- Pacific: Sentiment remains bearish amid elevated vessel supply

- Atlantic: Activity stays muted due to limited cargo offers

The dry bulk iron ore freight market witnessed a broad-based decline this week across major routes, weighed down by muted cargo demand, ample vessel availability, and subdued chartering activity. Both Capesize and Supramax segments experienced notable rate drops, particularly on key lanes such as Australia-China, Brazil-China, South Africa-China, and India-China, as weak trading momentum and limited fresh fixtures kept sentiment under pressure. The overall market tone remained bearish, further reinforced by falling FFA rates and bunker prices, while the Baltic Dry Index also retreated amid soft fundamentals and oversupply concerns.

At the start of the week, Capesize freight offers to iron ore miners on the Western Australia-Qingdao route were reported at the higher end, around $10.15 per dry metric tonne (dmt). As the week advanced, sentiment weakened amid limited fresh demand and softening market activity. Reports indicated that miners managed to fix a Capesize vessel at approximately $9.7/dmt for a November 2025 laycan, reflecting the downward pressure on rates. By late Asian trading hours, both bid and offer levels continued to decline, slipping to around $9.6/dmt and eventually easing further to nearly $9.25/dmt, as market participants adjusted to the persistent weakness in chartering interest and growing vessel availability.

Trading activity remained subdued through much of the Asian session, with little movement observed in the market. “Not very exciting,” remarked a ship operator, noting that overall conditions appeared largely flat for the day.

Meanwhile, both forward freight assessments (FFA) rates and bunker prices faced downward pressure this week, reflecting a generally softer market tone. The decline in FFAs indicated weaker sentiment among market participants, as slowing cargo demand and limited fresh fixtures weighed on near-term expectations. At the same time, bunker fuel prices eased across major ports, supported by lower crude benchmarks and steady supply, offering slight relief on operating costs but underscoring the overall bearish trend in the shipping market.

Following this, freight rates on the Brazil-China and South Africa-China routes weakened this week as sentiment in the Atlantic basin turned increasingly soft. Limited iron ore cargo inquiries from Brazilian and South African miners, coupled with an oversupply of available tonnage, put downward pressure on Capesize earnings. Muted chartering activity further contributed to the decline, with market participants reporting a lack of fresh fixtures and growing uncertainty over near-term demand. Overall, the Atlantic market remained sluggish, reflecting subdued trading momentum and weaker fundamentals.

The India-China Supramax freight market for iron ore remained subdued this week, weighed down by multiple regional factors. The extended holiday period across parts of Asia led to reduced trading activity, while an ample tonnage list continued to exert downward pressure on rates in both regional and Indian Ocean markets. Despite earlier expectations of a recovery, the market failed to gain traction, with sentiment turning increasingly weak as iron ore demand slowed considerably.

A major Indian steel maker mentioned, “Freight levels fell sharply from around $11.90/dmt in the previous week to about $10.48-10.50/dmt, marking a significant w-o-w decline. Over the past two to three weeks, the market has shown heightened volatility, with frequent fluctuations in rates amid unstable demand.”

“The global appetite for iron ore has remained muted, though some participants anticipate a possible pickup in Indian iron ore exports by early to mid-November, which could lend limited support to the market”, said a Mumbai-based shipbroker to BigMint.

Route-wise updates

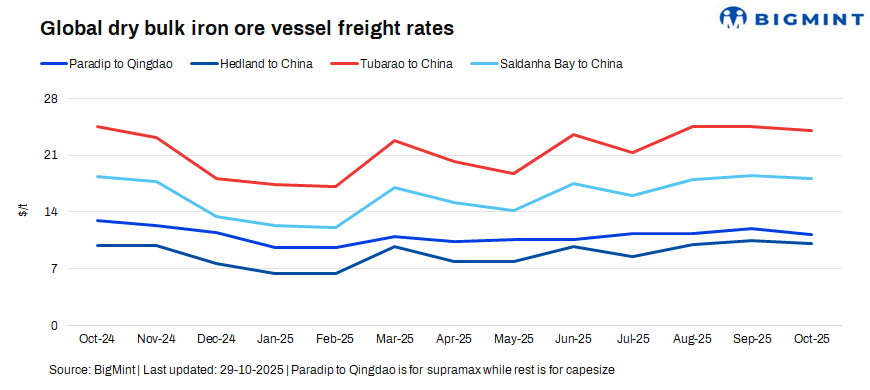

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China witnessed a w-o-w decrease of $1.4/dmt to $10.50/dmt.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China fell by $1.4/dmt w-o-w to $9.30/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments witnessed a drop of of $1.9/dmt w-o-w, settling at $22.50/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao edged lower by $1.3/dmt w-o-w, settling at $17/dmt.

Market highlights

- Baltic index edge lower on soft demand, vessel oversupply: The Baltic Exchange’s main dry bulk sea freight index posted a sharp w-o-w decline amid weakening vessel segments on weak cargo demand, vessel oversupply, and subdued chartering activity. As of 28 October, the overall index fell by about 107 points to 1,950. The Capesize segment decreased sharply w-o-w by 275 points to reach 2,784. Similarly, the Supramax index continued to slide, by 28 points w-o-w to 1,350.

- Brent crude futures strengthen on supply concerns: Brent crude oil futures climbed down about $1.51/barrel (bbl) w-o-w to $64/bbl on 29 October. Brent crude oil futures eased this week amid weaker global demand sentiment and a firmer U.S. dollar. Rising inventories and steady supply from key producers further weighed on prices, while easing geopolitical risks kept market sentiment cautious.

Outlook

The near-term outlook for dry bulk iron ore freight remains cautiously soft, with rates likely to face continued pressure amid muted cargo demand and an oversupplied tonnage list. Activity out of key exporting regions such as Brazil and Australia has been limited, while slower Chinese steel production and subdued restocking interest have weighed on sentiment.

However, some seasonal demand recovery could emerge in the coming weeks as charterers return from holidays and weather-related disruptions begin to affect vessel schedules. Any rebound, though, is expected to be modest, with overall market direction hinging on Chinese import appetite and miner shipment volumes.

Leave a Reply