- Market stable amid ample stocks, festive slowdown

- Recovery expected post-Diwali from mid-Nov

The Indian portside market for Indonesian-origin thermal coal remained largely stable during the week ending 17 October 2025, as seasonal slowdown and subdued industrial demand kept buying sentiment restrained. With ample inventories and cautious procurement behaviour, traders reported limited price movement across most grades during the week.

Port stocks climb on steady arrivals

India’s portside thermal coal inventories rose 9% w-o-w to 13.26 million tonnes (mnt) in week 41, up from 12.22 mnt in Week 40, supported by regular vessel arrivals and steady inflows at key terminals.

According to market sources, restocking ahead of the winter demand phase provided some support, but overall trading remained limited due to festive closures and reduced industrial activity. In Gujarat, port operations ran below full capacity over the past two weeks, with material lifting remaining sluggish during the festive period.

Market participants anticipate a post-Diwali recovery, with activity expected to resume from Labh Pacham onward and noticeable improvement projected by mid-November.

Prices firm, lower grades see slight easing

According to BigMint assessments, 5000 GAR Indonesian coal prices were unchanged w-o-w at INR 7,100/t (Kandla) and INR 7,050/t (Vizag).

Meanwhile, the 4200 GAR grade remained stable w-o-w to INR 5,800/t (Kandla) and INR 5,700/t (Vizag), and the 3400 GAR grade slipped INR 100/t to INR 4,400/t (Navlakhi). The marginal decline was attributed to ample stock availability and sluggish spot procurement by smaller industrial consumers.

Freight market softens on weak chartering activity

Supramax freight rates on the Indonesia (East Kalimantan)-India (Navlakhi) route edged down $0.06/dmt w-o-w to $16.19/dmt. The Asia-Pacific freight market remained under mild downward pressure due to falling bunker fuel costs and weak chartering demand.

Market activity across Indian Ocean routes stayed muted, with limited new fixtures and broadly flat sentiment prevailing among shipowners and charterers.

Domestic coal stocks at power plants edge up

Coal inventories at Indian power plants improved slightly to 44.67 mnt as of 15 October, equivalent to roughly 15 days of consumption. Despite the improvement, 17 power stations remained under critical stock conditions – including 13 domestic-coal-based units and four reliant on imports.

The rise reflects better coordination in coal movement by domestic producers, though logistical bottlenecks and weather disruptions continue to constrain regional supplies.

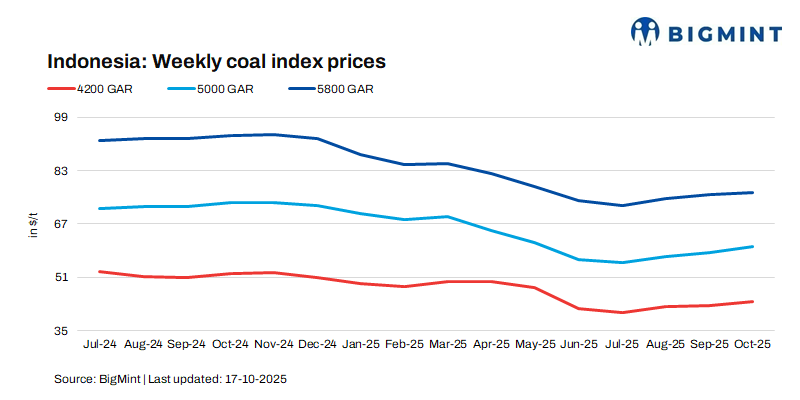

Seaborne prices inch up

In the seaborne market, Indonesian coal prices posted minor week-on-week gains amid firm buying from Asia. The 5800 GAR grade rose $0.98/t to $77.18/t, the 4200 GAR grade climbed $1.32/t to $44.35/t, and the 3400 GAR grade increased $0.54/t to $31.14/t.

The uptrend was driven by renewed procurement from China and Southeast Asia and limited low-CV cargo availability, though gains were capped by soft freight rates and balanced supply conditions.

Outlook

India’s portside thermal coal market is expected to stay range-bound amid ample stocks and festive demand lull, with activity likely to revive post-Diwali. Freight softness and firm Indonesian prices suggest a gradual recovery from mid-November.

Leave a Reply