- Mixed economic data tempers price gains

- Global supply deficit nears one million tonnes

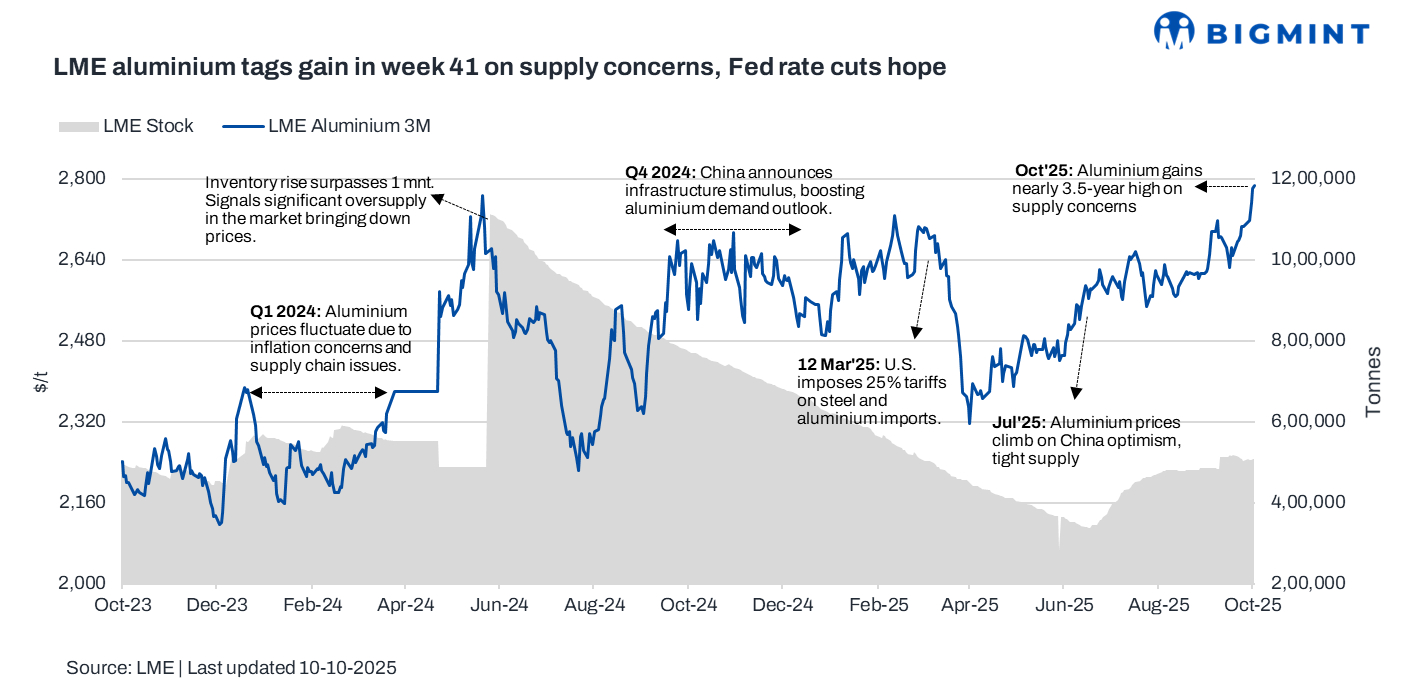

London Metal Exchange (LME) aluminium prices rose to nearly a 3.5-year high during week 41 of CY’25 (6-10 October 2025).

The price rise was primarily driven by renewed optimism in global commodity markets following the U.S. Federal Reserve’s 50-basis-point rate cut. The rate cut boosted investor sentiment and lifted overall commodity prices, including base metals.

Pricing, inventory trends

LME aluminium prices averaged $2,751/t in week 41, marking a $65/t or 2.5% increase w-o-w from week 40 (29 September-3 October). The week began with prices at $2,716/t, climbing steadily to around $2,750/t mid-week, briefly touching $2,800/t, and closing strong at $2,787/t.

Supporting the price rally, LME aluminium inventories declined by 1%, falling to 507,290 t in week 41 from 512,219 t the previous week, indicating tightening supply conditions.

Rate cut impacts on aluminium pricing

The U.S. Federal Reserve, after a 25 bps rate cut last month, is expected to ease further at its 28-29 October and December meetings. Fed Governor Christopher Waller expressed support for rate cuts but stressed caution amid mixed economic signals. His comments came as reports named him a finalist to succeed Jerome Powell as Fed Chair in 2026.

Expectations of continued monetary easing, along with a weakening dollar, have boosted investor sentiment across commodities, contributing to a rise in global aluminium prices as lower rates typically enhance demand and reduce holding costs for industrial metals.

Market updates

Support for aluminium prices continues to build amid tightening global supply conditions. Notably, China has reached its annual aluminium production cap of 45 mnt), reinforcing expectations of constrained global output. On the inventory side, LME aluminium stocks have dropped by 50% from their June 2024 peak, while SHFE inventories are down approximately 53%, highlighting persistent supply-side pressure.

Trade flows further underscore this trend. China’s aluminium imports surged 40% y-o-y to 317,549 t in 2025, driven by higher inflows from Russia, Indonesia, and India.

However, it is important to acknowledge the mixed macroeconomic backdrop. While supply dynamics remain tight, China’s industrial production growth slowed to 5.2%, and fixed asset investment increased by just 0.5% y-o-y, pointing to underlying softness in domestic economic momentum.

From a global perspective, the World Bureau of Metal Statistics reported a supply deficit of 985,300 t for the January-July 2025 period, reinforcing the broader structural tightness in the aluminium market.

Outlook

Looking ahead, market sentiment remains cautiously optimistic, a mix of mixed global fundamentals and macroeconomic challenges may cap further gains, likely keeping aluminium prices range-bound in the near term. However, anticipated U.S. rate cuts, a softer dollar, and tightening inventories are expected to provide solid support, sustaining price stability and preventing significant declines.

Leave a Reply