cost-sensitive and shaped by energy diversification trends.

Regional supply dynamics remain uneven

Performance across Indonesia’s coal-producing regions remained uneven, shaped by logistical factors and grade-specific demand. East Kalimantan, the country’s dominant mining hub, saw shipments fall 8% m-o-m to 14.6 mnt due to port congestion and limited vessel availability.

North Kalimantan recorded a sharper 20% drop to 1.01 mnt, constrained by lower premium-grade uptake. South Kalimantan also eased 12% to 11.8 mnt, reflecting muted interest from major importers.

Conversely, Sumatra defied the trend, with exports surging 20% to 5.08 mnt, supported by stronger demand for low-calorific-value coal from Southeast Asian buyers seeking cheaper energy feedstock.

Port performance reflects operational contrasts

Port-wise data revealed clear operational disparities across Indonesia’s key loading terminals. Taboneo Port reported a 22% increase in shipments to 7.16 mnt, buoyed by smoother weather conditions and improved barge movements. Balikpapan, however, posted a steep 31% decline to 1.83 mnt, amid maintenance work and shipment delays. Bunati Port slipped 1.8% to 4.36 mnt, while Samarinda fell 18% to 3.88 mnt, reflecting lower throughput.

The standout performer was Muara Pantai Port, where exports soared 66% to 2.83 mnt, backed by enhanced operational efficiency and a rise in low-CV coal handling.

Thermal coal prices diverge as market balances quality, cost

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has revised its benchmark thermal coal prices (HBA) for the first half of November, reflecting mixed market sentiment amid softening global demand and shifting regional supply trends.

High-CV (6,322 kcal/kg GAR) coal prices fell 5.5% to $103.75/t due to weak buying interest, while mid-CV (5,300 kcal/kg GAR, HBA-I) eased 0.8% to $67.22/t amid stable but cautious trading.

In contrast, low-CV coal showed divergent trends, with HBA-II (4,100 kcal/kg GAR) rising 0.7% to $44.02/t and HBA-III (3,400 kcal/kg GAR) edging down 0.5% to $33.74/t, reflecting Southeast Asian utilities’ preference for cheaper grades and subdued industrial demand.

Outlook

Indonesia’s coal exports are expected to stay steady yet limited through late 2025, supported by winter demand but restrained by weak Chinese buying, high Indian stocks, and growing renewable competition. Low- and mid-CV grades should hold demand, while high-CV prices may face continued pressure.

Leave a Reply