- Exports surge by 40% in H1FY’26, EU’s intake rises 69%

- CBAM concerns bring forward EU demand for Indian steel

- Exports to UAE surge as Indian mills resume offering HRCs

Morning Brief: India’s steel exports (including stainless steel) climbed up by 24% m-o-m to 1.07 million tonnes (mnt) in September 2025, the highest volume recorded since March 2024. In the past 18 months, this is the first time that exports have crossed the 1-mnt mark.

Additionally, volumes have almost doubled y-o-y.

Shipments from India have accelerated in the past two months, primarily due to active restocking in the EU following concerns about additional tax burdens and higher procurement costs due to the Carbon Border Adjustment Mechanism (CBAM).

Commodity-wise break-up

Finished flat carbon steel exports increased by 24% m-o-m to 0.86 mnt, with about hot-rolled coils (HRCs) comprising almost half of the volume at 0.41 mnt, up 50%. Other flat products witnessed growth, though by more modest percentages.

Semi-finished exports more than doubled to 0.09 mnt, while finished longs were down by 15% at 0.06 mnt.

Stainless steel exports were more or less stable at 0.06 mnt.

Country-wise scenario

Exports to the EU, the leading destination, increased by 12% m-o-m to 0.6 mnt. The UAE took the second spot among top importers, tripling its intake to over 0.1 mnt. The UK received the third-highest volumes, at 0.05 mnt. Shipments to Nepal slid by a sharp 42% to 0.04 mnt, and while Vietnam sourced only 0.03 mnt, this marks a manifold surge from August.

Why did Indian steel exports rise in Sep’25?

HRC exports to EU surge: Indian HRC exports to the EU rose sharply as buyers stocked up aggressively due to uncertainty over new trade policies, including reduced quotas and CBAM. Indian mills also ramped up exports to utilise their quotas before new safeguard measures and CBAM regulations took effect.

HRC exports to Vietnam resume: An Indian mill has resumed HRC offers to Vietnam after a prolonged pause, with a deal of approximately 30,000 t heard concluded. This followed signs of a demand recovery in the country. This rebound was largely driven by rising domestic consumption and substantial government-led infrastructure and construction projects.

HRC exports to Middle East rise: Rising Chinese tags in July-August prompted Indian mills to resume HRC export offers to the Middle East after several months of inactivity. Following this, although trading remained largely muted, sporadic deals were likely concluded. For example, in mid-August, around 25,000 t were procured by a UAE-based tube-maker and re-roller for September shipment.

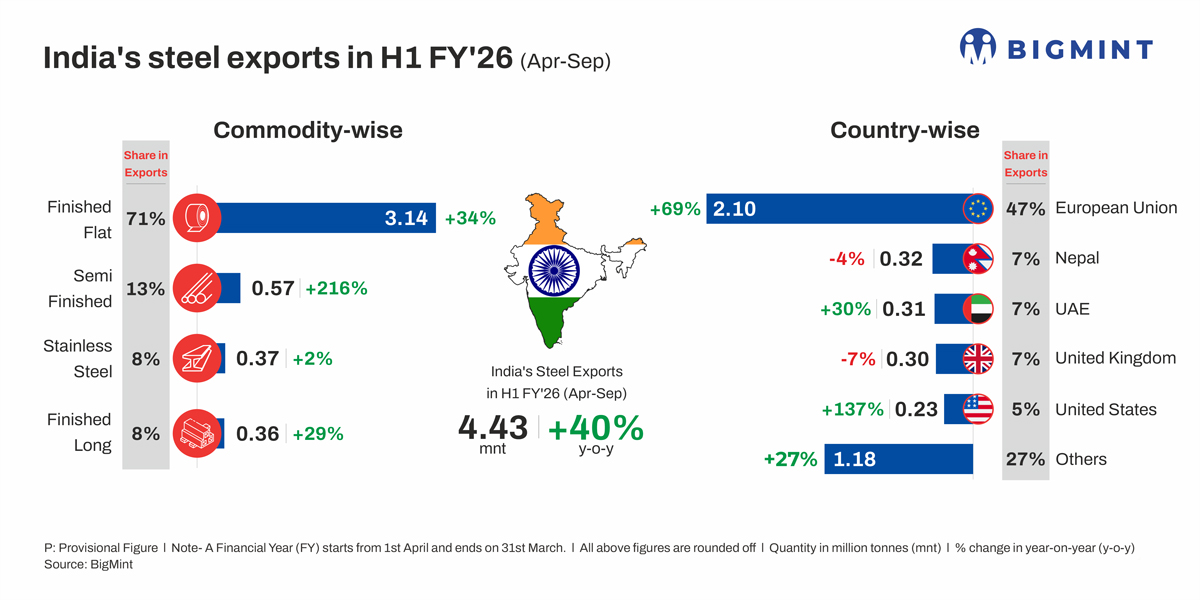

Robust export momentum emerges in H1FY’26

Meanwhile, in H1FY’26, Indian steel exports totalled 4.43 mnt, rising by a robust 40% y-o-y. Monthly volumes averaged around 0.6 mnt in April-July, higher than H1FY’25’s 0.5 mnt, before sharp surges in August and September.

Exports of HRCs increased by 56% y-o-y to 1.12 mnt, with pipes and tubes closely following with 0.96 mnt. Galvanised steel exports increased by 3% to 0.6 mnt, while cold-rolled coil (CRCs) were up 83% to 0.4 mnt.

Semi-finished exports increased by a massive 216% to 0.57 mnt, and finished steel climbed up by 29% to 0.36 mnt on the back of a 48% increase in wire rod shipments.

Again, exports to the EU drove up the total, with a substantial 69% rise to 2.1 mnt. Intake by the “Others” category, a miscellany of minor destinations, jumped by 45%, seemingly as Indian exporters looked beyond traditional markets for offloading material.

Outlook

Overall, while India’s exports have increased in recent months and H1FY’26, a big question marks hangs over the sustainability of this trend and future growth in volumes. Policy changes in the EU remain the primary factors.

To illustrate, there is already uncertainty over the continued competitiveness of Indian exports following the CBAM, and it is heard that buyers were unwilling to close deals for October shipment due to concerns over tax liabilities.

Another hurdle is the EU’s proposed slashing of tariff-free import quotas by a steep 47% and a 50% out-of-quota ad valorem duty. While this may bring forward demand, most buyers remain cautious, as per the latest assessments.

Leave a Reply