- Freight rates stable, FOB offers inch up

- Sponge iron prices in India drop w-o-w

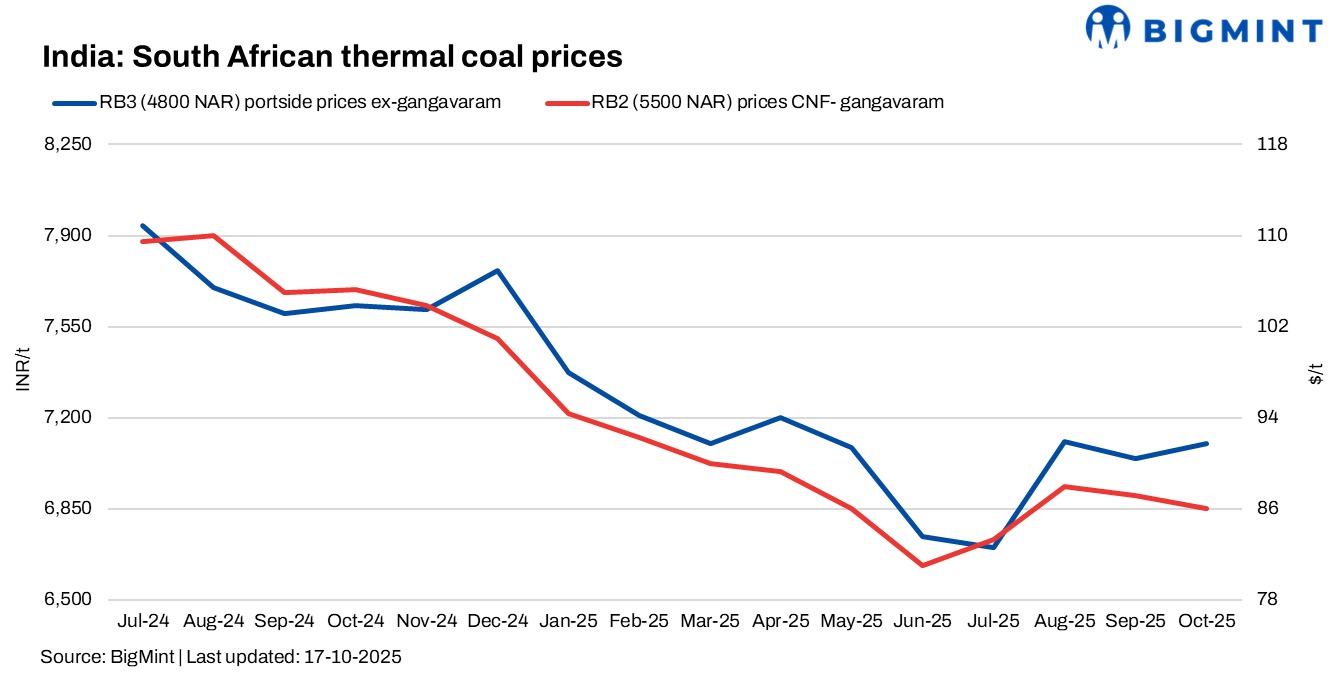

South African portside coal offers in India remained steady this week, with RB2 assessed at INR 8,200/t and RB3 at INR 7,100/t across Paradip, Vizag, and Gangavaram. Although some traders raised RB2 offers to INR 8,500/t following a $2–2.5/t rise in seaborne indices due to geopolitical tensions, no confirmed deals were reported at higher levels.

Market activity stayed subdued. Sponge iron producers continued to operate at reduced capacities due to rainfall and weak steel demand.

Port activity and inventory movement

Portside trading volumes were limited, with reported deals including 2,500 t of RB2 at INR 8,150/t ex-Mangalore, 10,000 t of RB3 at INR 7,000/t, and 12,000 t of RB2 at INR 8,150/t ex-Vizag. Portside thermal coal inventories increased 9% week-on-week to 13.26 mnt in Week 41, up from 12.22 mnt in Week 40, as vessel arrivals improved and stock inflows strengthened at major east coast ports.

Domestic market holds steady

Domestic coal prices remained largely unchanged this week, with 5,000 GCV at INR 6,250/t ex-Bilaspur and 4,500 GCV steady at INR 5,200/t. Market activity stayed limited as delivery orders from previous SECL auctions were delayed. Traders continued to hold back new offers, awaiting clarity from SECL’s upcoming auctions on 24 and 25 October, which together will offer over 860,000 t of coal.

Export and freight updates

Export offers from RBCT rose marginally by $0.5–1/t, with RB2 at $71.5/t FOB and RB3 stable at $60/t FOB. South Africa-India Panamax freight rates were unchanged at around $14.72/t this week, suggesting balanced vessel availability amid steady cargo flow.

Sponge iron market weakens

BigMint’s C-DRI index (ex-Rourkela) fell INR 750/t w-o-w to INR 24,500/t due to continued weak sentiment and slow downstream steel demand. Although sellers refrained from deeper price cuts, overall buying interest remained limited, reflecting persistent caution among end-users.

Outlook

South African coal offers are expected to stay range-bound in the short term. However, rising FOB levels at RBCT and potential vessel congestion could support a mild uptrend in November.

Leave a Reply