- US scrap prices rise amid tight HMS availability

- EU tariff changes keep Turkish buyers cautious

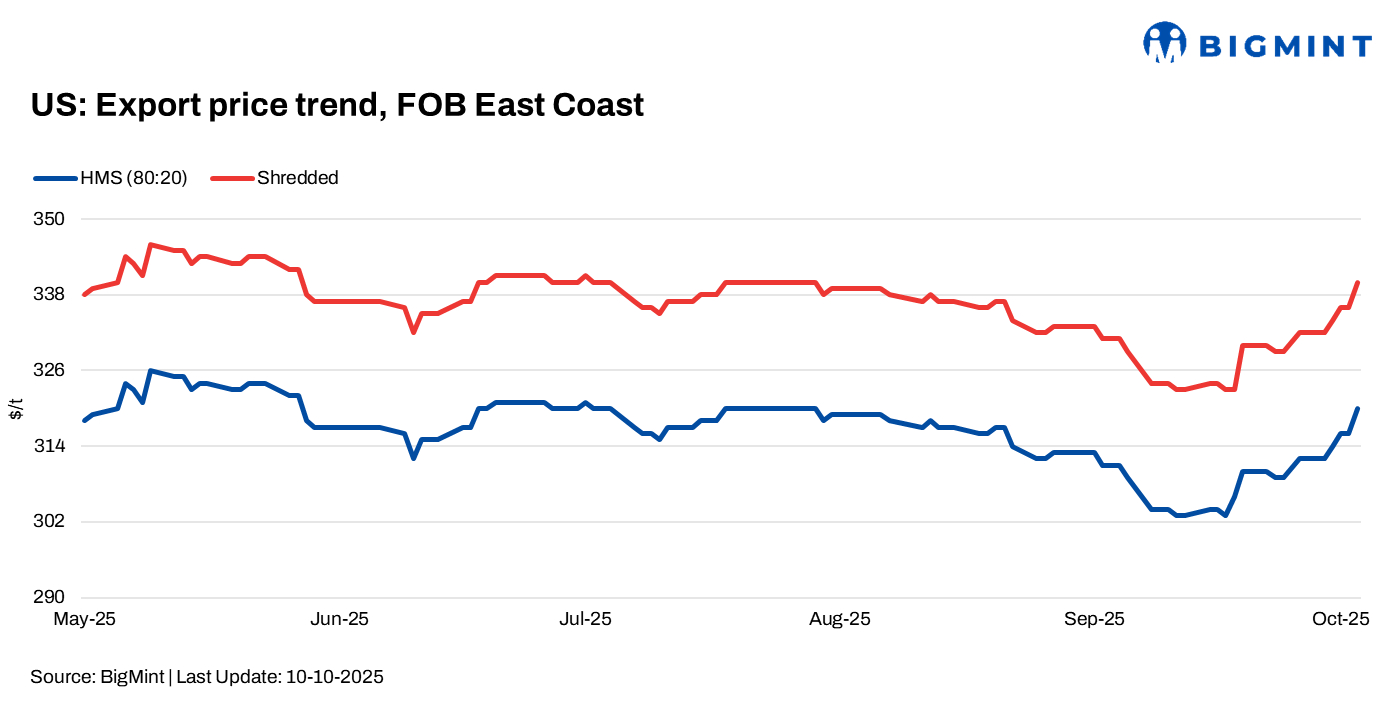

US ferrous scrap export prices rose by $8/t w-o-w, supported by tight availability of HMS along coastal markets. As per market insiders, HMS pricing remained unusually strong compared to other grades with limited supply and firm buyer interest.

Despite the price gains, demand in key markets showed caution. Turkish steelmakers paused deep-sea purchases following the European Commission’s proposal to sharply reduce steel import quotas, including a 47% cut in tariff-free volumes and a 50% ad valorem duty on excess imports. This development, combined with weak downstream steel demand, limited fresh US scrap bookings, even as coastal availability remained tight.

Mills are expected to implement short-term production cuts amid squeezed margins and constrained ability to pass through rising raw material costs.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $320/t, up $8/t w-o-w

- Shredded – $340/t, up $8/t w-o-w

Key importer

Turkiye: Demand for US-origin ferrous scrap in Turkiye stayed cautious, with prices edging up despite subdued trading. Tradable values for US and Baltic-origin cargoes were heard at $346-350/t CFR, though US sellers were offering higher at $350-355/t CFR amid rising freight concerns.

- Weak downstream steel demand weighed on fresh imports

- European tariff revisions added to market uncertainty

Bulk scrap inquiries from Bangladesh and Vietnam stayed dull, with only a handful of buyers showing interest in US cargoes. Most preferred smaller, easier-to-manage shipments from nearby markets like Singapore, Hong Kong, South Korea, Malaysia, and Japan.

US-origin HMS 80:20, bulk — CFR assessments

- Turkiye – $351/t, up $6/t w-o-w

- Vietnam – $340/t, stable w-o-w

- Bangladesh – $349/t, down $2/t w-o-w

Outlook

US scrap export prices are likely to remain supported in the near term due to tight coastal scrap availability, but demand may stay weak in markets like Bangladesh and Vietnam amid weak downstream demand.

Leave a Reply