- Cathode imports dry up, down 7% y-o-y in Q2FY’26

- Scrap imports up 35% y-o-y in Jan-Sep’25

- Scrap supply tightening, US restrictions pose threats

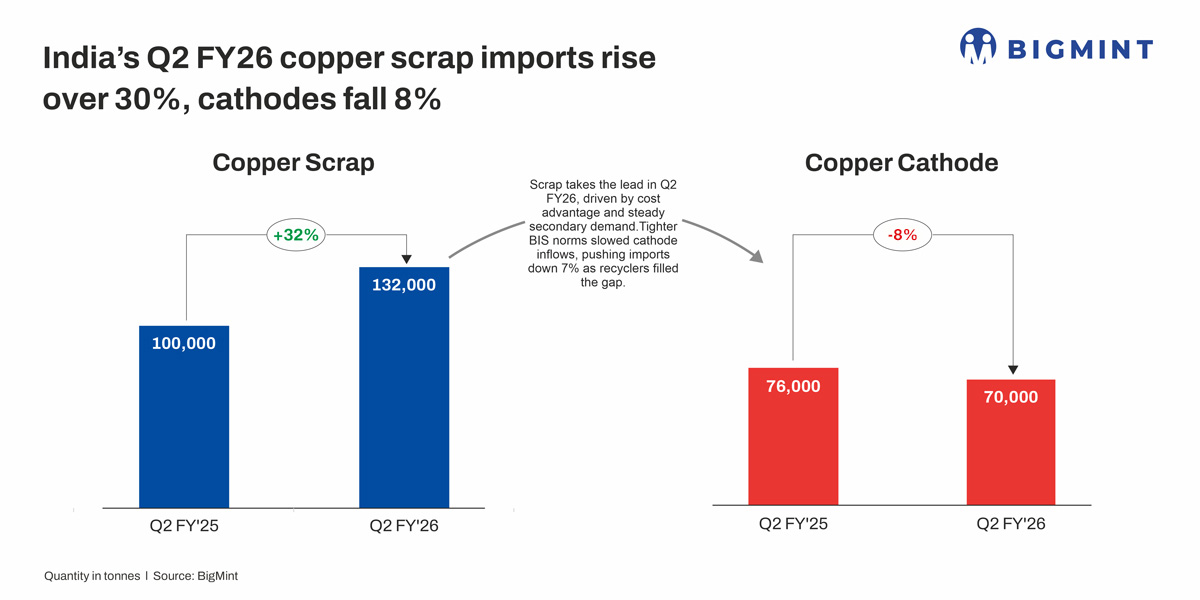

Morning Brief: India’s copper scrap imports surged by 33% y-o-y in Q2FY’26 (July-September 2025), reflecting strong buying interest amid persistent domestic supply gaps and competitive import prices. Total inflows of imported scrap reached 132,191 tonnes (t) during Q2, up from 99,575 t in the same period last fiscal, according to BigMint data.

The increase in copper scrap imports builds on sustained momentum from Q1 in which imports stood at 107,572 t, taking the cumulative H1FY’26 imports to nearly 240,000 t, compared with around 180,000 t in H1FY’25. This surge underscores the domestic industry’s reliance on imported secondary feedstock as copper smelters and recyclers ramp up operations.

Notably, copper scrap imports rose by 35% y-o-y to 317,733 t during the first nine months of 2025 (January-September), compared with 234,530 t a year earlier.

In contrast, copper cathode imports fell by 7% y-o-y in Q2, declining to 70,135 t from 75,795 t in Q2FY’25.

In July-September, the average LME copper price was around $9,963/t (3-month contract) compared to roughly $9,384/t in July-September 2024, indicating a y-o-y gain of 6.2%.

Why is scrap gaining preference over cathode?

For many downstream industries, especially cable and wire producers, scrap offers cost advantages over primary cathodes. The global copper scrap market has been supplying higher volumes at steady prices, boosted by exports from the US and Saudi Arabia.

India faces challenges in domestic scrap availability and quality. A significant proportion of domestic scrap is mixed, contaminated, or alloyed, unsuited for high-grade metallurgy. Hence imports of cleaner, high-quality copper scrap like bare bright and clean scrap are preferred by refiners to maintain product quality.

Leading Indian smelters and recyclers are increasingly investing in flexible secondary metal processing routes. This shift allows them to optimise cost while managing feedstock variability. Growing capacities of Indian recyclers encourage stable scrap sourcing over cathode dependence.

Increased scrap imports reduce reliance on cathode imports, which are more sensitive to regulatory changes and global political risks (such as the US 50% tariff on Indian copper).

How are global factors influencing India’s imports?

India’s copper scrap imports from the US surged by 177% in H1 FY’26 at 57,257 t and 256% y-o-y in Q2, reaching 38,465 t, largely reflecting pre-tariff shipments rushed before the US imposed a 50% export duty on metal scrap in early August. Since most cargoes arriving in August-September were booked in advance, the impact of the duty may emerge in the next quarter.

The 50% US tariff on Chinese copper products indirectly benefited India. With reduced Chinese demand and slower domestic offtake, US recyclers faced surplus scrap, prompting a sharp rise in exports to India. Indian secondary smelters, offering competitive prices and no import tariffs, became key buyers.

Germany’s copper scrap exports to India fell by 12.6% y-o-y in Q2 because of tight domestic scrap availability and stronger European demand. With refined copper prices staying elevated, several German recyclers opted to retain high-grade material for local processing instead of exports. Additionally, higher energy and logistics costs in Europe further reduced the competitiveness of German cargoes in Indian markets.

What is supporting higher scrap imports?

Growing domestic supply gaps have propelled scrap demand. India’s own recycling capacity and secondary production remain underutilised, and mines offer modest output. As smelters and recyclers expand aggressively, they depend on imported scrap to keep operations running and to respond to surging demand from infrastructure and manufacturing.

In contrast, copper cathode imports have shrunk. New quality control regulations require stringent BIS certification and documentation for cathode shipments, raising compliance costs and causing supply chain delays. Foreign suppliers, especially from Japan, Tanzania, and Mozambique, face more hurdles, making cathodes less attractive and less accessible. Indian buyers are increasingly turning to scrap as a reliable, low-cost alternative amid regulatory bottlenecks.

Brass honey imports up in H1, steady trend in Q2 FY’26

Brass Honey imports to India were up 7% y-o-y in H1 FY’26 at 69,000 t against overall imports of 240,000 t and held almost flat at 34,086 t in Q2 FY’26, a fall of just 2.1% y-o-y despite gains in other scrap grades. This resilience is particularly visible in Jamnagar’s brass hubs, where demand for Honey remains consistent to feed the thousands of small workshops that produce fittings, fasteners, and hardware. Jamnagar, which hosts over 5,000 large and 10,000 small brass workshops, continues to absorb stable volumes even when imported supplies are jittery.

Outlook

India’s copper demand is set to nearly double to 3-3.3 mnt by 2030, while domestic scrap generation will stay limited at 430,000-530,000 t, keeping import dependence high. With supply risks in Chile, Peru, and Indonesia, scrap’s role will strengthen further. Refiners are expanding local capacity, led by Adani’s Kutch project and Hindustan Copper’s mine plans.

Scrap imports will stay firm through FY’26, aided by policy support and strong demand, while cathode inflows remain constrained by QCO rules and high prices. India’s secondary copper market is expected to maintain strong import momentum through FY’26, supported by healthy domestic demand, expanding recycling capacity, and cost advantages over cathodes.

However, global scrap supply tightening, higher freight rates, and upcoming US export restrictions may keep importers cautious in the coming months.

Leave a Reply