- FFAs decline as market confidence weakens

- Activity limited as most participants remain on the sidelines

Dry bulk iron ore freight markets continued to face another round of uncertainty across major routes – India-China, Australia-China, South Africa-China, and Brazil-China. Except for the Brazil-China route, all others posted gains this week; however, the increase was largely sentiment-driven rather than demand-based.

A handful of fixtures concluded at higher levels early in the week, particularly on the Australia-China route, temporarily lifted market averages. Limited follow-up activity and muted cargo demand from key miners, however, kept overall sentiment cautious. Market participants noted that the upward movement may be short-lived unless stronger cargo volumes and fresh chartering activity emerge to sustain the momentum.

The Capesize market saw a mixed week, marked by early strength followed by a loss of momentum as sentiment turned cautious. Robust activity in the Pacific, driven by steady miner demand, supported early gains, with rates on the Australia-China route climbing beyond $12/DMT. In contrast, the Brazil and South Africa to China routes struggled to find traction amid limited inquiries and subdued fixture activity, reflecting sluggish demand.

While underlying fundamentals remained firm, market sentiment was dented by escalating geopolitical tensions after China imposed new port fees on U.S.-linked vessels in retaliation for similar U.S. actions. However, industry participants noted that the Chinese Ministry of Transport’s subsequent move to exempt Chinese-built ships from these fees could help ease concerns and restore some confidence. The announcement also triggered a sharp sell-off in freight derivatives (FFAs), leading to a notable fall in FFA values later in the week.

From an India-China perspective, the Supramax segment witnessed a subdued tone through the week, weighed down by limited fresh cargoes and excess prompt tonnage across the region. With widespread holidays in Asia dampening trading activity, market sentiment remained soft and fixtures were very few.

“The Supramax market remains firm and is showing signs of gradual improvement. However, activity in India-China route has been relatively subdued ahead of the Diwali holidays, as many market participants prefer to stay on the sidelines. Only those with prompt cargo requirements are actively seeking to conclude fixtures before the holiday period”, mentioned a source to BigMint.

Another major source said, “The market currently reflects a clear disconnect between vessel owners and charterers, with owners quoting higher rates while traders are targeting levels $1-2 lower. The softening in iron ore prices since yesterday, coupled with renewed U.S.-China tensions, has further weighed on sentiment. Additionally, iron ore demand from overseas markets, particularly China, appears lackluster, adding to the overall cautious tone in the freight market.”

While throwing some light on current vessel preferences, a charterer said, “Iron ore shipments are increasingly favoring Panamax vessels over Supramaxes due to lower repositioning costs and better economics. Supramax flows to East Coast India have slowed, making Panamaxes more attractive, with ECI-North China freight rates comparatively cheaper than Supramax.”

Route-wise updates

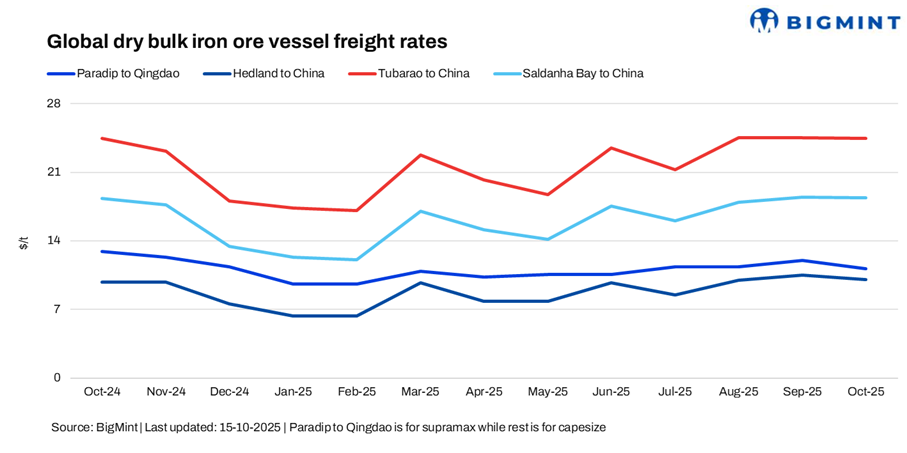

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China witnessed a w-o-w increase of $0.04/dry metric tonne (dmt) to $11.05/dmt.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China rose by $0.88/dmt w-o-w to $10.28/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments witnessed a marginal drop of $0.04/dmt w-o-w, settling at $23.82/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao edged higher by $0.06/dmt w-o-w, settling at $18.05/dmt.

Market highlights

- Baltic Capesize index rises w-o-w, Supramax yet to recover: The Baltic Exchange’s main dry bulk sea freight index increased w-o-w on 14 October 2025, driven by a recovery in Capesize rates. The overall index increased around 75 points w-o-w to 2,022, with the Capesize index rising sharply by around 122 points w-o-w to 3,007. Meanwhile, the Supramax segment continue to head south by 17 points w-o-w to 1,408.

- DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract decreased by around RMB 4/t ($1/t) to RMB 776.5/t ($108.7/t) on 15 October 2025. DCE iron ore futures fell this week as profit-taking, rising steel inventories in China, and expectations of increased ore supply pressured prices, with the January contract hitting a one-month low.

- Brent crude oil futures fall w-o-w: Brent crude oil futures dropped by around $2.86/barrel (bbl) w-o-w to $62.08/bbl. Brent crude futures fell this week to five-month lows on concerns of a global supply surplus and slowing demand amid U.S.-China trade tensions.

Outlook

The global dry bulk market faces headwinds from softening demand and increasing vessel deliveries, which have pressured freight rates, particularly for Capesize vessels.

Leave a Reply