- Exports remain higher by 7.8% y-o-y despite m-o-m drop

- Mild weather, logistical slowdowns weigh on Asian intake

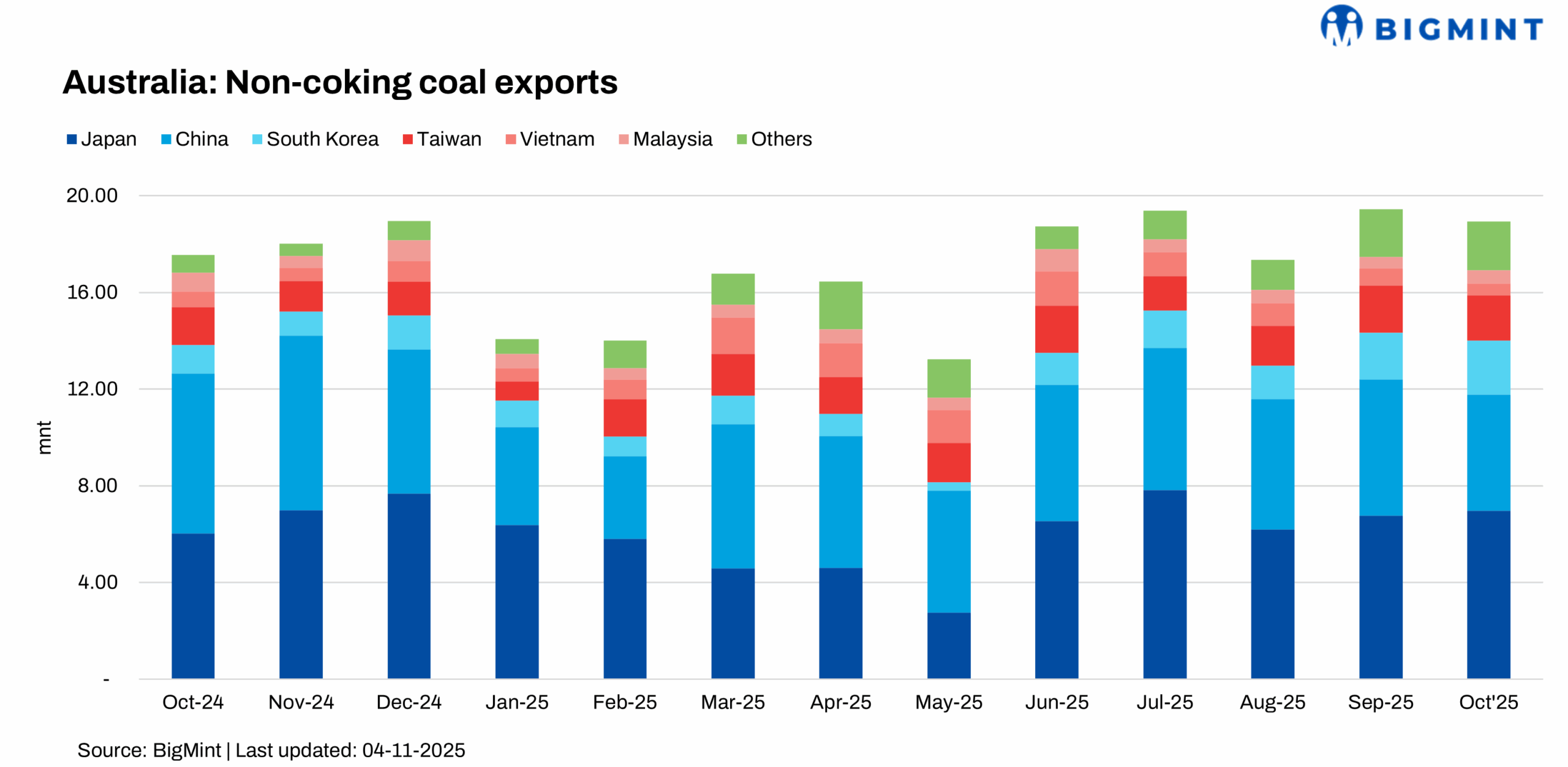

Australia’s non-coking coal exports slipped 2.6% m-o-m in October 2025 to 18.92 million tonnes (mnt) from 19.44 mnt in September. However, exports were still higher by 7.8% from 17.56 mnt in October 2024.

The m-o-m decline stemmed mainly from weaker demand across key Asian buyers, along with logistical slowdowns in certain importing nations. Reduced restocking activity and mild weather in northeast Asia also curtailed near-term buying interest, especially from China and Vietnam.

Asian demand softens

Major importers such as China, Malaysia, and Vietnam slashed their coal intakes in October amid sluggish industrial recovery and ample domestic inventories.

China’s imports fell sharply by 17.3% to 4.8 mnt, as buyers held off fresh purchases due to domestic transport bottlenecks. Malaysia’s intake declined 22.4% to 0.55 mnt, while Vietnam saw a drastic 49% fall to 0.48 mnt, reflecting subdued power demand.

Taiwan’s imports edged down 4.1% m-o-m to 1.87 mnt. Conversely, Japan, Australia’s top non-coking coal buyer, marginally increased imports by 0.6% to 6.97 mnt, supported by stable utility demand. South Korea also showed resilience, raising imports by 17.2% to 2.26 mnt on restocking.

Port performance mirrors decline

Export performance across Australia’s key coal ports reflected mixed momentum during October. Newcastle Port, the largest coal hub, handled 13.98 mnt, up 1.6% m-o-m, signalling stable vessel scheduling. Gladstone Port posted a robust 16% rise to 2.1 mnt, while Brisbane Port’s handling rose 14.1% to 0.57 mnt on steady shipments.

However, Abbot Point recorded a steep 34% fall to 1.2 mnt, while Dalrymple Bay Coal Terminal (DBCT) saw a 22.5% decline to 0.87 mnt. Port Kembla experienced the sharpest drop of 48.9% to 0.23 mnt, reflecting weaker vessel turnout.

Outlook

Australia’s non-coking coal exports are expected to remain range-bound in the near term as Asian demand stabilises following a seasonal slowdown. However, sustained Japanese and Korean buying, coupled with improved port performance, could support volumes ahead.

Leave a Reply