- India’s bauxite imports decline amid global supply disruptions

- Regulatory delays impact Vedanta’s Sijimali bauxite project

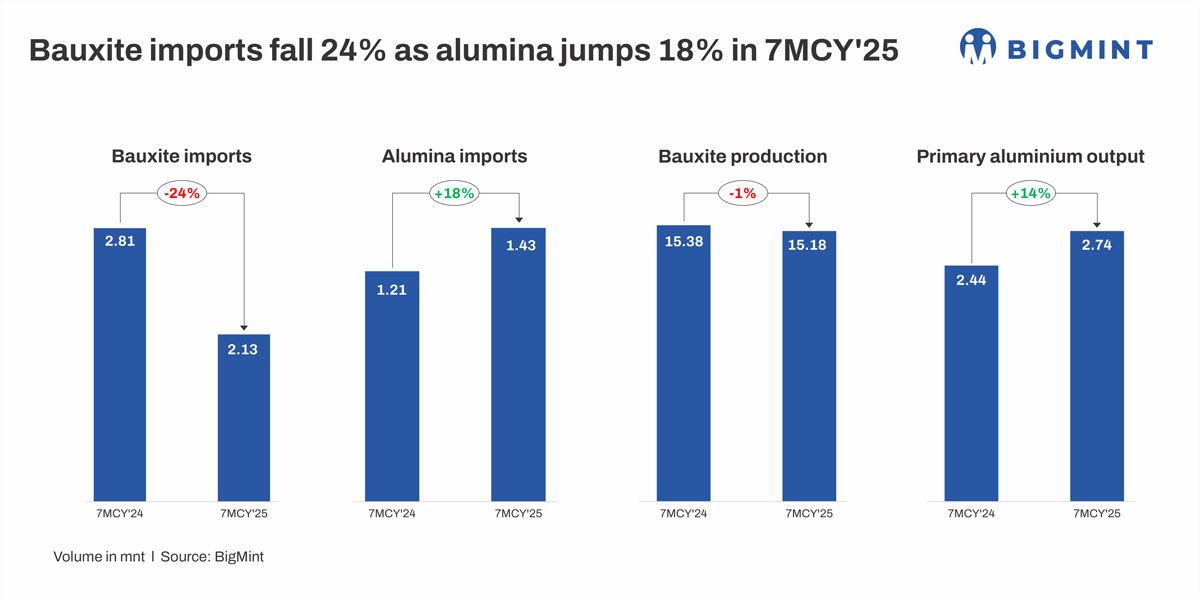

India’s bauxite imports fell 24% y-o-y in the first seven months of calendar year 2025 (7MCY’25) to 2.13 million tonnes (mnt) from 2.81 mnt in 7MCY’24. This decline comes despite a marginal 1% dip in domestic bauxite production, which stood at 15.18 mnt versus 15.38 mnt a year earlier, reflecting sustained pressure on raw material availability.

In contrast, alumina imports rose 18% y-o-y to 1.43 mnt in 7MCY’25, suggesting that producers increasingly relied on imported value-added material to bridge quality gaps or offset limitations in domestic bauxite supply. This shift has supported a 12% growth in primary aluminium output, which reached 2.74 mnt, indicating that higher reliance on alumina imports helped maintain robust aluminium production despite constrained bauxite availability.

Regulatory developments and environmental concerns continue to impact India’s aluminium sector. The MoEFCC deferred Vedanta’s Sijimali bauxite project in Odisha over ecological and local issues, with a 12-member R&R committee overseeing resettlement and social audits for the 1,549-hectare project planned to mine 9 mnt annually. Meanwhile, a private company has sought clearance to explore bauxite over 1,100 acres in Karnataka’s Honnavar forests near the Apsarakonda-Mugali marine sanctuary. Despite these constraints, India’s primary aluminium output remains strong, though regulatory delays and ecological sensitivities influence domestic bauxite availability and market dynamics.

Meanwhile, the country’s rapidly growing aluminium industry requires a steady and scalable supply of raw material, and until domestic bottlenecks in mining are resolved, imports will remain an essential part of India’s bauxite supply chain.

Bauxite production mixed across states

Regional bauxite output in India during the first seven months of CY’25 presents a mixed picture. Odisha, the leading producing state, saw a modest 2% decline, while Jharkhand and Madhya Pradesh recorded minor drops of 3% each. Maharashtra’s output fell slightly by 2%. In contrast, Chhattisgarh and Gujarat posted growth, with increases of 5% and 4% respectively, highlighting pockets of resilience. Overall, total domestic bauxite production declined 12% y-o-y to 13.57 mnt, reflecting ongoing challenges in raw material availability across several key states.

Country-wise bauxite, alumina imports

India’s bauxite imports fell 11% y-o-y in the first seven months of calendar year 2025 to 3.56 mnt from 4.02 mnt in 7MCY’24. The decline was largely driven by a 29% drop in imports from Guinea, which remained the largest supplier, falling to 1.93 mnt from 2.72 mnt a year earlier.

Guinea’s military-led government tightened mining regulations, disrupting exports from smaller operators such as SBG, GAC, and KIMBO, while Kambia Bauxite Mining remained inactive. However, major Chinese-backed mines maintained stable shipments, supported by port diversification across nine active facilities. The government’s drive to promote domestic refining over raw ore exports also triggered disputes, leading to the suspension of some mining licenses for firms that failed to meet refinery development commitments. While Guinea expanded its port infrastructure to handle increased demand, logistical challenges persisted, impacting the efficiency of bauxite shipments. These infrastructure constraints may have contributed to the reduction in export volumes.

Imports from Indonesia declined 22% to 0.61 mnt, while Vietnam’s fell 11% to 0.16 mnt. Indonesia’s 2023 export restrictions on bauxite, combined with shortened mining production quotas in 2025 and government-set pricing, created market uncertainty. These factors led to reduced export volumes as buyers hesitated to purchase at mandated prices, impacting overall shipments.

Vietnam’s bauxite exports have been limited by infrastructure and processing constraints, strict environmental regulations, and a focus on sustainable development, which slowed expansion of mining operations. Rising domestic consumption for local processing further reduced the surplus available for export, collectively restricting Vietnam’s bauxite export volumes.

In contrast, imports of alumina from China into India rose 45% to 0.16 mnt, reflecting a shift towards alternative sourcing amid constrained supplies from traditional exporters. China exported 1.57 mnt of alumina to the world, including metallurgical and other grades, during January-July 2025, up 64.3% y-o-y. In July alone, exports rose to 229,448 t, up 56.4% from last year and 34.2% m-o-m driven by firm domestic production and steady overseas demand during the same period.

India’s primary aluminium output growth continues

India’s primary aluminium output remained robust in the first seven months of calendar year 2025, rising 12% y-o-y to 2.74 mnt from 2.44 mnt in 7MCY’24, despite raw material volatility.

Vedanta led growth with a 20% increase to 1.07 mnt, Hindalco grew modestly by 5% to 0.69 mnt, while both Balco and Nalco registered 13% gains, producing 0.34 mnt and 0.27 mnt, respectively, reflecting steady performance across major Indian companies.

Outlook

India’s bauxite imports are likely to remain subdued in the remaining months of CY’25, supported by steady alumina imports and stable domestic production. While regulatory delays, environmental concerns, and logistical challenges may persist, ongoing investments and capacity expansion are expected to sustain growth in the bauxite and aluminium sectors.

Leave a Reply