- Southeast Asian buyers inactive; wide bid-offer gap slows trade

- Russian tags dip on soft demand; stronger rouble squeezes margins

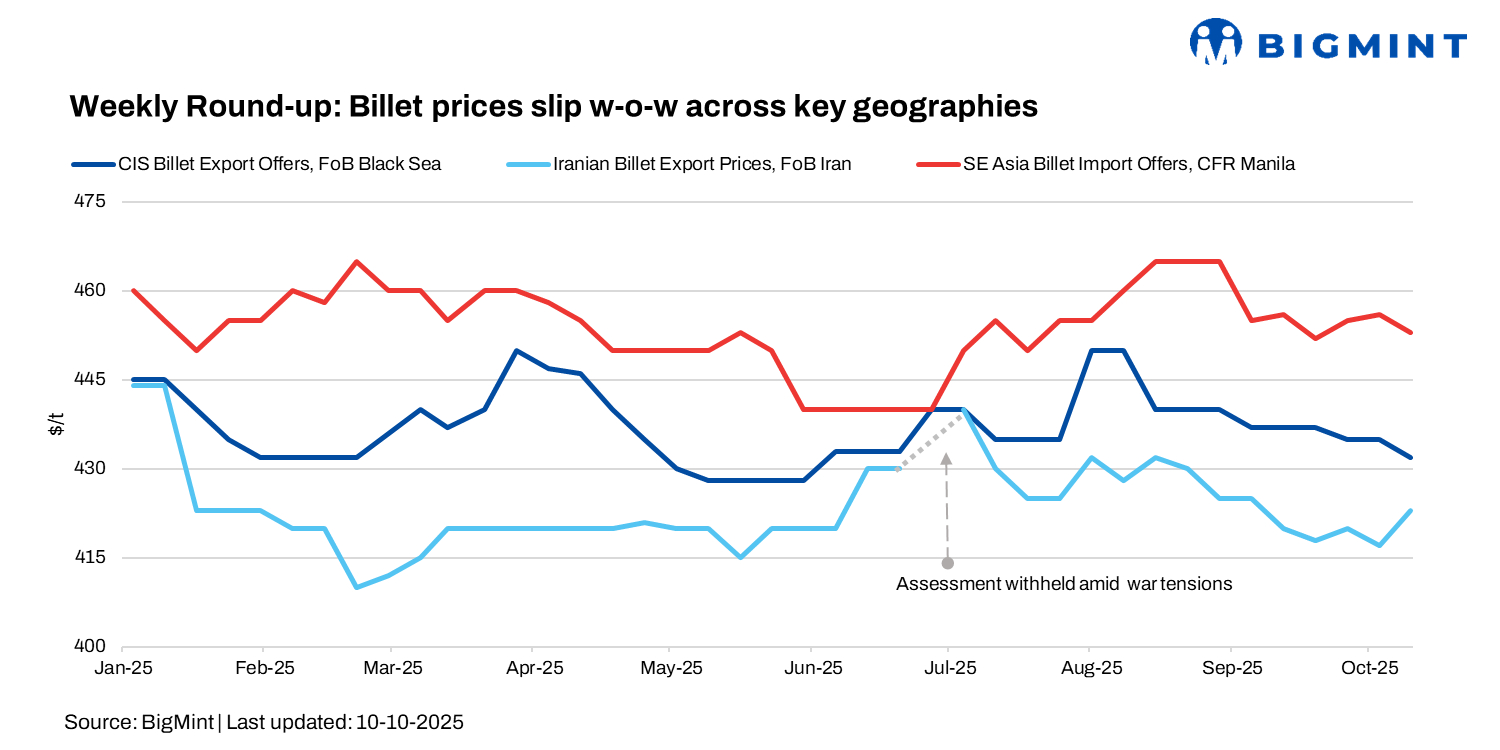

In week 41 of 2025, global billet prices extended their downward trend w-o-w, except in Iran, where prices inched higher. CIS billet values fell further amid weak Turkish buying and minimal North African demand, despite firmer scrap tags. In Asia, billet export prices remained unchanged from pre-holiday levels, with most buyers inactive and a wide gap between bids and offers in Southeast Asia.

Turkiye’s imported scrap market showed a steady upward trend, supported by firm freights and tight supply. US/Baltic-origin HMS 80:20 offers rose from $346-350/t CFR early in the week to around $350-352/t CFR by the weekend, as sellers held back cargoes amid higher costs. While domestic sales remained under pressure, optimism resurfaced following Ukraine’s exemption from EU steel import tariffs, which could aid Turkish mills in boosting exports ahead.

CIS, Russia

CIS billet export prices continued to edge lower this week, pressured by weak Turkish demand and inactive North African markets despite firm scrap values. Russian billets were heard at $435-440/t FOB Black Sea for December shipment, down from above $440/t last week. Larger-volume deals with partial prepayment were reportedly achievable at $430/t FOB.

A stronger rouble further constrained exporters’ margins, limiting new December offers. In Turkiye, Russian billets were quoted at around $450/t CFR, slightly below last week’s $455/t CFR. With low trading interest and few fresh deals, indicative CIS billet export prices were revised down by $2/t to $430-432/t FOB, reflecting continued market softness and cautious sentiment.

India

As per market insiders, around 10,000 t of billet were recently sold to Africa at $455/t FOB Kandla by a major Gujarat-based steelmaker, marking one of the few recent exports from Gujarat mills. African buyers typically purchase 3sp/4sp grades. The deal is considered competitive, compared with $430/t FOB for Chinese billets and Indonesia’s Dexin at $435/t FOB.

Historically, Gujarat-based mills were active exporters to East Africa from 2020 to 2022. Since then, shipments have declined, limited mainly to small lots to Sri Lanka.

Southeast Asia

Asian export billet prices were largely unchanged this week as end-users remained inactive, waiting for lower levels. Chinese 3sp billet offers stood at $430-435/t FOB, while buyers bid around $425/t FOB. Dexin Steel’s Indonesian base-grade billet remained stable at $435/t FOB for December, with slab offers at $455/t FOB.

In Southeast Asia, 5sp billet offers were at $455-460/t, and 3sp levels were at $450-452/t CFR, with bids at $440-445/t CFR. Some interest came from Thailand, but no deals were heard. Outside the region, Chinese billets were offered at $465/t CFR Saudi Arabia, with buyers bidding $450-455/t CFR.

China

In Tangshan, China, billet prices inched up RMB 20/t ($3/t) w-o-w to RMB 2,970/t ($417/t) on 10 October from RMB 2,950/t ($414/t) on 30 September. SHFE (January 2026) rebar rose RMB 31/t ($5/t) w-o-w to RMB 3,103/t ($436/t) over the same period.

Despite this marginal recovery post-Golden Week holidays, the market remains subdued due to weak domestic demand, high inventories, and limited export activity. Mills reduced output to manage supply pressure, while exporters offered $5/t lower prices to attract overseas buyers amid northern port congestion.

Iran

Iranian export billets stood at $422-425/t FOB, with a major steel company selling three cargoes totalling 90,000 t for mid-December delivery, likely from Khouzestan Steel Co. at $425/t FOB basis.

Slab prices remained unchanged at $410/t FOB, while rebars held at $390-400/t exw.

Recent exchange rate increases have reduced rebar prices, prompting speculators to exploit the gap between free-market and preferential (subsidised) rates using rented commercial cards.

Saudi Arabia

The Saudi billet market remained largely stable despite high scrap costs and weak downstream demand. Domestic billets were offered at SAR 1,780-1,800/t ($474-480/t) exw, slightly down from last week. Rolling margins remained under pressure as rebar prices failed to cover production costs.

A 50,000-t Chinese billet deal was reportedly concluded at $455-457/t CFR, with offers heard at $462-465/t CFR; buyers targeted $450-455/t CFR.

Domestic HMS (80:20) was at SAR 1,415/t ($377/t), citing tight supply and unchanged benchmark mill prices. Market activity is limited, and both billet and scrap prices are expected to remain range-bound until fresh import offers and clearer rebar demand emerge.

Leave a Reply