- Indonesia-India rates hit over 1-month low

- Market sentiment muted on slow post-festive demand

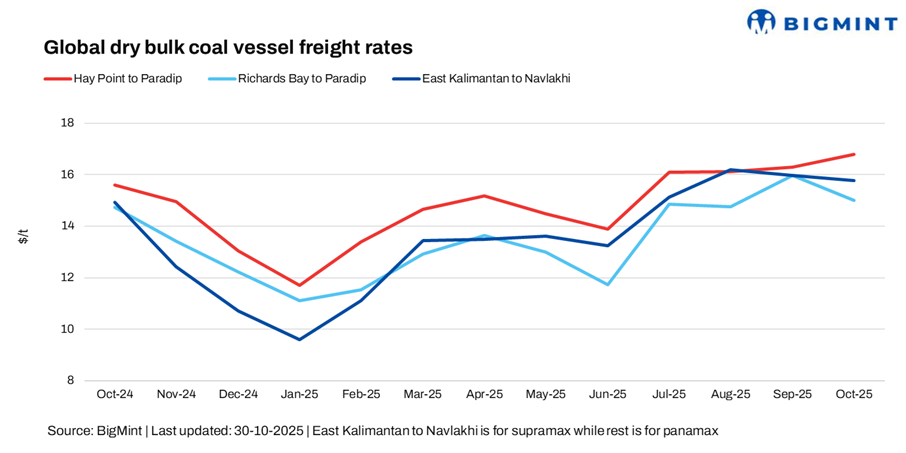

India’s seaborne coal freight market witnessed a mixed trend this week, with rate movements varying across major routes. While Panamax freights on the Australia-India corridor remained firm amid a few decent fixtures and steady tonnage demand, the South Africa-India route held largely stable in the absence of fresh inquiries. In contrast, Supramax rates on the Indonesia-India route continued to soften due to muted activity and weak cargo flow. Overall market sentiment stayed cautious, shaped by limited post-festive recovery in industrial demand and steady portside coal inventories across key Indian ports.

“Market activity remained sluggish in the aftermath of the festive holidays, while cyclone-related disruptions along India’s east coast further constrained trading operations”, source said.

Coal freight rates on the Australia-India route held firm this week, supported by a few decent fixtures despite a noticeable drop in overall activity compared to the previous week. Limited fresh inquiries kept trading volumes muted, yet the available fixtures were concluded at relatively higher levels, indicating underlying strength in market sentiment and a tighter tonnage supply in the region.

Freight rates on the South Africa-India route remained stable w-o-w, as limited market activity and a persistent shortage of fresh coal cargo inquiries kept sentiment subdued. BigMint reported only a single fixture concluded at around $14.28/dry metric tonne (dmt), though specific details regarding the vessel size and laycan period were not disclosed within the publishing window. Overall, the route continued to face muted demand, with charterers adopting a wait-and-see approach amid soft market fundamentals.

Supramax freight rates on the Indonesia-India route extended their downward trend w-o-w, weighed by subdued activity and limited fresh coal cargo inquiries. Market sentiment across the Indian Ocean remained largely stagnant, as both charterers and owners adopted a cautious stance amid soft demand and steady vessel supply. Overall, the region saw minimal momentum, with most lanes maintaining a flat tone through the week.

Meanwhile, India’s portside thermal coal inventories remained broadly steady in week 43 (ending 26 October), inching up 1.2% w-o-w to 13.33 million tonnes (mnt) from 13.17 mnt in week 42. The marginal rise was supported by slight restocking activity at select eastern and western ports, even as trading stayed muted amid slow post-festive industrial recovery.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up w-o-w by around 0.16/dmt to $17.66/dmt. “Out of Australia, a steady flow of fresh cargoes emerged during the latter half of Asian trading hours, boosting tonnage demand and lending support to overall market sentiment”, a Mumbai-based shipbroker told BigMint.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route remained stable at $14.80/dmt. Another source said, “Fixing activity out of South Africa remained limited, with scarce market information highlighting subdued demand and cautious market sentiment amid steady vessel availability. Additionally, weaker sponge iron prices further dampened buying interest, keeping freight rates under pressure.”.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: “No new voyage fixtures were reported on the Indonesia-India coal route during Asian trading hours, as market activity remained muted and participants refrained from fresh commitments amid weak demand”, a source told BigMint. Supramax coal freights on the Indonesia to India route stood at $14.43/dmt, a w-o-w decrease of $1.07/dmt, hitting one-month low.

Meanwhile, Brent crude oil futures dropped by about $1.77/barrel (bbl) w-o-w to $63.74/bbl on 30 October 2025. The fall was driven by persistent concerns over slowing global demand and ample supply from key producers. Additionally, rising US inventories and subdued refinery activity weighed on market sentiment, while geopolitical risks offered only limited price support through the week.

Outlook

The near-term outlook for dry bulk coal freight remains cautiously steady, with mixed trends expected across key routes. Demand from India is likely to offer some support, particularly for Panamax and Supramax segments, as utilities continue to replenish stocks ahead of seasonal demand. However, the overall pace of fixtures may stay moderate amid lingering supply-side pressures and fluctuating bunker prices.

Meanwhile, sentiment could face intermittent headwinds from geopolitical uncertainties and weather-related disruptions affecting port operations and vessel availability. While freight levels may see short-term volatility, market fundamentals suggest a broadly range-bound trend in the immediate term.

Leave a Reply