-

Production affected at 20-30% of IFs, rolling mills in Raipur cluster

-

Producer margins face increased pressure on firm raw material prices

-

Output cuts may deepen in Nov on high inventories if downturn persists

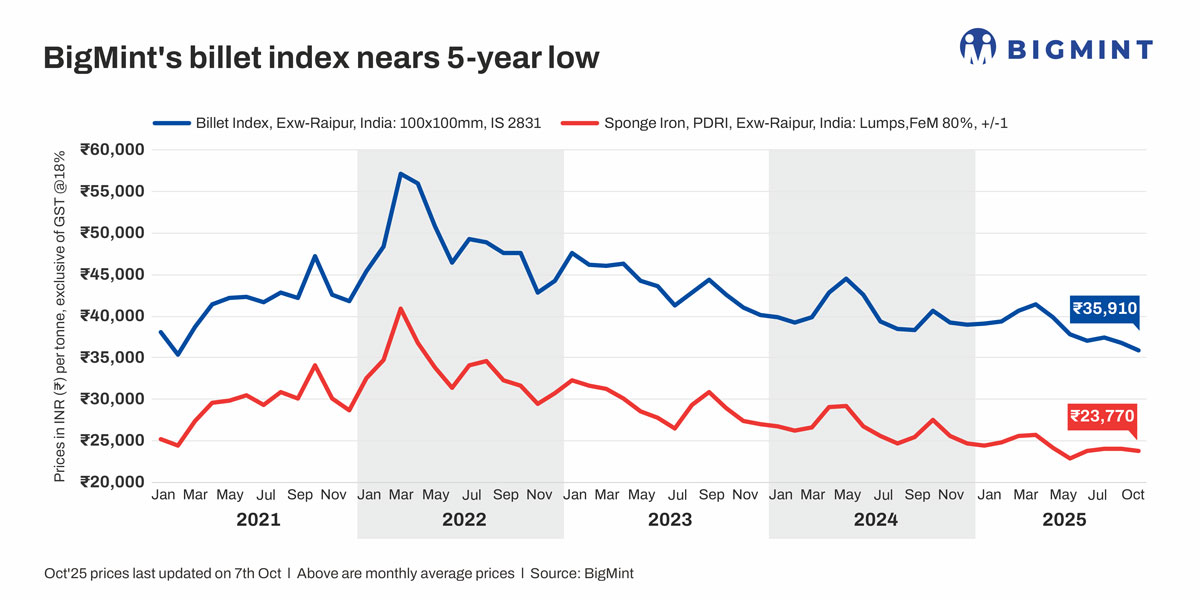

Morning Brief: India’s semi-finished steel market continued to reel under sustained pressure even in the festive month of October 2025, with BigMint’s benchmark Raipur billet (100×100 mm, IS 2831) index plunging to its lowest level in four years and eight months to a weighted average of INR 35,600/t exw-Raipur in October (till date), a low last witnessed in February 2021.

The persistent decline in the index has led to a rapid erosion of conversion margins amid rising raw material costs. With margins shrinking sharply, mill owners are facing significant financial stress. Nearly 20-30% of plants operating in the Raipur cluster, particularly the induction furnace-based producers and the rolling mills, have either halted or partially curtailed production amid mounting inventories of finished steel products, sluggish offtake, costlier raw materials, which have collectively eroded profitability.

The conversion spread from sponge iron to billet in Raipur has dropped steeply to INR 12,000-12,500/t, far below the usual margin range of INR 15,000-16,000/t required for stable operations, as per sources. The narrow spread underscores the deep financial strain across the sector, with limited room for operational flexibility.

The downtrend in the domestic billet market, however, was not a Raipur-specific phenomenon. Prices in the other major secondary steel hubs such as Durgapur in eastern India and Jalna and Mandi Gobindgarh in western and northern India dropped to multi-year lows, especially in the April-October period of the current year.

While prices in Raipur fell by 14% during April-October, average prices in Durgapur, for instance, dropped from INR 41,600/t exw in April to INR 36,350/t in October, a decline of nearly 13%.

Why did index drop to multi-year lows?

Sharp decline in finished steel prices: The precipitous drop in BigMint’s billet index, which monitors the key steelmaking hub of Raipur, owes directly to the sustained drop in finished steel prices. Semis such as billets and ingots are used to directly re-roll into finished construction steel products such as TMT bars, or rebars, as well as structural steel.

For perspective, rebar (12-25 mm Fe 500D, IF route, IS 1786) prices in Raipur dropped from INR 48,800/t exw on 1 April to around INR 42,200/t on 1 October, a decline of over 13% in seven months. Likewise, structure steel angle (40×40, IF route) prices declined from INR 46,811/t exw on 1 April to INR 41,400/t exw on 1 October, a decrease of over 11% in seven months.

Moreover, amid the market downturn, the blast furnace-based rebar producers were reportedly selling to the project segment at prices equivalent to those of IF-based producers. As the spread between BF- and IF-route rebar shrank, the IF-based producers came under further price pressure.

Sustained demand downturn: Market participants attribute the downturn in steel prices to persistent weakness in downstream demand, particularly from the construction and infrastructure sectors due the early onset of monsoon, the prolonged impact of heavy rainfall across regions and the detrimental impact on construction, logistics, mining and the entire supply chain which impacted steel prices.

Moreover, global headwinds such as prolonged demand and production slump in key geographies, weak global steel prices, tariffs and trade uncertainty, as well as the prolonged downturn in the Chinese steel sector all weigh on steel prices. Seasonal slowdown combined with reduced liquidity and subdued trade sentiment, further dampened demand. Traders and mills refrained from building inventories amid market uncertainty, further impacting spot demand.

Raw material prices: The decline in key raw material prices was another key factor for semis and finished steel prices edging down to multi-year lows during 2025. In the predominantly sponge iron-based billet market in Raipur, sponge iron (DR-CLO-based) prices declined to the lowest level since February 2021 to average INR 27,525/t exw in October compared to around INR 29,800/t in April, a decrease of around 8%. Declining raw material prices pressured billet prices.

However, the rapid erosion in producer margins was owing to the fact that steel prices edged down more sharply compared to raw materials. This was due mainly to flat domestic iron ore production amid surging demand. For example, while sponge iron in Raipur declined by 8% in the April-October period, billet prices dropped 14%. In fact, pellet (Fe63%) prices in Raipur increased marginally by 1.3% in the April-October period of 2025 from an average of around INR 10,200/t DAP Raipur in April to INR 10,300/t in October.

Outlook

With the festive season approaching, short-term recovery appears limited. Market activity is expected to remain subdued as many buyers prefer to postpone fresh procurement until after Diwali. However, any improvement in construction activity post-Diwali or restocking efforts by mills could lend some support to prices.

However, despite thin and/or negative margins, many mills in Raipur are holding greater-than-average inventories as production cuts have not been proportional to the decline in prices. If the downtrend persists in November, we are likely to see further production cuts. Therefore, the focus among producers is likely to remain on inventory control and production optimisation to minimise losses during this challenging phase for the industry.

Leave a Reply