- Post-holiday demand supports stability in portside coal trades

- Domestic coal market muted due to SECL policy uncertainty

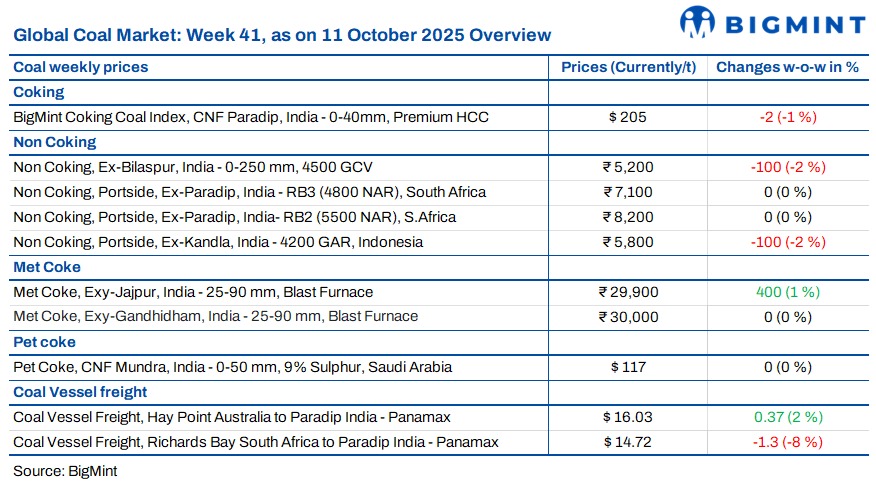

This week, the Indian coal market displayed a cautious yet stable sentiment. Indonesian and South African portside coal maintained steady levels, supported by post-holiday buying, while the domestic coal segment remained quiet due to uncertainties over the new SECL policy. Pet coke supply constraints kept US thermal coal demand firm, and coking coal sentiment was range-bound amid limited deals. Overall, selective strength emerged across certain routes and grades, but muted industrial activity and rising costs kept market participants watchful.

Indonesian portside coal prices steady amid weak demand

Indian portside prices of Indonesian thermal coal stayed largely stable in the week ending 3 October 2025, as weak demand and ample stocks kept the market balanced. 5000 GAR was assessed stable w-o-w at INR 7,100/t at Kandla and INR 7,050/t at Vizag, while 4200 GAR eased INR 100/t w-o-w to INR 5,800/t and INR 5,700/t, respectively. Power plant coal stocks fell to 44.52 mnt, raising fuel security concerns ahead of the festive season. Overall, prices are expected to stay range-bound amid subdued industrial activity.

South African thermal coal portside prices hold firm on active post-holiday trades

South African portside coal prices in India were stable this week, supported by steady demand after the holidays. RB2 was assessed at INR 8,200/t and RB3 at INR 7,100/t across Paradip, Vizag, and Gangavaram. Around 100,000 t of trades were heard, at INR 8,150-8,200/t ex-works. Portside stocks rose 3% w-o-w to 12.22 mnt amid improved arrivals and logistics. Export offers at RBCT edged up $1-2/t following a dip in freights, while RB2 was at $71/t FOB and RB3 at $60/t FOB. Market outlook remains firm for November.

Domestic coal prices steady as SECL policy keeps market subdued

India’s domestic coal market stayed quiet this week amid uncertainty over SECL’s new grade upgradation policy. Prices of 5,000 GCV coal held at INR 6,250/t ex-Bilaspur, while 4,500 GCV slipped INR 100/t to INR 5,200/t. Traders avoided fresh bookings due to delivery delays and limited lifting, leading to emerging supply concerns in the near term.

US portside thermal coal prices steady but may rise on pet coke shortage

US-origin thermal coal prices at Indian ports stayed unchanged w-o-w at INR 10,400/t. However, market sentiment turned firm as domestic pet coke supply remained tight, with Reliance and Nayara prioritising self-consumption. The shortage has prompted some end-users to consider US coal as an alternative fuel, which could lift demand and support prices in the coming weeks.

BigMint’s coking coal index steady amid limited trades, firm steel outlook

BigMint’s premium hard coking coal (PHCC) index was assessed at $205/t CNF Paradip on 10 October 2025, down $2/t w-o-w. A single deal of 75,000 t Australian-origin PHCC was booked at $203/t CFR India for end-October shipment, while bid-offer gaps limited further trades. Met coke prices in India rose on stronger steel demand and anti-dumping talks, while Chinese coke prices increased post-holidays. With Indian mills raising rebar prices and diversifying coking coal sourcing beyond Australia, near-term sentiment remains range-bound but fundamentally supported.

Met coke prices rise slightly w-o-w; western offers stay stable

India’s met coke market showed a mild upward trend in the week ending 9 October 2025. Prices in east India increased by INR 400/t w-o-w to INR 29,900/t ex-Jajpur, with a deal heard at INR 30,500/t, supported by improved post-festive steel demand and supply issues in Australia. In contrast, west India remained steady at INR 30,000/t exw-Gandhidham amid weak buying. Foundry-grade coke held firm at INR 35,600/t ex-Rajkot. Australian premium hard coking coal prices stayed at $190/t FOB. Meanwhile, pig iron prices dipped to INR 31,950/t ex-Durgapur on subdued foundry demand.

Imported pet coke prices stay firm amid tight local supply

Imported pet coke prices into India held steady this week as domestic availability remained tight. BigMint assessed US-origin material at $118-120/t CFR, with a 50,000-t cargo booked in east India at $119/t CFR. RIL continued self-consumption and imports, while reduced output from Nayara Energy further limited supply. No Saudi offers surfaced due to refinery shutdowns, keeping market sentiment firm.

Refiners raise pet coke prices again in Oct’25 amid tight supply

Indian refiners extended pet coke price hikes for October, supported by limited supply and steady cement demand. IOCL raised prices by INR 380-750/t across refineries, with Panipat at INR 14,560/t and Koyali at INR 13,480/t. BPCL increased rates at Bina and Kochi by INR 467-573/t, while MRPL and CPCL lifted offers by about INR 550/t. Nayara revised its gate prices up by INR 580/t to INR 14,870/t amid lower output. With RIL inactive and supply tight, refiners maintained pricing control as post-monsoon demand picked up.

Freight rates on South Africa-India route fall to 2-month low amid mixed market trends

Dry bulk coal freights showed mixed trends this week. Rates on the South Africa-India route dropped sharply by $1.3/t w-o-w to $14.72/t, the lowest in two months, due to weak fixtures and muted activity. Indonesia-India Supramax rates slipped by $0.22/t to $16.25/t amid sluggish demand and vessel oversupply. Meanwhile, Australia-India Panamax freights inched up by $0.37/t to $16.03/t as Indian steelmakers resumed spot buying post-Dussehra. However, rising bunker prices continued to inflate voyage costs, limiting fresh deals. Overall, market sentiment stayed cautious, with mixed movements across key trade routes.

Leave a Reply