- Festive holidays keep buying need-based

- Lower raw material tags pull down prices

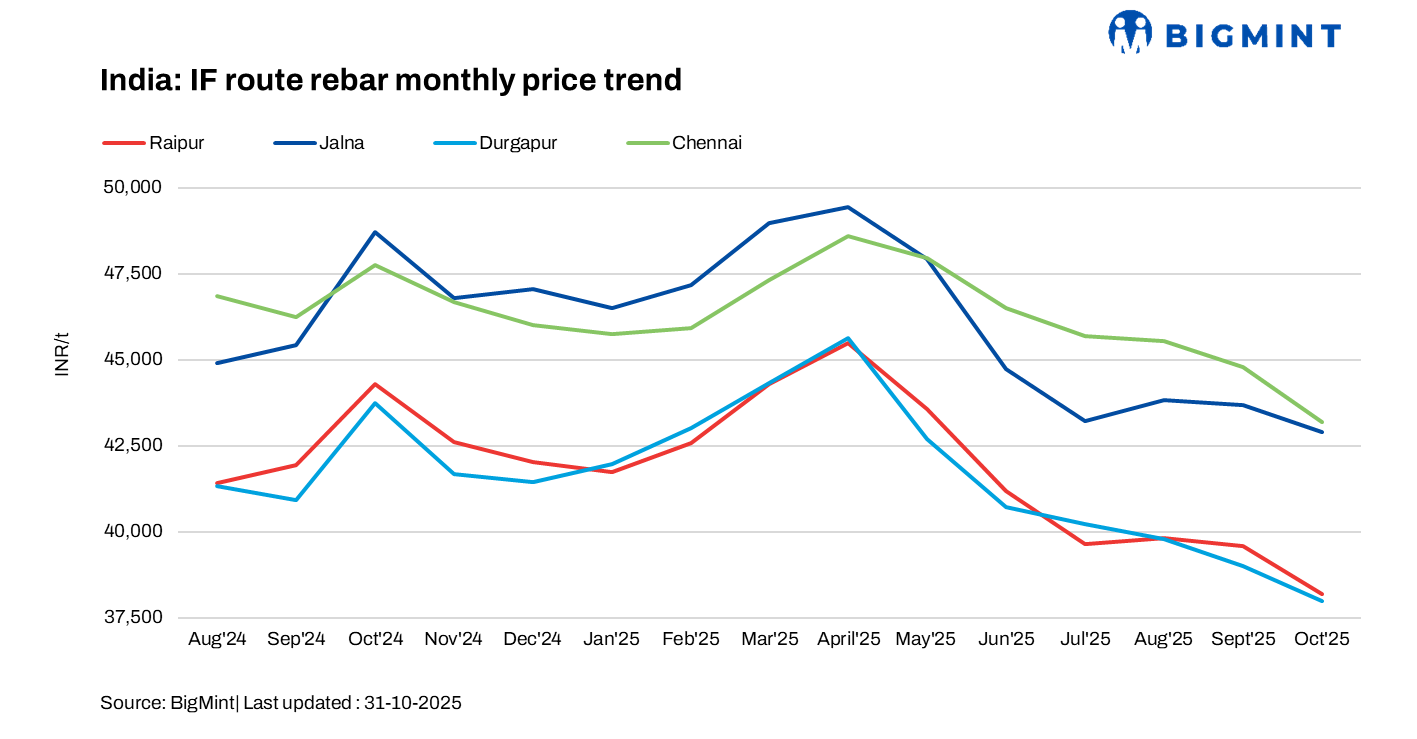

India’s induction furnace (IF) rebar prices witnessed a downtrend in October 2025, in the range of INR 100-2,000/tonne (t) m-o-m across regions, as per Big Mint’s assessment.

The market witnessed a slowdown in October, as weak sentiment and limited customer inquiries led to sluggish order bookings. Most buyers restricted purchases to immediate requirements amid the Diwali festive holidays and subdued finished steel demand. The decline in raw material prices, particularly sponge iron and billets, added further pressure on sentiment, keeping overall market activity muted.

To stimulate sales and manage inventories, manufacturers reduced offers and extended trade discounts. Inventory levels were at around 15-17 days in October.

As per Joint Plant Committee (JPC) data, India’s total rebar production through the IF and BF routes stood at 38.9 million tonnes (mnt) in April-September of FY’26, marking a significant 8% rise from around 35.9 mnt in the same period of FY’25, indicating continued growth momentum.

Region-wise price movements

Prices saw a downward movement across all major regions during the month. The southern region witnessed the highest declines, with Bangalore and Hyderabad recording m-o-m drops of INR 2,000/t and INR 1,300/t, respectively, while the Chennai market slipped by INR 800/t.

In the eastern region, Rourkela recorded a drop of INR 1,000/t, and Durgapur saw a decrease of INR 800/t. In central India, prices experienced a decline of INR 400/t in Raigarh, while Raipur, a key production hub, saw a reduction of INR 1,100/t m-o-m.

The northern region witnessed notable declines, with the Delhi market down by INR 800/t, while Jaipur saw a reduction of INR 1,100/t.

In the western region, prices in Mumbai and Jalna were down by INR 700/t and INR 100/t, respectively, while Goa recorded a marginal gain of INR 200/t.

Factors impacting market

Raw material prices drop m-o-m: The drop in finished steel prices was driven by lower prices of key raw materials, steel billets and sponge iron, used in IF-route production. Dull buying interest and slow trade activity across several markets prompted manufacturers of both commodities to reduce their prices.

Considering Raipur as the benchmark, billet prices declined by INR 600/t m-o-m to INR 36,150/t exw, while sponge iron (PDRI FeM 80% ±1) saw a drop of INR 700/t m-o-m to INR 24,100/t exw (prices taken from 30 September to 31 October 2025).

Demand slows down: Market activity remained subdued during the festive holidays, with most buyers restricting purchases to immediate requirements and avoiding bulk bookings. Moreover, weak demand in the finished steel segment, sluggish construction activity, and labour shortages further dampened sentiment, resulting in a slowdown in overall material procurement.

BF-route rebar prices hold firm m-o-m: Trade level BF-rebar prices remained stable m-o-m at an average of INR 47,100/t exy-Mumbai amid slow domestic demand in October 2025. Domestic steel demand remained subdued due to logistical challenges, labour shortages, and the festive season, which kept buyers cautious. Major mills either reduced prices or offered discounts amid weak market sentiments.

In the projects segment, prices declined by 500/t m-o-m to an average price of INR 45,500-46,000/t FOR Mumbai.

Outlook

With the festive season now over, domestic steel prices are likely to witness a gradual recovery, supported by firming raw material costs. The resumption of construction activities is also expected to lift demand in the coming days. Market sentiment has already started showing signs of improvement over the past few days, and this positive momentum is expected to strengthen further, leading to a rebound in prices.

Leave a Reply