- SE Asian billet prices firm on post-monsoon recovery

- Turkish demand slows on weak rebar sales, holidays

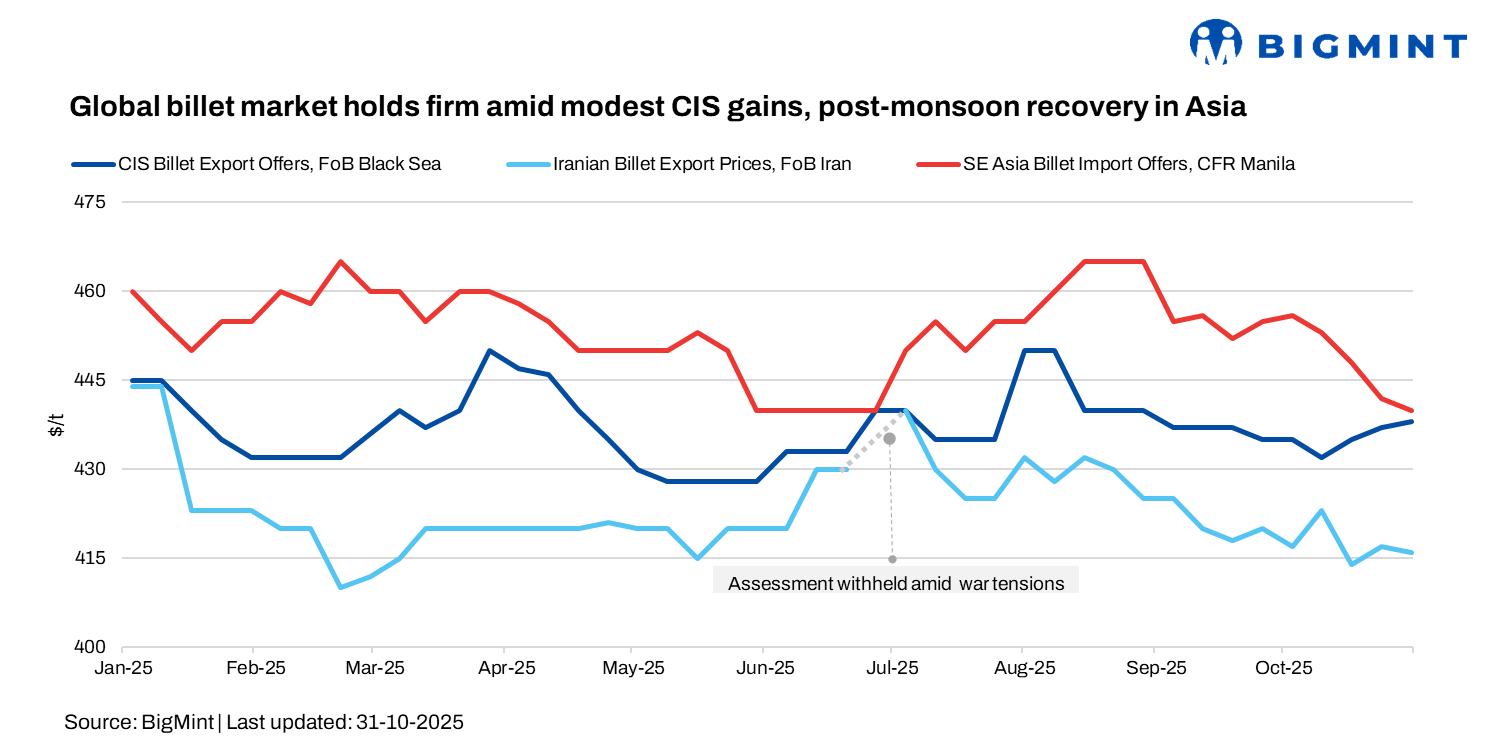

In week 44 of CY’25, the global billet market remained broadly stable, with slight upward adjustments across the CIS and Asian regions, while the Middle East and GCC markets stayed range-bound. CIS suppliers mostly maintained offers but hinted at modest hikes amid a stronger rouble and firmer Chinese billet prices.

Russian exporters were evaluating price increases to $440-445/t FOB Black Sea, compared with $435-440/t last week.

The Turkish imported scrap market stayed subdued, with limited fresh deals concluded, as mills avoided bookings amid weak rebar sales and limited working days. The availability of cheaper imported billet further pressured market sentiment.

However, scrap demand is expected to rebound in November as Turkish mills face low raw material inventories and maintain steady steel output. With European and US mills likely to restock ahead of winter, suppliers may adopt a bullish stance on tightening scrap collection in December-January.

Market updates

CIS: CIS billet suppliers mostly kept prices stable but hinted at small increases amid a stronger rouble and firmer Chinese billet tags. Export offers currently stand at $440-445/t FOB Black Sea, with mills targeting $443-447/t FOB in upcoming sales. In Turkiye, CIS billet remained workable at $455-460/t CFR, though deals were limited due to Republic Day holidays and weak rebar sales. Some suppliers floated offers to Egypt at $470/t CFR (around $440/t FOB) for December shipment. With sellers turning slightly bullish, CIS billet export prices were assessed at $438-440/t FOB.

Despite tight exporter margins, billet prices are likely to stay mostly stable in the coming months. The global scrap market may lend near-term support, with Turkish mills expected to ramp up scrap imports from the US and Europe amid low inventories and reduced winter collection rates.

Asia

Chinese exporters raised billet offers, prompting CIS mills to closely track rouble movements and assess necessary price hikes to offset currency-driven losses. Meanwhile, Asian billet demand in Turkiye is projected to stay firm through year-end, supported by competitive offers from China, Indonesia, and Malaysia, as regional exporters seek overseas buyers amid weak domestic demand and subdued construction activity in China.

Southeast Asia: Southeast Asian billet demand is expected to improve slightly in November-December, aided by the end of the rainy season and modest recovery in construction. However, fragile regional economies and constrained government spending will limit significant consumption growth. Construction in the Philippines, Thailand, and Indonesia is projected to grow by 5-6% by end-2025, though real gains may lag amid fiscal and geopolitical challenges.

In the Philippines, SteelAsia has temporarily halted operations at its Calaca scrap recycling plant, the nation’s only integrated steelworks, with no timeline for resumption. Regional billet prices edged higher to $440-445/t CFR for the Philippines and Indonesia, supported by renewed optimism following US-China trade discussions.

Chinese exporters held firm at over $450/t CFR for 3SP-grade billet, while buyers remained near $440-445/t CFR.

GCC: Billet prices across the Gulf remained stable through October amid thin buying and narrow producer margins. Chinese and Indonesian billets were offered at $465/t and $470/t CFR, respectively, while Emirati and Qatari mills maintained offers at $500/t and $490/t CPT, with Saudi domestic billet at $475-480/t exw.

Regional producers, operating between $450-500/t exw, are expected to maintain current offers unless Asian prices soften.

Weak construction sentiment in Southeast Asia and rising finished steel inventories in China pressured offers, but further declines were capped by tight margins — Chinese export costs are estimated at around $452-455/t CFR, and Indonesian around $430-435/t CFR.

Iran: An Iranian producer concluded an export tender this week, selling 20,000 t of commercial-grade billets at $416/t FOB for December shipment. Further deal details are expected following recent trade discussions between Iranian, Chinese, and Indian buyers at a regional symposium.

The latest indicative levels were as follows: billet $416-420/t FOB, slab $410/t FOB, and rebar $400-410/t exw.

China: China’s billet and rebar markets showed mild gains as supply curbs and firmer raw material costs offset weak steel demand. Tangshan billet rose RMB 50/t ($7/t) w-o-w to RMB 2,980/t ($420/t), while SHFE January 2026 rebar gained RMB 48/t ($8/t) to RMB 3,106/t ($437/t). Although sentiment improved slightly, construction demand remains sluggish, limiting further upside. Prices are expected to remain range-bound in early November, as optimism from policy cues meets resistance from weak real demand.

Leave a Reply