- Vedanta plans INR 13,226 crore aluminium expansion

- Global refined copper output forecast to grow 3%

At close of trading on 10 October 2025, base metals prices on the London Metal Exchange (LME) showed divergent trends w-o-w, with copper witnessing the highest decline of 1.85% to $10,518/tonne (t). Meanwhile, LME warehouse stocks exhibited negative trends, with zinc witnessing the steepest decline of 4.65%.

On the LME, three-month aluminium prices stood at $2,748/t, up by 1.40% w-o-w, while zinc decreased by 1.09% to $3,002/t. Copper prices were at $10,518/t, down by 1.85% w-o-w, and lead was up by 0.05% at $2,021/t. Nickel stood at $15,280/t, down by 0.99% w-o-w.

LME aluminium prices surged to a 3.5-year high of $2,790/t, last seen in June 2022, driven by tightening supply and falling inventories. On-warrant stocks dropped 15% in a month to 398,775 t, highlighting strong demand. Adding pressure, Guinea revoked all mining licences from Guinea Alumina, raising concerns over bauxite supply disruptions to major producers like Emirates Global Aluminium, further fuelling market uncertainty.

The benchmark three-month copper contract on the London Metal Exchange (LME) closed at $10,700/t on 4 October, marking a gain of $400 from 26 September. The move reflects a confluence of bullish forces tightening supply, falling inventories, steady demand, and supportive currency trends.

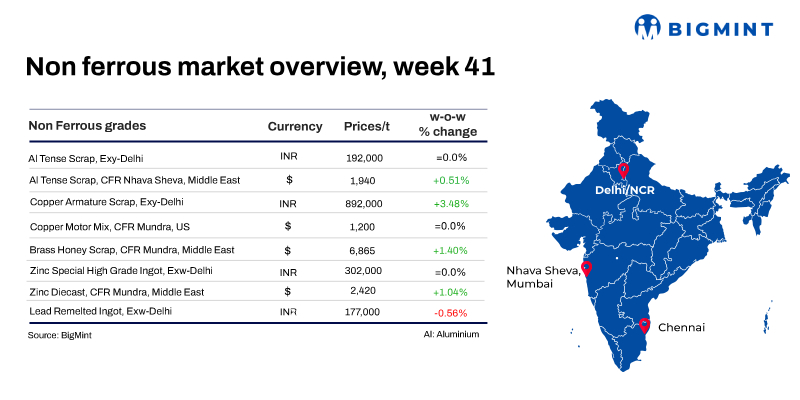

India’s imported aluminium scrap prices saw an increase of $20-30/t w-o-w, following a positive trend on London Metal Exchange (LME) benchmarks.

BigMint assessed Tense scrap from the US at $1,995/t, up by $20/t w-o-w, while US Taint Tabor HRB (2-3%) was up $25/t at $2,250/t.

India’s bauxite imports fell 24% y-o-y in the first seven months of calendar year 2025 (7MCY’25) to 2.13 million tonnes (mnt) from 2.81 mnt in 7MCY’24. In contrast, alumina imports rose 18% y-o-y to 1.43 mnt in 7MCY’25, suggesting that producers increasingly relied on imported value-added material to bridge quality gaps or offset limitations in domestic bauxite supply.

India’s aluminium ADC12 alloy ingot prices saw a slight m-o-m increase in October 2025 primarily due to the positive auto demand post the cuts in GST.

BigMint’s monthly assessment for OEM-grade ADC12 showed firm pricing across key regions, with Delhi at INR 230,000/t, up by INR 1,500/t m-o-m; Pune at INR 230,000/t, reflecting a m-o-m increase of INR 2,000/t; and Chennai at INR 231,000/t, up by INR 500/t m-o-m. These prices are based on 30-day payment terms.

Imported copper scrap prices in India saw an uptrend w-o-w, following a gain in London Metal Exchange (LME) copper futures, which hit a 16-month high and remained high levels currently and remained at around $10,260/t. Parallelly, domestic copper scrap prices increased w-o-w.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $9,900/tonne (t), up by $5/t w-o-w, while US motors mix stood at $1,200/t (both CFR Mundra), remained stable w-o-w.

India’s copper pipe and tube imports fell 10% y-o-y to 39,900 tonnes (t) in the first five months of FY26 (April-August 2025), compared with 44,500 t in the same period last year. Shipments from Vietnam plunged by 25% y-o-y to 21,100 t (53% of total imports) from 28,100 t (63%) in the previous year.

India’s zinc scrap and dross market witnessed an upward movement this week, supported by sustained demand from local processors and steady inquiry levels.

BigMint assessed zinc diecast scrap (Middle East origin) at $2,425/tonne (t) CFR west coast India, up by $30/t w-o-w, reflecting firm buying interest from secondary producers.

Hindustan Zinc Limited (HZL), the worlds largest integrated zinc producer, announced strong operational performance for the second quarter and first half of FY26, with record mined metal production.

In Q2 FY26, HZL achieved its best-ever second-quarter mined metal production at 258,000 t, up 1% year-on-year.

Domestic zinc spot prices remained stable at INR 302,000/t exw-Delhi w-o-w. HZL zinc prices were up by 2.4% w-o-w to INR 317,600/t ex-Chanderiya.

Lead

The lead market experienced a week of mixed signals and slight volatility.

Domestic primary lead ingot prices stood at INR 195,000/t, down by INR 3,000/t w-o-w, while re-melted ingots stood at INR 177,000/t, down by INR 1,000/t w-o-w.

Meanwhile, HZL lead prices were up by INR 1,100/t w-o-w to INR 208,700/t ex-Chanderiya.

Other updates

Vedanta to invest INR 13,226 crore to boost aluminium capacity

Vedanta Ltd. plans to invest INR 13,226 crore to expand its aluminium production capacity from 2.4 MTPA to 3.1 MTPA by FY’28, with an interim goal of 2.75 MTPA by FY’26. The company, which has cut aluminium production costs by nearly 24% through backward integration at its Lanjigarh refinery and captive coal operations, aims to make aluminium the largest contributor to its group-level EBITDA of $8–10 billion by FY’28. Rising domestic demand, driven by India’s infrastructure growth and energy transition, is expected to further support Vedanta’s expansion strategy.

Global refined copper output to rise 3% in 2025

The International Copper Study Group (ICSG) projects global refined copper production to grow by 3.4% in 2025, supported by capacity expansions in China, the DRC, India, and Indonesia, along with improved output from Zambia. Primary refined copper from concentrates and SX-EW is expected to rise 3%, while secondary output from scrap may increase 4.5%. However, the market is forecast to show a surplus of 178,000 tonnes in 2025 before shifting to a 150,000-tonne deficit in 2026 due to limited concentrate availability. Global mine production is set to rise 1.4% in 2025 and 2.3% in 2026, driven by ramp-ups at key projects in Mongolia, Russia, and Chile.

Leave a Reply