- Policy uncertainty on export duty keeps market cautious

- NMDC’s next price revision to offer near-term direction

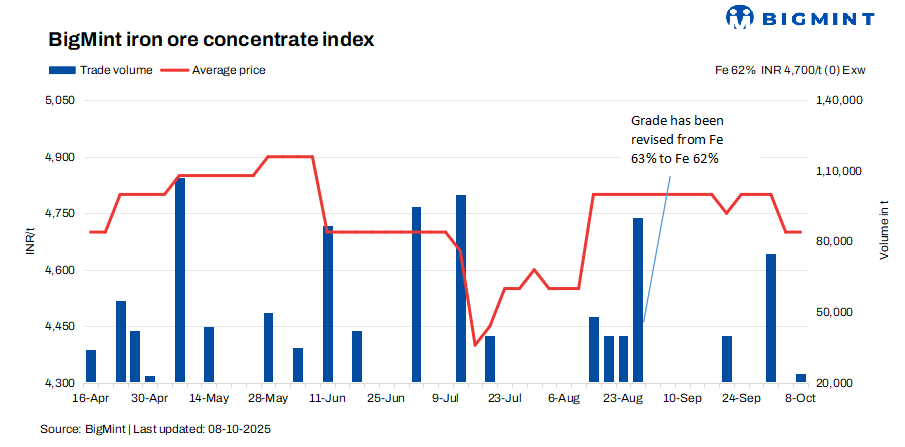

BigMint’s bi-weekly assessment for India’s iron ore concentrates remained stable at INR 4,700/tonne (t) ($53/t) exw-Jabalpur, unchanged from the previous evaluation on 4 October 2025 while falling by INR 100/t ($1/t) w-o-w. Prices held largely firm amid steady buying interest and limited market movement. Overall, deals for around 20,000-24,000 t were concluded at around INR 4,600-4,700/t exw.

Meanwhile, Fe 63% concentrate prices stood at INR 4,900/t ($55/t) exw, with a few deals concluded within this band during the week, indicating steady demand at higher grades.

Some sellers held back their offers, waiting for clarity on whether the export duty will be imposed or not. Market participants were cautious and preferred to assess the situation before making fresh deals. On the other hand, a few sellers have already booked their cargoes for this month, ensuring sales stability amid uncertainty in the policy outlook.

With the monsoon season coming to an end, logistical challenges are expected to ease considerably. Improved transportation and mining conditions are likely to support smoother production and dispatch activities, which could enhance supply in the coming weeks. This seasonal transition is expected to bring more consistency to the market movement and trading volumes.

Market players are now closely watching NMDC’s upcoming price revision and the government’s stance on the potential export duty, both of which are likely to set the direction for prices ahead.

Rationale

- One (1) trade was recorded in the publishing window and taken into consideration, receiving 50% weightage

- Nine (9) offers and indicative prices were heard, and six (6) were taken into consideration as T2 trades, receiving 50% weightage.

Factors supporting iron ore concentrate prices

- Pellet prices remain stable in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable at INR 10,300/t ($116/t) DAP on 7 October 2025 compared to the previous assessment on 3 October. Prices in the Raipur region held firm this week, with limited market movement, as overall activity stayed muted. The decline in sponge iron and billet prices weakened sentiment, curbing buying interest from sponge iron and steel producers. Market participants noted that continued softness in the semi-finished steel segment kept pellet demand subdued.

- Odisha iron ore fines prices hold steady w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,300/t ($60/t) ex-mines on 4 October 2025. Iron ore prices in Odisha held steady this week, with market activity remaining subdued due to the festive holidays and restricted production across key mining belts. According to market participants, spot availability remained limited, as most miners withheld fresh offers amid dispatch constraints and logistical challenges in the region.

Outlook

Iron ore concentrate prices are likely to remain stable in the coming week amid steady demand and cautious market sentiment. Improved post-monsoon logistics may enhance supply, but uncertainty over the potential export duty and NMDC’s upcoming price revision could keep trading limited. Overall, the market is expected to stay range-bound in the near term.

Leave a Reply