- SE Asia buyers remain hesitant; freight and demand guiding prices

- Black Sea billet offers up; Russian rouble supports minimal gains

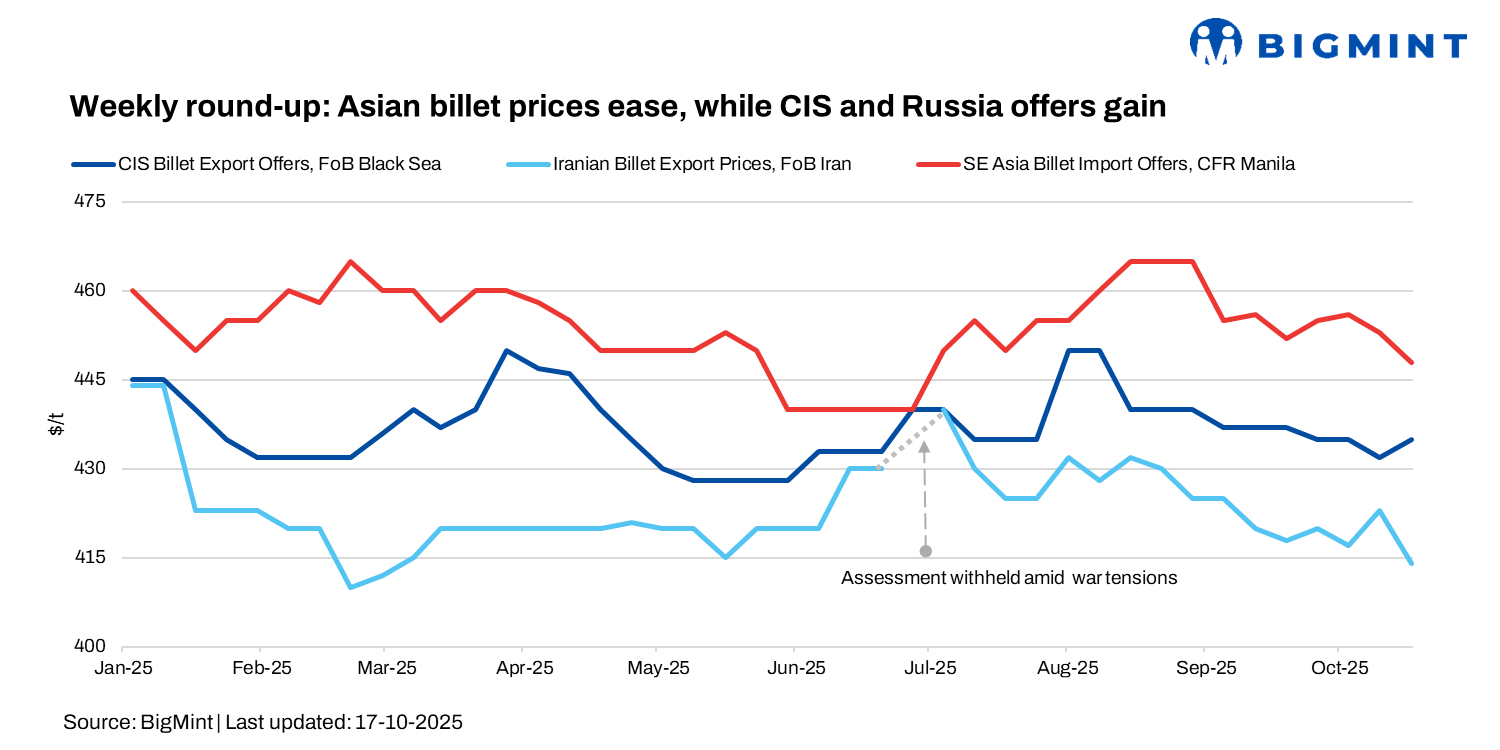

In week 42 of 2025, global billet prices showed a mixed w-o-w trend. CIS and Turkish billets saw a late uptick, while Chinese and Southeast Asian prices softened. Demand remained muted in Southeast Asia, Chinese prices eased, and selective strength emerged outside the region, particularly in the Middle East and Sri Lanka.

Turkiye’s imported scrap market saw a slight uptick, with US-origin HMS 80:20 at $345-353/t CFR. Trading remained limited due to weak downstream demand, high freight costs, and cautious mill buying. Some support came from US cargo bookings and firm dry bulk rates, while currency fluctuations and rising collection costs restrained activity. Buyers stayed hesitant above $350/t, with near-term prices likely guided by freight trends, demand, and US-origin scrap availability.

CIS, Russia

Billet suppliers from the Black Sea region revised their offers over the past week, driven by recent Kardemir semis sales and higher scrap costs. While the strengthening Russian rouble could have supported a larger increase, weak purchase interest capped further rises.

Russian billet for December shipment was offered at $440-445/t FOB Black Sea, up from $435-440/t last week. One insider noted that mills needed to raise prices by around $10/t just to offset the 2.5% exchange rate gain. Export operations at one mill were temporarily halted due to a fire.

In Turkiye, CIS-origin semis were offered at $450-460/t CFR ($430-440/t FOB), while buyers were still targeting $440-445/t CFR ($420-425/t FOB). Some offers even touched $470/t CFR ($450/t FOB).

Chinese, East Asian billet markets

Early in the week, Asian export billet prices were largely stable post-holidays. Chinese 3sp billet was offered at $430-435/t FOB, with bids around $425/t FOB, while Indonesian Dexin Steel quoted $435/t FOB for December. 5sp billet offers in SE Asia ranged $455-460/t CFR, with bids lagging at $445/t CFR, and limited deals mostly from Thai importers. Beyond SE Asia, Chinese billet was offered at $465/t CFR Saudi Arabia, with cautious buyer negotiations.

By mid-week, weaker Chinese demand weighed on prices. Chinese 3sp billet softened to $425-430/t FOB, and Dexin reduced offers to $430/t FOB. Some activity emerged in the UAE and Sri Lanka, with 50,000 t sold to the UAE at $465/t CFR and 45,000 t to Sri Lanka, supported by limited Chinese supply and sluggish rebar demand.

An Indonesian exporter raised January shipment offers to $432-435/t FOB, selling 100,000 t of base grade billet at $430/t FOB for December to Southeast Asia and the Middle East. Chinese 3SP billets remained $426‑430/t FOB, with some unconfirmed deals at $425/t FOB.

In Taiwan, scrap consumers stayed cautious amid slow rebar demand. Late in the week, open-origin 3sp billet traded at $440-445/t CFR a sharp drop of $10/t w-o-w, while China-origin 3sp billets were offered at $435-440/t CFR. A $430/t CFR bid for Chinese semis was reportedly rejected by buyers.

China market

China’s domestic steel market remained weak this week with limited demand and sluggish exports keeping prices under pressure. Tangshan billet prices dropped RMB 40/t ($6/t) w-o-w to RMB 2,930/t ($411/t), while SHFE Jan’26 rebar fell RMB 66/t ($10/t) to RMB 3,037/t ($426/t).

High inventories and slow post-holiday recovery weighed on sentiment, prompting mills to reduce output and offer small discounts of $3-5/t to attract buyers. Port congestion further slowed export movement, while rising coke costs and steady iron ore squeezed mill margins. Prices are expected to fluctuate within RMB 40-50/t next week as mills await policy cues and seasonal demand support.

Iran market

Over the week, billet prices edged down from 374,000 rial/kg ($888/t) to 372,000 rial/kg ($885/t) (-2,000 rial/kg / $5/t), despite limited mill supply and some delivery delays. Rebar prices dipped slightly from 407,000 rial/kg ($966/t) to 405,000 rial/kg ($963/t), while flat products remained firm on rising exchange rates.

Export market: South Kaveh Steel.Co’s tender is expected to close tomorrow (19 Oct) with offers around $410-415/t for November delivery, varying by mill. Mills, currently operating without production issues, are keen to export to offset prior losses.

The short-term outlook is cautiously bullish, supported by export demand. However, gains may be limited by mandated pricing, potential gas cuts, and currency-policy pressures.

Leave a Reply