- Kanto tender sees 20,000 t of H2 sold to Bangladeshi mill

- JPY depreciation revives some buying interest for scrap

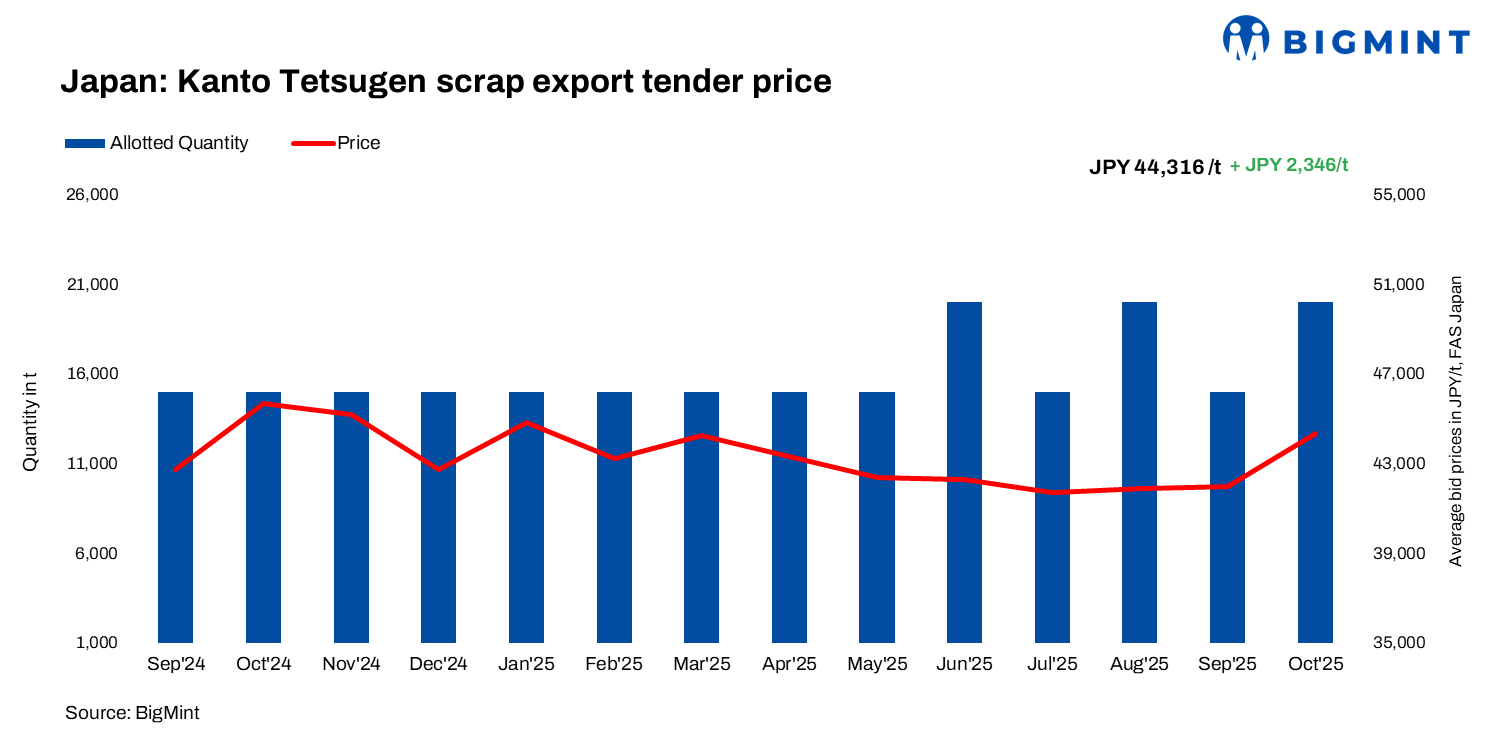

Japan’s October 2025 Kanto scrap export tender witnessed a sharp m-o-m uptick of JPY 2,346/tonne (t) ($15/t), with a 20,000-t H2 lot reportedly awarded via a Japanese trading firm to a Bangladesh, Chattogram-based mill at JPY 44,316/t ($290/t) FAS Japan. For comparison, this is an increase from Sep tender’s JPY 41,970/t ($275/t). This marks the third consecutive monthly price rise and the highest since January’s JPY 44,810/t. The 20,000 t unit is the largest since August.

As per market insiders, the upward movement was driven by a weaker JPY (from JPY 147/$ on 10 September to 153/$ on 9 October), which supported higher export offers and resulted in a dollar value increase of $15/t.

All 15 participating trading companies submitted bids, totaling 146,100 t– an increase of 200 t from September. Only the first bid was successful, with the cargo destined for Vietnam or Bangladesh and shipping by 30 November.

The usual upper limit per ship, 15,000 t, was raised to 20,000 t by member vote. Chairman Minami noted that the exchange rate was the main driver of the increase.

According to a supplier, “The price equates to approximately $300-305/t FOB Japan, with an estimated freight of $48-52/t, bringing the CFR Chattogram cost to around $350-352/t for the buyer.” Notably, the latest Kanto tender witnessed the participation of another major Chattogram-based mill, which returned to the market after a month’s gap.

Japan’s domestic and export scrap market

Last week, H2 scrap deals were estimated at JPY 42,000‑42,500/t FOB ($275-278/t) amid tight supply and currency weakness.

Current Kanto EAF scrap prices are at JPY 41,000/t ($268/t) levels, with bay prices around JPY 41,500‑42,500/t ($272-278/t), and it is anticipated that domestic prices may rise following the bid.

The next shipments are scheduled for 8,500 t in 2 to 3 weeks, followed by 15,000 t from the September contract in 3-4 weeks.

The next shipments are scheduled for 8,500 t in 2 to 3 weeks, followed by 15,000 t from the September contract in 3-4 weeks.

BigMint’s weekly assessment placed H2 at JPY 42,600/t ($279/t) FOB Tokyo Bay, a rise of JPY 700/t ($5/t) w-o-w.

As per market participants, this is the first time since January that Tokyo Steel has adjusted prices across all its plants. The move shows concerns over Japan’s fiscal outlook following Sanae Takaichi’s victory, as her pro-spending stance and criticism of the Bank of Japan’s rate hikes have raised fears of weaker fiscal discipline.

While the softer JPY has revived some buying interest, overall activity remains limited amid regional holidays. A Korean mill booked a mixed H1:H2 cargo at JPY 43,000/t CFR ($281/t), or JPY 40,500/t FOB ($265/t) after JPY 2,500/t ($16/t) freight.

Shindachi and HS offers were held at JPY 46,500-47,500/t FOB ($305-311/t), with bids at JPY 46,000-47,000/t ($301-308/t), indicating improved buyer sentiment.

Outlook: Japan’s scrap market is expected to remain cautiously active in the near term. The weaker JPY continues to support higher export offers, drawing buyers from Bangladesh and South Korea, while domestic demand may stay muted amid fiscal uncertainty under Takaichi’s leadership. Overall, activity is likely to remain selective, with pricing influenced by currency movements and tight supply. The upcoming Kanto tender, scheduled for 11 November, will be a key indicator of market direction.

Leave a Reply