- Australia holds firm despite selective buying by Asian utilities

- Indonesian loading activity strengthens post-holiday break

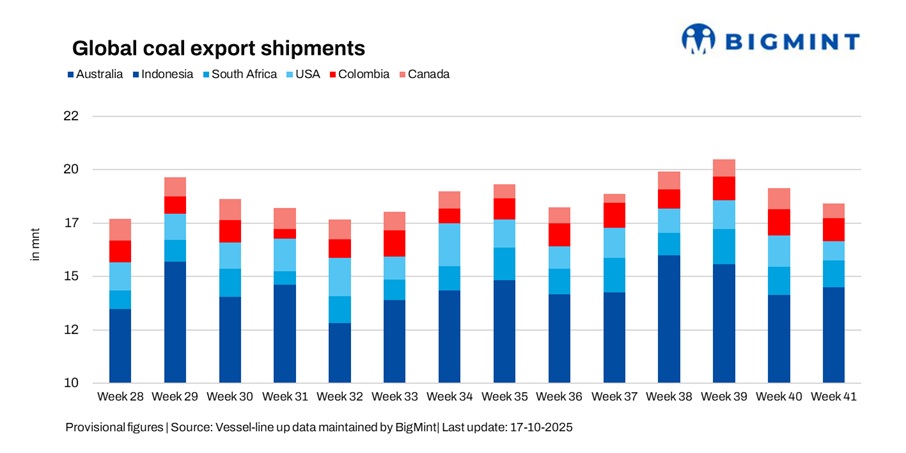

Global seaborne coal exports edged lower by 3.7% w-o-w to 18.08 million tonnes (mnt) in Week 41 (04-10 October 2025) from 18.78 mnt in Week 40 (27 September-03 October 2025), according to BigMint’s vessel line-up data. The overall decline was led by steep reductions in US and Canadian shipments, which outweighed a modest rebound from Indonesia and stability in Australian volumes. South Africa and Colombia also registered softer flows amid lacklustre fixture activity.

Market sentiment remained cautious through the week, as limited fixtures, weak terminal performance in the Atlantic basin, and freight volatility capped export momentum. In contrast, Indonesia’s shipments gained modestly, supported by improved vessel scheduling and resumed loading post-holiday, while Australia’s exports stabilised following consecutive declines.

Country-wise trends

Australia’s coal exports were largely stable, easing marginally by 0.3% w-o-w to 7.16 mnt in Week 41 from 7.19 mnt in Week 40. Shipments from key terminals such as Newcastle (3.07 mnt), Taboneo (2.59 mnt), DBCT (1.44 mnt), and Gladstone (1.34 mnt) showed minimal movement. Vessel arrivals were steady, but fixtures stayed limited, reflecting cautious buyer sentiment and selective procurement by Asian utilities. Demand from Japan (3.24 mnt) and China (3.20 mnt) continued to anchor flows, although Indian buying remained subdued at 2.30 mnt.

Australia’s coking coal market exhibited tentative signs of stabilisation, supported by firmer demand from northeast Asia and consistent export performance. However, muted global steel production and broader market uncertainties may constrain recovery prospects. Going forward, sustained Chinese demand and a potential pick-up in Indian buying will be critical in determining the pace of momentum in Australia’s coal trade.

Indonesia’s coal exports rose 5.5% w-o-w to 7.15 mnt in Week 41 from 6.78 mnt in Week 40, driven by smoother vessel scheduling and a pick-up in post-holiday loading activity. Key terminals such as Taboneo (2.59 mnt), Samarinda (0.93 mnt), and Bunati (0.64 mnt) recorded higher throughput as charterers resumed spot inquiries following the festive break. However, overall gains remained capped by subdued industrial coal demand and cautious restocking sentiment in India.

On the demand side, Japan led imports at 1.55 mnt, followed by China (1.17 mnt), India (1.08 mnt), and South Korea (0.79 mnt). Despite continued softness in Indonesia-India freights, the w-o-w rebound underscored steady miner output and improved port efficiency, as accumulated backlogs were cleared and vessel availability normalised.

US coal exports plunged 37.8% w-o-w to 0.87 mnt in Week 41 from 1.39 mnt in Week 40, as reduced vessel nominations and weaker loadings at major ports weighed on overall volumes. Norfolk (0.37 mnt) accounted for the bulk of shipments, while Mobile and Baltimore handled around 0.14 mnt each, reflecting the impact of logistical bottlenecks and soft Atlantic basin demand.

Terminal throughput remained sluggish, with limited fresh fixtures curbing export momentum despite steady miner output. On the demand front, the Netherlands (0.15 mnt) and India (0.14 mnt) registered modest offtake, while elevated freight and bunker costs continued to erode price competitiveness and restrict additional bookings.

South Africa’s coal shipments fell 6.3% w-o-w to 1.20 mnt in Week 41 from 1.28 mnt in Week 40, weighed down by subdued fixture activity and persistent logistical bottlenecks at Richards Bay Coal Terminal (RBCT), which handled the entire export volume.

India remained the principal destination, taking in around 0.62 mnt, though elevated landed costs and cautious buying limited further offtake. Market participants noted that recurring rail congestion, slower vessel turnaround, and weaker freight levels prompted charterers to defer new fixtures, keeping overall export momentum subdued despite steady miner availability.

Colombia’s coal exports declined 13.8% w-o-w to 1.02 mnt in Week 41 from 1.18 mnt in Week 40, primarily due to slower port operations and reduced fixture activity. Puerto Nuevo (0.71 mnt) and Puerto Bolivar (0.24 mnt) accounted for most shipments, while Prodeco Group (0.73 mnt) and Cerrejón Mines (0.24 mnt) led loadings during the week.

Despite stable miner output, weaker Atlantic basin demand and subdued European procurement continued to weigh on overall volumes. Market participants noted that elevated freight costs and limited arbitrage opportunities dampened buying interest, resulting in a cautious export environment.

Canada’s coal exports dropped sharply by 29.1% w-o-w to 0.68 mnt in Week 41 from 0.96 mnt in Week 40, as weaker vessel arrivals and sluggish rail movement to west coast ports constrained overall throughput. Roberts Bank (0.32 mnt), Vancouver (0.23 mnt), and Prince Rupert (0.13 mnt) all recorded reduced loadings amid logistical disruptions and port congestion that delayed cargo flow.

On the demand side, China (0.28 mnt) and Indonesia (0.17 mnt) remained the primary buyers, though overall sentiment stayed muted. Exporters pointed to elevated bunker costs and subdued freight market conditions as additional headwinds limiting shipment recovery.

Dry bulk coal freight rates displayed a mixed trend in Week 41, with Indonesia-India and South Africa-India routes witnessing further softness due to weak fixture activity and oversupply of tonnage, while Australia-India rates gained marginally on post-holiday buying interest from Indian steelmakers.

The divergent trend in freight markets influenced cargo movement across key routes-softer freight on South African and Indonesian lanes failed to spur additional loadings amid subdued demand, whereas costlier Australia-India voyages, coupled with rising bunker prices, kept exporters cautious. Overall sentiment stayed fragile, constrained by limited new cargoes, selective chartering, and increasing voyage costs.

Outlook

Near-term coal export momentum is expected to remain moderate, with US and Canadian shipments likely to stay under pressure amid logistical challenges and soft Atlantic demand. Australian exports may stabilise further, supported by steady port throughput and returning buyer activity, while Indonesia’s volumes could hold firm as vessel scheduling normalises.

However, freight volatility and rising bunker costs pose downside risks, particularly for South African and Indonesian flows, where thin trading and weak charterer appetite may continue to restrain loadings.

Leave a Reply