- Japan’s aluminium premium declines by 20% q-o-q in Q4CY’25

- Weak demand from construction, automotive sectors persists

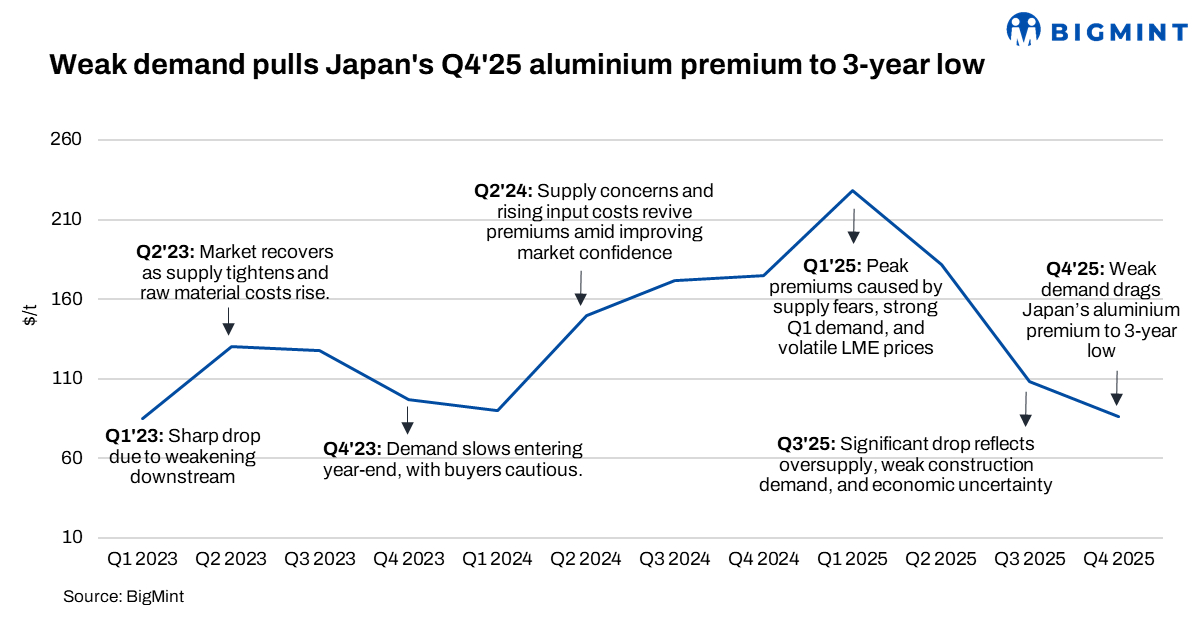

Japan’s premium for imported primary aluminium for the fourth quarter of 2025 has been set at a three-year low of $86/t over the London Metal Exchange (LME) cash price, CIF main Japanese ports. The new rate marks a 20% decline from the previous quarter’s $108/t, reflecting subdued demand across key consuming sectors, according to sources directly involved in the quarterly pricing negotiations.

The latest settlement represents the third consecutive quarterly drop and came in below producers’ initial offers of $98-103/t. The Q4 premium was established based on a few trades conducted earlier this week, covering a minimum of 13,000 t per month of seaborne P1020/P1020A aluminium ingots for loading between October and December.

Negotiations, market sentiment

During the negotiation period, offers ranged between $92-103/t, while buyers’ expectations remained largely in the low $80/t range amid limited spot activity.

Weak consumption in Japan’s construction and automotive industries weighed heavily on buying interest. Market participants noted that the auto sector had earlier been hit by the 25% US automotive tariffs introduced in April, which were later reduced to 15% in September, providing slight optimism for a modest recovery in the coming months.

Supply-side developments in Asia

On the supply front, new capacity additions in Indonesia are shaping regional market dynamics. The Xinfa Group-Tsingshan Industrial aluminium smelter began operations in the third quarter and is currently running at half of its 500,000 t/year first-phase capacity. The remaining capacity ramp-up is expected to continue through late 2025 and into 2026.

Meanwhile, PT Kalimantan Aluminium Industry (KAI), backed by PT Alamtri Resources Indonesia (formerly Adaro Energy), plans to start its first production phase by end-2025. However, market participants expect commercial volumes to enter the market only by Q2CY’26, as part of a broader 1.5 mnt/year capacity project to be executed in three phases.

Mixed outlook for Asian aluminium market

The regional outlook remains uncertain. Some traders anticipate that potential production cuts — particularly at South32’s Mozal Alcantara smelter in 2026 due to power constraints — could tighten supply and lend support to premiums in Asia. Others, however, remain cautious, citing high port inventories and slow demand across Asia.

At the end of September, aluminium port stocks in Japan stood at 341,300 t, up 1.8% m-o-m and 9% y-o-y. Market participants warned that the current stock build-up could limit price recovery, despite temporary boosts from European premium trends linked to the upcoming Carbon Border Adjustment Mechanism (CBAM) in 2026.

Looking ahead

Japan’s Q4 aluminium premium decline signals persistent weak demand from the construction and automotive sectors. While regional supply is set to rise with new Indonesian smelters, high inventories and slow consumption may cap price recovery. However, potential global supply disruptions and easing tariffs could provide limited support to Asian aluminium premiums in early 2026.

Leave a Reply