- Three-month LME zinc contract gains 2.51%

- MCX tags rise on improving global sentiment

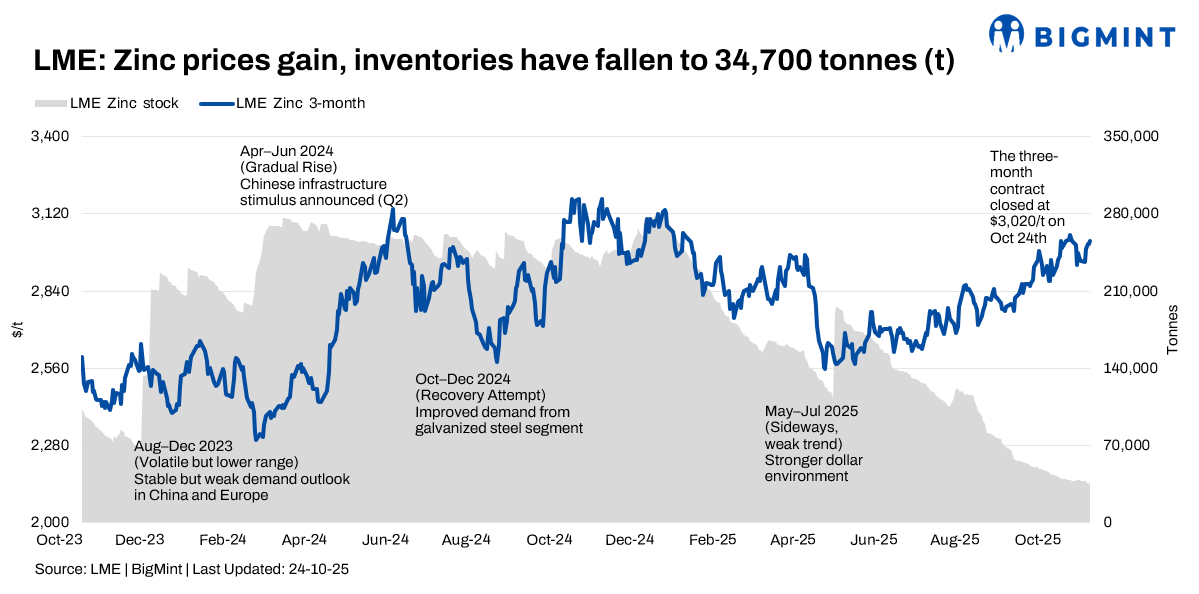

The London Metal Exchange (LME) zinc market witnessed strong upward momentum during Week 42, driven by continued supply-side support and firm fundamentals. Prices surged to multi-month highs, although they faced some profit-taking towards the end of the week. Critically low LME inventories provided significant underpinning for the rally, but macroeconomic volatility and mixed demand signals added an element of caution.

Price trends

LME zinc cash-settlement prices trended sharply higher throughout the week. Prices opened the week at $3,159/t on 20 October and saw a sustained rally, hitting a peak of $3,326/t on 21 October before closing lower at $3,227/t on 24 October. This represents an impressive increase of 2.15% for the week. The three-month LME zinc contract mirrored this pattern, starting at $2,946/t on 20 October and closing higher at $3,020/t on 24 October, a 2.51% gain.

Inventory analysis

LME zinc inventories continued their declining trend, providing a strong support factor for prices. Stocks fell from 37,325 t on 20 October to 37,275 t on 21 October, 35,300 t on 22 October, and 34,700 t on 23 October, before a slight rebound to 37,600 t on 24 October. The overall trend of critically low inventories, representing less than one day of global demand, remains a key driver of the market. Additionally, Chinese domestic inventories, particularly in the bonded zone, declined during the week, suggesting stronger import demand.

MCX zinc trends (20-24 October)

MCX zinc prices experienced a strong upward trend, aligning with global supply-side support. MCX zinc futures saw significant gains. For instance, the October contract closed at INR 294,200/t on 20 October and closed higher at INR 299,650/t on 24 October, an increase of 1.7%. The Indian market benefited from the improving global macroeconomic sentiment, tightening LME inventories, and strong domestic demand from consuming industries.

SHFE zinc trend

SHFE zinc prices were influenced by the global rally but also by domestic factors, with an overall increase. The most-traded SHFE zinc 2512 contract hovered at high levels throughout the week, opening at RMB 22,345/t and closing at RMB 22,355/t on 24 October. This demonstrated strength despite mixed demand signals. Despite concerns over tepid domestic demand, the market was supported by tightening supply conditions and macro events influencing sentiment.

The SHFE/LME price ratio fluctuated, with the zinc ingot export window opening, suggesting that Chinese domestic zinc prices were high relative to LME, making exports potentially profitable.

Global zinc surplus – ILZSG

According to the International Lead and Zinc Study Group (ILZSG), global refined zinc demand is forecast at 13.71 million tonnes (mnt) in 2025, rising to 13.86 mnt in 2026, while production will likely reach 13.80 mnt in 2025 and 14.13 mnt in 2026, creating surpluses of 85,000 t and 271,000 t. China’s slowdown is expected to offset a modest European recovery. For India, softer global prices may support galvanising and infrastructure demand amid steady imports.

Outlook

The near-term zinc outlook remains cautiously optimistic, driven by critically low LME inventories and continued supply-side support. However, volatility is expected due to the sustainability of Chinese demand and potential shifts in macroeconomic factors. Market participants will closely watch for clearer signals of sustained Chinese demand and monitor the balance between tightening refined supply and potentially increasing global mined output, especially ahead of LME Week.

Leave a Reply