- Combined increase in China, DRC stands at 9%

- Japan’s output falls 8% due to smelter maintenance

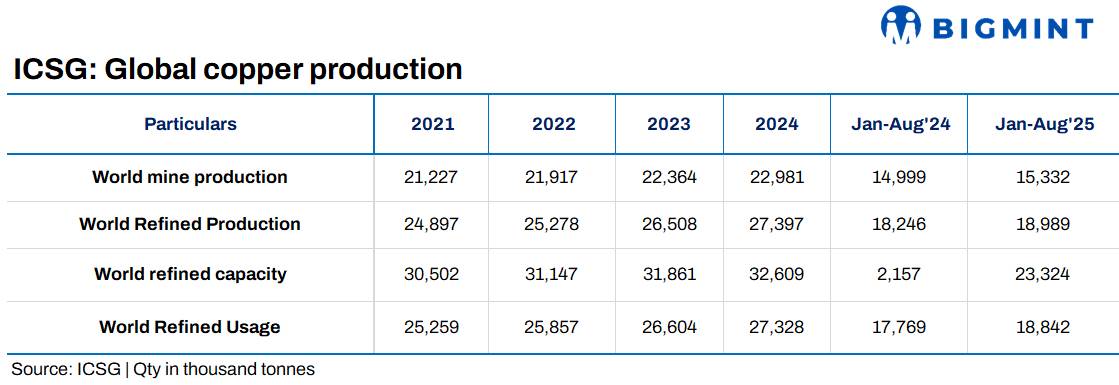

The International Copper Study Group (ICSG) has released preliminary data for January-August 2025, indicating that global refined copper production grew approximately 4% y-o-y. This included a 3.9% increase in primary production (from ores via electrolytic and electrowinning processes) and a 5% rise in secondary production (from scrap).

Regional trends in refined copper production

The growth in global refined copper production during the first eight months of 2025 was largely driven by China and the Democratic Republic of Congo (DRC), which together accounted for about 57% of global output and saw a combined increase of 9% (China +9%, DRC +8%). Excluding these two countries, world refined copper production declined by approximately 2%.

In Asia (excluding China), output fell by 4.7%, mainly due to lower production in Japan and the Philippines. Japan’s refined copper production dropped by 8% following smelter maintenance shutdowns, while the Philippines saw a sharp decline of 64% as a result of the Pasar refinery closure. In Indonesia, the Amman refinery produced its first cathode in late March, and the Manyar smelter/refinery commenced production in July. India recorded a 22% increase in output, driven by improved operating capacity rates.

Chilean refined copper production declined by 10%, with electrolytic production from concentrates down 12.5% due to smelter maintenance, and solvent extraction-electrowinning (SX-EW) output falling 8.5%.

Meanwhile, global secondary refined copper production (from scrap) increased by 5%, primarily supported by higher output in China.

Copper mine output up

Global copper mine production increased by about 2.2% y-o-y in the first eight months of 2025, with concentrate output rising 2.1% and SX-EW up 2.8%, supported by ramp-ups at new projects and improved performance at several operating mines.

Chile’s mine production rose by 1%, driven by higher output at Escondida, Centinela, Mantos Copper, and Codelco, which more than offset declines at Collahuasi, Los Pelambres, and several smaller mines.

In Peru, copper mine production increased by 2.6%, led by significant gains at Las Bambas and Toromocho that outweighed reductions at Cerro Verde, Antamina, and Antapaccay.

The DRC saw an 8% rise, mainly due to expansions at the Kamoa mine (concentrates) and the Tenke/Kisanfu operations (SX-EW).

Mongolia’s copper concentrate production surged 34% as a result of the ramp-up at the Oyu Tolgoi underground project.

Meanwhile, Indonesian output fell by 30%, largely due to planned major maintenance at Grasberg and lower production at Batu Hijau owing to mine sequencing.

Refined copper usage grows

Preliminary data suggests that global apparent refined copper usage rose by about 6% y-o-y in the first eight months of 2025.

China’s apparent demand increased by around 9%, while net refined copper imports fell by 1.5% as imports rose 1% and exports grew 15%. China’s share of total world refined copper usage remains at approximately 58%.

Global consumption outside China increased by about 1.6%, with gains in several Asian and MENA countries offsetting weaker demand in the EU and Japan.

Market surplus rises

The global refined copper market recorded an apparent surplus of about 147,000 t. Adjusting for estimated changes in Chinese bonded inventories, the world refined copper balance suggests a market surplus of approximately 208,000 t.

Copper prices

The average LME cash price for September was $9,952.73/t, up 3.2% from the August average of $9,645.85/t. The highest price in 2025 was $10,866.50/t on 9 October, while the lowest was $8,539/t on 9 April. The year-to-date average price stands at $9,623.54/t, 5.2% higher than the 2024 annual average.

China’s bonded stocks are estimated to have increased by around 61,000 t compared to end-2024 levels. Combined copper stocks at the major metal exchanges (LME, COMEX, and SHFE) stood at 530,651 t at the end of September, up 23.3% (100,423 t) from December 2024. Stocks fell at the LME by 129,625 t while rising at COMEX by 209,186 t and at SHFE by 20,862 t.

Leave a Reply