- Retail sales improve during festive season, aided by discounts

- GST 2.0 tax cuts considerably enhance vehicle affordability

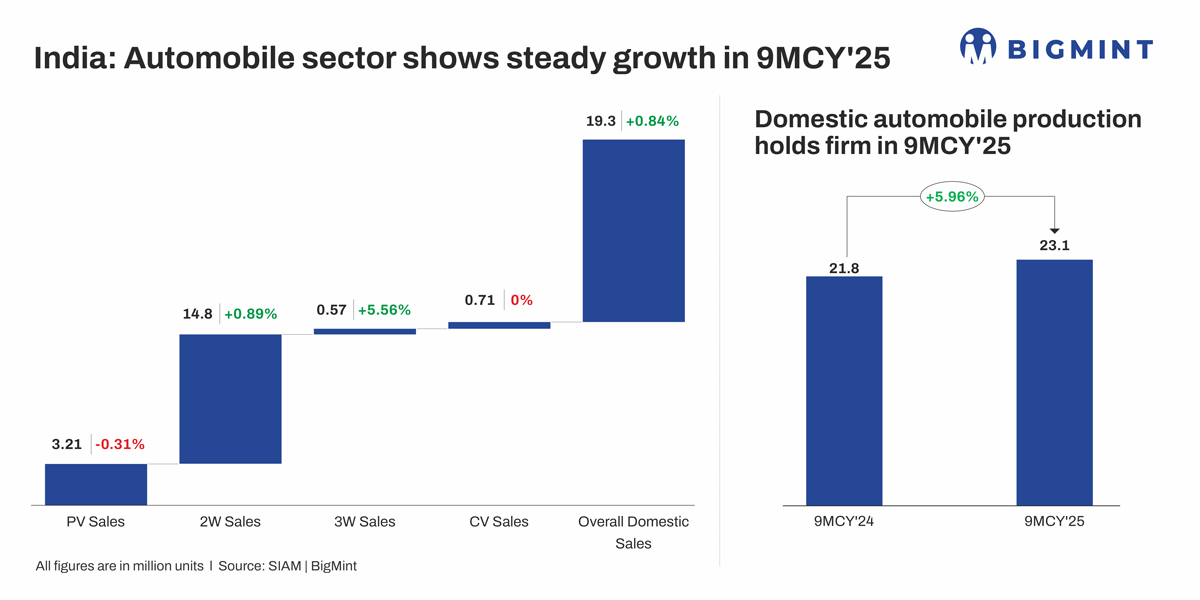

India’s automobile sector recorded a stable performance in 9MCY’25 compared to 9MCY’24, according to SIAM OEM data. Passenger vehicle sales edged down 0.31% y-o-y to 3.21 million units, while two-wheeler sales rose 0.89% to 14.8 million units. Three-wheeler sales increased 5.56% to 0.57 million units, and commercial vehicle (CV) sales remained unchanged at 0.71 million units. Domestic sales were up 0.84% y-o-y to 19.3 million units, with total production climbing 5.96% to 23.1 million units, indicating strong manufacturing momentum.

The steady overall performance was supported by rising rural and semi-urban demand, particularly for two- and three-wheelers, aided by improved rural income and last-mile transport needs. A surge in export orders and government incentives under the Production-Linked Incentive (PLI) scheme encouraged OEMs to ramp up output, boosting factory utilisation even amid moderate domestic demand.

Additionally, easing semiconductor shortages and localisation of component manufacturing enhanced production efficiency. However, a marginal decline in passenger vehicle sales reflected a shift in consumer preference towards premium and SUV models, leading to slower growth in entry-level car demand. Overall, the sector maintained balance, with production gains driven by export strength and policy support.

Meanwhile, FADA retail data painted a more positive picture. Passenger vehicle retail sales grew 5.23% y-o-y to 3.02 million units, while two-wheeler sales rose 1.70% to 13.19 million units. Three-wheeler and CV sales also expanded by 3.37% and 4.05%, respectively. Tractor sales improved 4.62% to 0.68 million units, pushing total retail sales up 2.54% y-o-y to 18.58 million units, reflecting firm consumer demand across categories.

The festive season, particularly Navratri and Diwali, encouraged higher footfalls and boosted consumer sentiment, aided by attractive offers, new product launches, and easier financing options. The recent GST 2.0 revision, which reduced tax rates on small cars and two-wheelers, further improved affordability and spurred retail activity during September and October. Together, these factors encouraged both first-time buyers and upgraders to make purchase decisions earlier than planned, strengthening overall retail performance.

Rural and semi-urban markets also played a vital role in supporting vehicle sales. A good monsoon and higher agricultural output led to better rural incomes, translating into strong demand for two-wheelers, three-wheelers, and tractors. Steady access to finance, stable interest rates, and strong dealer incentives further aided sales. The rise in passenger vehicles, two-wheelers, and tractors points to improving consumer confidence, while higher demand for three-wheelers and commercial vehicles highlights resilience in last-mile transport and logistics. Overall, the increase in retail sales reflects a combination of festive momentum, policy support, and firm rural consumption trends driving India’s automobile sector.

According to FADA Vice President Sai Giridhar, the first three weeks of September were subdued as customers deferred purchases in anticipation of the new GST regime. However, sentiment reversed dramatically in the final week when Navratri festivities coincided with the implementation of lower GST rates, igniting a strong consumer response across segments.

”September 2025 was an exceptionally unique month for India’s automobile retail industry. The first three weeks were largely muted, but the dynamics changed in the final week as festive cheer and GST 2.0 reforms revived sentiment. As a result, the month ended with an overall 5.22% y-o-y growth” Giridhar said.

GST reforms boost auto affordability

The GST 2.0 reduction, which reduced tax rates on small cars and two-wheelers from 28% to 18%, has made vehicles more affordable and spurred consumer demand. This led to higher bookings, especially in the entry-level segment, encouraging earlier purchase decisions and supporting retail growth during the festive season. The increased vehicle sales have also strengthened demand for ADC12 aluminium alloy, widely used in automotive components, driving production and reinforcing its role in India’s automotive manufacturing sector.

Impact on aluminium ADC12 alloy

Following the recent GST reductions effective from September 2025, India’s automotive sector has seen a notable surge in demand, especially for small cars, two-wheelers, and commercial vehicles, benefiting from lower tax rates. This policy shift has encouraged higher production and sales, directly boosting the consumption of ADC12 aluminium alloy, which is widely used in automotive components such as engine blocks, transmission cases, and structural parts. The reform has also improved vehicle affordability, accelerated purchase decisions and sustained demand for lightweight, durable materials.

In response, manufacturers have ramped up production of ADC12 aluminium ingots to meet the growing needs of the automotive sector. The combination of GST reforms and strong festive-season demand is expected to maintain robust consumption of ADC12, reinforcing its critical role in supporting India’s automotive manufacturing growth and meeting the requirements for modern, fuel-efficient vehicles.

According to BigMint’s monthly ADC12 assessment, prices of OEM-grade ingots in Delhi and Pune stood at INR 230,000/t and INR 231,000/t in October 2025 in Chennai, all on 30-day payment terms.

Outlook

India’s auto sector is likely to see steady growth in the coming months, driven by festive-season demand, higher rural incomes, and GST 2.0 tax cuts. Passenger vehicles and two-wheelers should gain traction, while CVs and tractors benefit from infrastructure activity and strong rural cash flows. ADC12 aluminium demand is expected to remain robust, supported by stable vehicle production and GST-driven sales, reinforcing its role in manufacturing lightweight, durable automotive components.

Leave a Reply