- Declining LME stocks prevent sharper price correction

- Buyers restrict activity amid limited spot negotiations

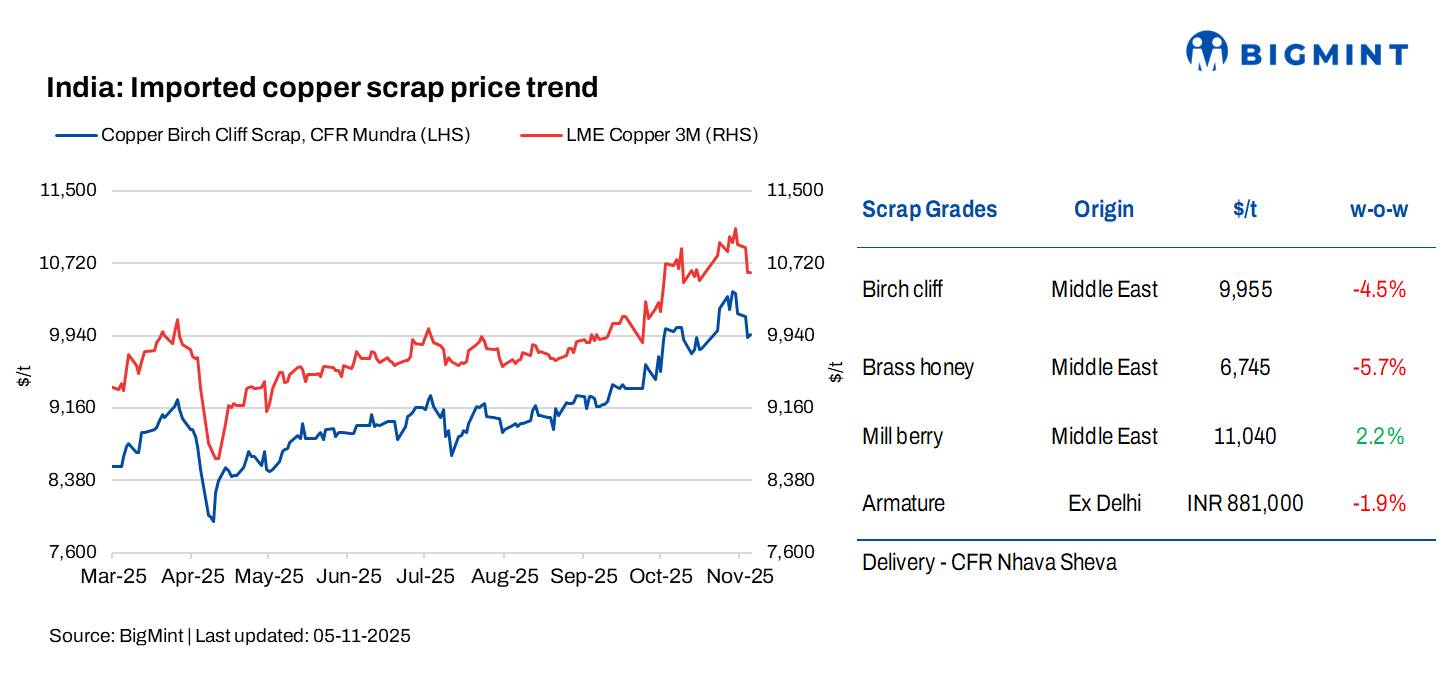

Imported copper scrap prices in India declined w-o-w tracking declines on London Metal Exchange (LME) futures. Parallelly, domestic copper scrap prices edged down amid muted demand and limited activity as the market continued to recover from the post-festive lull.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $9,955/tonne (t), down by 4.5% w-o-w, while US motors mix stood at $1,190/t (both CFR Mundra), down by 1.7% w-o-w.

LME copper eases after profit booking and softer Chinese demand

LME copper prices stood at $10,625/t on 5 November 2025, lower than $10,947/t a week earlier. LME copper prices retreated after touching $11,200/t as traders booked profits following a strong late-October rally.

The pullback was driven by a firmer US dollar, which made dollar-denominated metals costlier for overseas buyers, and by mixed signals from China, where manufacturing activity and short-term industrial demand showed signs of slowing. Rising inventories in key Chinese hubs also weighed on sentiment. However, analysts noted that the decline appeared to be a technical correction rather than a fundamental shift, as tight refined supply and resilient global demand continue to underpin market support.

Market updates

India’s copper market held largely steady this week, mirroring a mild w-o-w dip in LME copper as profit-booking and weaker Chinese demand capped gains. Domestic sentiment remained soft after Diwali, with most downstream units running at reduced capacity and postponing new purchases. Imported scrap offers stayed mostly unchanged, as suppliers maintained previous price levels instead of cutting rates.

Market activity was subdued due to the Guru Purab holiday, limiting spot negotiations across key hubs. Buyers preferred small deals in both refined and scrap segments. Demand for low-grade scrap such as mixed motors remained weak amid tight margins and continued exports of cleaner lots to Pakistan and the Far East.

Despite slow trading, underlying fundamentals provided support. Falling LME warehouse stocks helped prevent a sharper price correction, and steady import offers suggested no immediate supply pressure. Market participants expect normal trade to resume early next week, with selective restocking likely if LME prices stabilise.

Other updates

Codelco cuts forecast, Glencore faces cost hurdles

Global copper markets remain under pressure as Codelco, the world’s largest producer, cut its 2025 output guidance to 1.31-1.32 million tonnes (mnt) from an earlier 1.34-1.37 mnt, citing operational setbacks, declining ore grades, and rising capital costs. Despite this, the miner reaffirmed its long-term goal of reaching 1.7 mnt annually by 2030, supported by expansion projects at Rajo Inca and Ministro Hales.

Meanwhile, Glencore is evaluating the future of its Horne Smelter in Quebec — Canada’s largest copper facility due to environmental and upgrade costs exceeding $200 million. The smelter and the nearby Canadian Copper Refinery together produce over 300,000 t annually and employ about 1,000 workers. With copper demand expected to rise 24% by 2035 driven by electrification and renewable energy expansion, potential supply disruptions and cost pressures could tighten global markets and heighten price volatility ahead.

Outlook

In the near term, India’s copper market is expected to remain stable and even slightly firm supported by post-festive momentum and anticipated restocking activity. A recovery in downstream operations could lift spot demand modestly, while tight global refined supply and falling LME inventories are likely to cap downside risks. However, any sustained strength in the US dollar or weak Chinese buying could limit sharp gains.

Leave a Reply